When Should RCM Not Be Applied?

Introduction

The Reverse Charge Mechanism (RCM) under UAE VAT law plays a significant role in ensuring the taxability of cross-border transactions and supplies made by non-residents. However, RCM is not a blanket rule, and there are several scenarios where RCM should not be applied. Misapplication of RCM can result in incorrect VAT returns, input tax disallowances, and even FTA penalties.

This blog will explore the key situations where RCM is not applicable under UAE VAT law, with references to relevant legislation and practical business examples.

________________________________________

🔄 Quick Recap: What is RCM?

RCM is a VAT mechanism where the recipient of goods or services, instead of the supplier, accounts for VAT on the supply. This mechanism is especially relevant when:

• Goods or services are imported from outside the UAE.

• The supplier is not a UAE VAT registrant.

• The supply involves certain specified goods (e.g. gold, hydrocarbons) between VAT-registered UAE businesses.

Legal Basis: Article 48 of the UAE VAT Decree-Law and Cabinet Decision No. 59 of 2017.

________________________________________

🚫 Scenarios Where RCM Should Not Be Applied

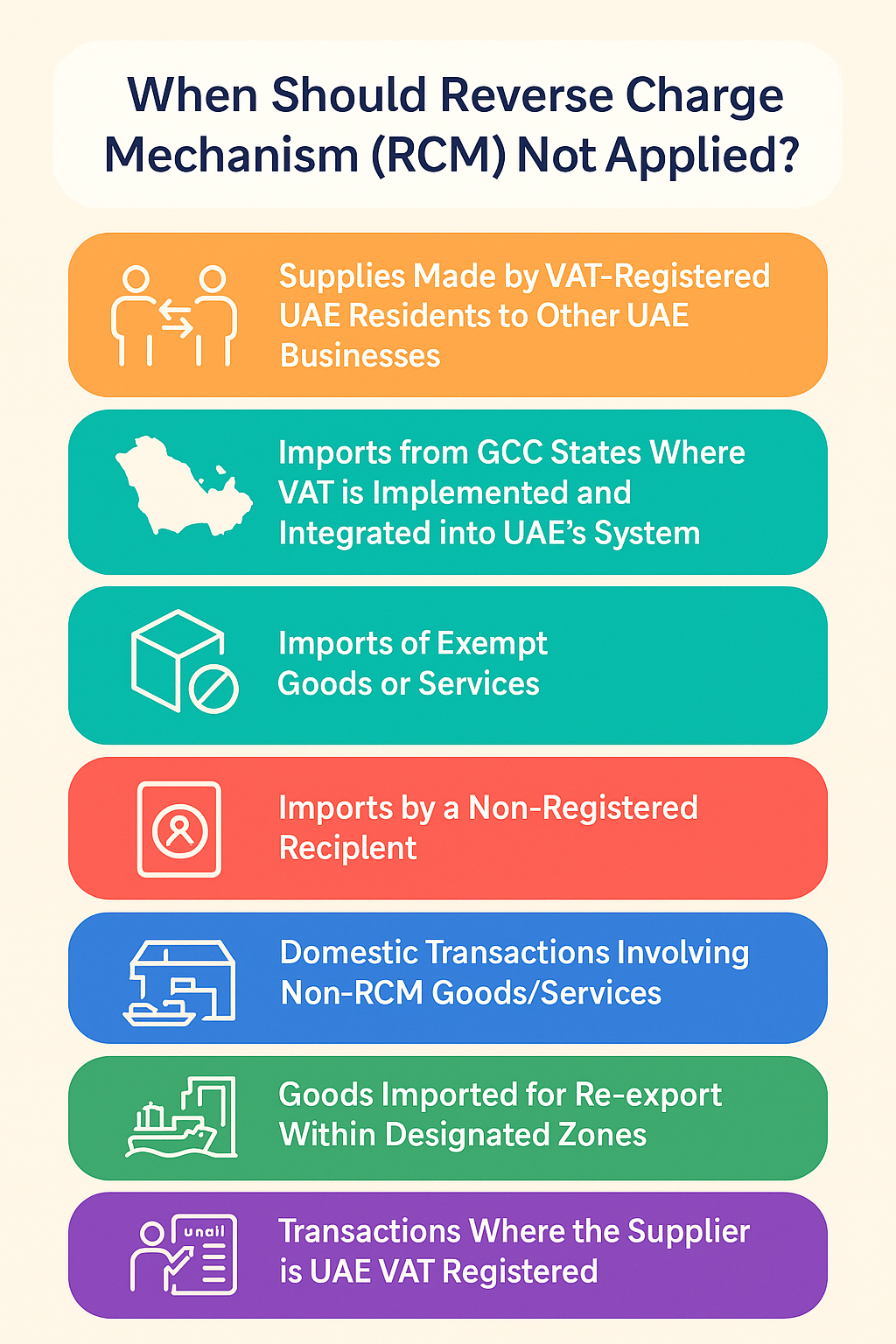

1. ✅ Domestic Supplies by UAE VAT-Registered Suppliers

If a UAE-based supplier is VAT-registered and is supplying goods or services to another UAE VAT-registered business, RCM does not apply.

Instead, the standard VAT mechanism is used:

• The supplier charges 5% VAT.

• The recipient can claim input VAT, subject to normal rules.

📝 Example: A UAE-based marketing agency charges AED 10,000 + 5% VAT to a UAE real estate firm. This is a normal supply, not under RCM.

________________________________________

2. ✅ Supplier is a Non-Resident But Registered for VAT in the UAE

If the foreign supplier is registered for VAT in the UAE, they are required to charge VAT directly. In such cases, RCM is not applicable.

📌 This is a common scenario with international consulting or software companies that register for UAE VAT to serve local clients.

📝 Example: A US-based software company registered for VAT in the UAE issues an invoice to a Dubai client with 5% VAT. The Dubai client should not apply RCM.

________________________________________

3. ✅ The Recipient is Not VAT-Registered in the UAE

RCM only applies where the recipient is VAT-registered in the UAE. If the recipient is an individual or a non-registered business, RCM does not apply.

🚨 Exception: In such cases, import VAT on goods may still be collected at the border by customs authorities.

📝 Example: A tourist buying software online from a foreign vendor is not required to self-account for VAT under RCM.

________________________________________

4. ✅ Imports of VAT-Exempt Goods or Services

If the goods or services imported are exempt from VAT, RCM does not apply because there is no VAT obligation to reverse charge.

📌 Examples of exempt items:

• Life insurance services

• Local passenger transport

• Residential bare land leasing

📝 Example: Importing insurance advisory services does not trigger RCM as such services are VAT exempt.

________________________________________

5. ✅ Supply Not Listed Under Designated RCM Rules

Only certain types of supplies are subject to mandatory RCM in the UAE. These are listed under Cabinet Decision No. 59 of 2017 and include:

• Crude and refined oil

• Natural gas

• Unprocessed and processed gold

• Hydrocarbons

If your supply is not listed, RCM does not apply — even if the transaction is domestic between two registered entities.

📝 Example: A UAE-based electronic parts trader sells goods to another UAE business — this is not covered under RCM.

________________________________________

6. ✅ Transactions within Designated Zones (with no mainland involvement)

Goods moving within or between designated zones (like JAFZA, DAFZA, etc.) and not entering UAE mainland may not be subject to RCM, depending on the supply chain and documentation.

📌 Caution: The supply must not involve movement into the mainland and the conditions for VAT-free designated zone transfers must be met.

📝 Example: Company A in JAFZA sells goods to Company B in DAFZA — with valid documentation and no UAE mainland involvement — RCM is not triggered.

________________________________________

7. ✅ Import of Goods Not Used for Taxable Supplies

If a VAT-registered business imports goods for exempt or non-business use, the reverse charge may not be applicable for the purpose of input tax recovery.

📝 Example: A financial services company imports office furniture for a non-VATable service — while they may pay import VAT, they cannot claim it via RCM as they are not making taxable supplies.

________________________________________

⚖️ Legal References

• Federal Decree-Law No. 8 of 2017 on VAT

• Executive Regulation (Cabinet Decision No. 52 of 2017)

• Cabinet Decision No. 59 of 2017 on Designated RCM sectors

• FTA Public Clarifications on RCM application

________________________________________

🧠 Practical Tips to Avoid Errors

✅ Check supplier’s VAT registration status before applying RCM.

✅ Review import documentation to confirm whether VAT is paid at customs.

✅ Classify transactions correctly based on supply type and sector.

✅ Document exemptions properly if RCM is not applied.

________________________________________

📌 Conclusion

While RCM is a critical tool in VAT compliance, it is not applicable in all scenarios. Knowing when NOT to apply RCM helps businesses avoid:

• Overstating output VAT

• Incorrect input tax claims

• Penalties and compliance issues with the FTA

📢 Need help reviewing your VAT filings for RCM accuracy? Contact our team of certified UAE tax professionals to ensure full compliance.

🌐 Visit us: www.sa-auditors.com

📧 Email: info@sa-auditors.com

📱 WhatsApp: +971-XX-XXXXXXX