When Is Reverse Charge Mentioned on Invoice?

Introduction

The Reverse Charge Mechanism (RCM) under the UAE VAT Law shifts the responsibility to pay VAT from the supplier to the buyer (recipient) in specific cases. This means that the supplier does not charge VAT on the invoice—but must still mention the reverse charge clearly.

Failing to correctly indicate reverse charge on invoices can result in non-compliance penalties during an FTA audit. Here we explain when and how to mention reverse charge on invoices.

________________________________________

📘 What is Reverse Charge Mechanism (RCM)?

Normally, the supplier charges VAT and pays it to the FTA. But under RCM, the recipient of goods or services is responsible for accounting and paying the VAT directly to the FTA. This is often used for cross-border transactions and specific local supplies.

________________________________________

✅ When Must Reverse Charge Be Mentioned on an Invoice?

Here are the main scenarios where the reverse charge must be stated on the invoice:

________________________________________

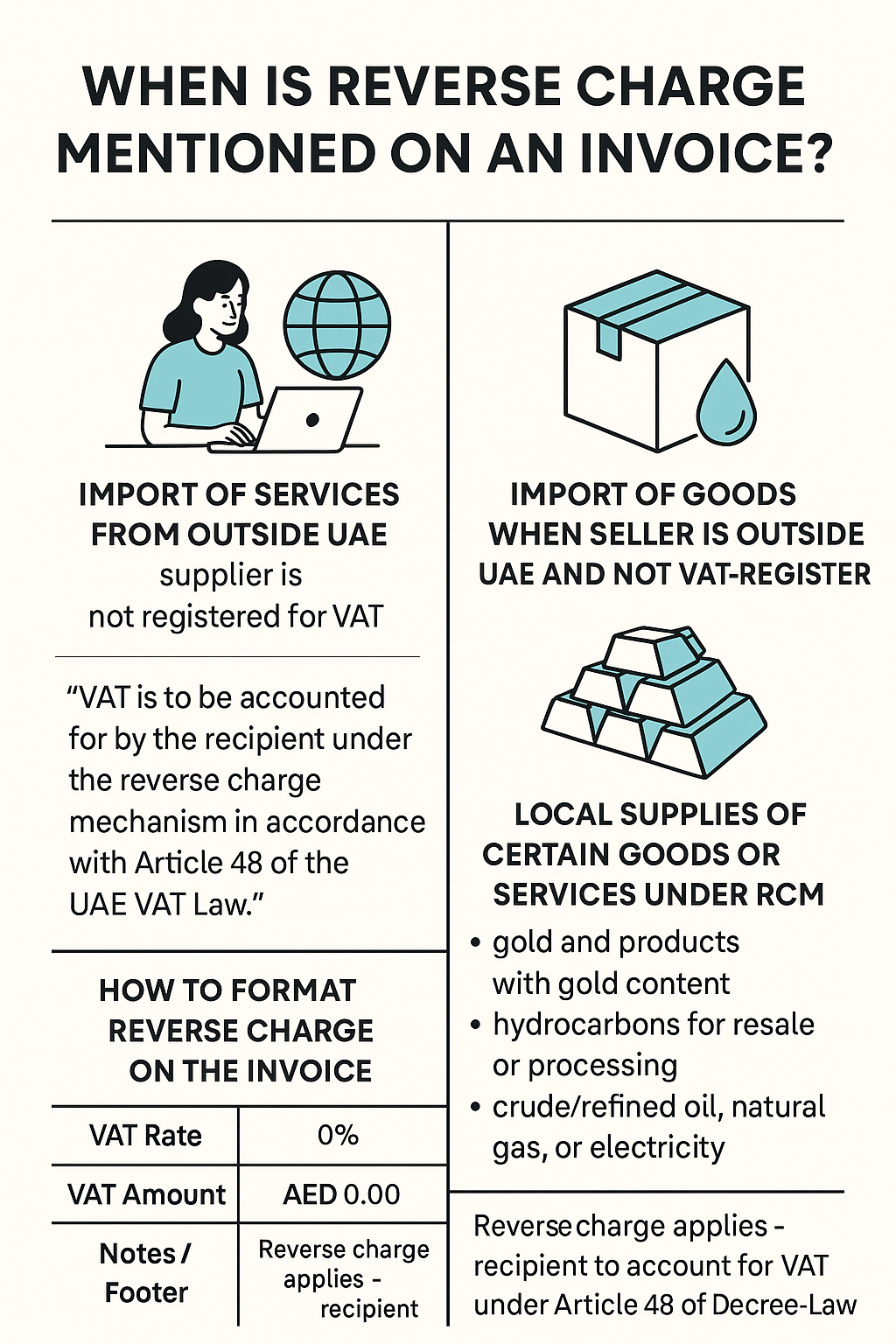

1️⃣ Import of Services from Outside UAE

When a UAE VAT-registered business purchases services from a foreign supplier who is not VAT-registered in the UAE, the UAE recipient must self-account for VAT under Article 48 of the VAT Decree-Law.

Example:

• Digital marketing services from a UK agency

• Software license purchased from a U.S. company

✅ Invoice must include this wording:

“VAT is to be accounted for by the recipient under the Reverse Charge Mechanism in accordance with Article 48 of the UAE VAT Law.”

________________________________________

2️⃣ Import of Goods from Non-Resident Suppliers

If the supplier is outside the UAE and is not registered for VAT, the UAE importer (buyer) becomes responsible for VAT under RCM during customs clearance.

Example:

• Importing raw materials from India

• Machinery purchased from Germany

🛑 The reverse charge is declared in the import declaration and in VAT Return Form 201 (Boxes 6 and 7).

💬 If the importer issues a self-invoice, they must clearly mention “Reverse Charge Applies”.

________________________________________

3️⃣ Domestic Supplies of Specific Goods and Services

As per Cabinet Decision No. 59 of 2017, reverse charge also applies within the UAE for the following supplies (even between VAT-registered businesses):

Examples:

Goods/Services Reverse Charge Applies If...

Gold and products with gold content Buyer is a registered reseller or manufacturer

Hydrocarbons (for resale/processing) Buyer is a VAT-registered business

Crude/refined oil, gas, electricity B2B between VAT-registered parties

Real estate supply From non-registered to registered business

Mobile phones, electronic devices, IT equipment For resale between VAT-registered businesses

✅ Invoice must include this note:

“Supply subject to reverse charge – VAT to be accounted for by the recipient.”

________________________________________

🔧 What to Include on a Reverse Charge Invoice?

Field Entry

Supplier TRN Mention (if available)

Customer TRN Mandatory for B2B

VAT Rate 0%

VAT Amount AED 0.00

Comment/Note “Reverse Charge Applies – VAT to be accounted by the recipient under Article 48”

Total Amount Gross amount (without VAT)

🧾 In B2B domestic RCM, full tax invoice is required even if VAT is not charged.

________________________________________

⚠️ Common Mistakes to Avoid

Mistake Consequence

Charging VAT on a reverse charge transaction Overpayment and wrong VAT return

Failing to mention RCM on invoice Risk of audit penalties

Using simplified invoice for RCM supply Non-compliance

Ignoring RCM box in Form 201 Underreporting VAT liability

________________________________________

📥 How to Report Reverse Charge in VAT Return (Form 201)?

Box Use

Box 3 Reverse charge on domestic purchases (gold, hydrocarbons, etc.)

Box 6 & 7 Imports of goods – customs declared

Box 10 Input VAT recoverable under reverse charge

________________________________________

✅ Best Practices

• Always verify if reverse charge applies before issuing invoice

• Use automated VAT invoice systems to flag RCM cases

• Maintain clear records with proper annotation

• Train accounting staff to distinguish normal vs RCM invoices

________________________________________

📌 Final Words

Mentioning reverse charge on invoices is not optional—it’s a legal requirement under UAE VAT law. Correctly indicating this ensures your business remains compliant, avoids VAT duplication, and passes any FTA audit with confidence.

💼 Need help reviewing your VAT invoicing process or implementing RCM-compliant billing?

Contact Sheikh Anwar Accounting & Auditing LLC for expert VAT consultancy and automation support.

📧 info@sa-auditors.com

🌐 www.sa-auditors.com