What is a Self-Billed Invoice?

In the landscape of Value Added Tax (VAT) compliance in the UAE, one lesser-known but powerful invoicing method is the self-billed invoice. It is particularly relevant in industries where buyers control pricing, or where suppliers are numerous, unregistered, or unable to issue timely invoices—such as gold trading, agriculture, logistics, or subcontracting.

Here we explores what a self-billed invoice is, when it is used, how it must be structured under UAE VAT Law, and how to avoid compliance issues.

________________________________________

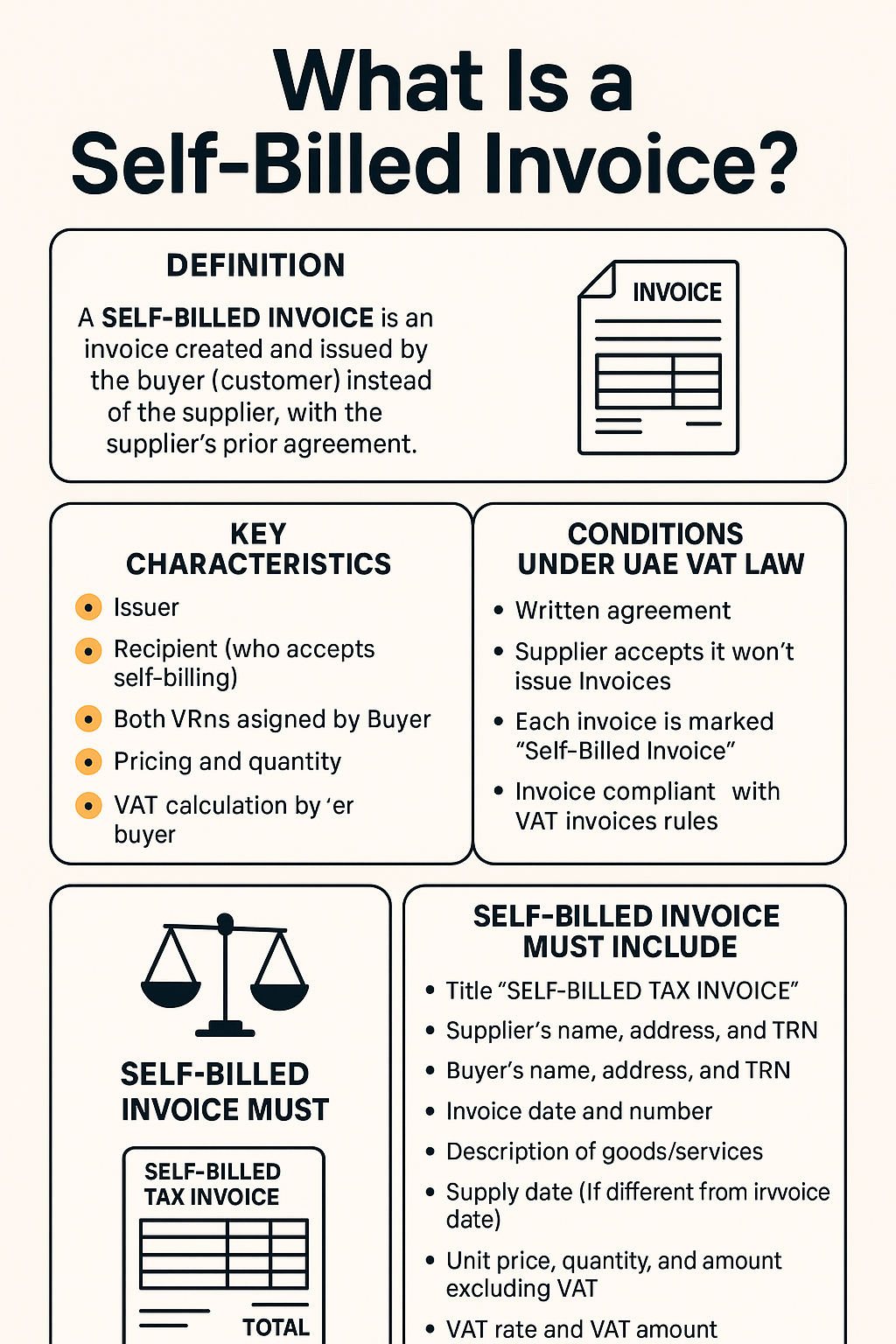

📘 Definition: What is a Self-Billed Invoice?

A Self-Billed Invoice is an invoice that is prepared and issued by the recipient (buyer) of goods or services on behalf of the supplier.

Unlike traditional invoices where the supplier issues the invoice to the buyer, in self-billing, the buyer generates the invoice and provides a copy to the supplier, along with payment.

________________________________________

🔍 Why Use Self-Billing?

Self-billing is typically used in the following situations:

Situation Description

High-volume small suppliers Buyer deals with many small or unorganized suppliers

Buyer determines price or quantity Buyer decides final quantity or pricing based on inspection, weighing, or resell price

Unregistered or semi-formal suppliers Supplier is not tax-savvy or unable to generate VAT-compliant invoices

Efficient bulk reconciliation Buyer prefers centralized billing for operational ease

________________________________________

✅ Examples of Where Self-Billing is Common

1. Gold & Precious Metal Trading

Refineries buying raw gold from multiple dealers generate self-billed invoices.

2. Supermarkets Buying from Farmers

Retail chains purchase produce in bulk and issue self-billed invoices based on weigh-in data.

3. Construction Firms & Subcontractors

Project contractors issue self-billed invoices to petty labor suppliers or transporters.

4. Auction Houses or Marketplaces

Platforms charge commission and issue invoices on behalf of sellers.

________________________________________

📜 UAE VAT Law on Self-Billing

As per Article 59 of Cabinet Decision No. 52 of 2017 and Executive Regulations under UAE VAT Law, self-billing is allowed, subject to certain conditions.

________________________________________

📄 Legal Conditions for Self-Billing in the UAE

To comply with UAE VAT law, the following 5 conditions must be met:

Condition Explanation

1. Written Agreement The buyer and supplier must sign a written self-billing agreement authorizing the buyer to issue tax invoices.

2. Supplier Acceptance The supplier agrees not to issue separate invoices for the same supply.

3. VAT-Compliant Invoice The invoice must meet all legal VAT invoice requirements (TRNs, breakdown, etc.)

4. Clearly Labeled The invoice must be clearly marked as a “Self-Billed Tax Invoice”

5. Record Keeping Both parties must retain copies of the invoice and agreement for at least 5 years (or 15 years for real estate).

________________________________________

🧾 What Should a Self-Billed Invoice Include?

The structure of a self-billed invoice must comply with Article 59 of the Executive Regulations, including:

Field Requirement

Title Must say "Self-Billed Tax Invoice"

Buyer & Supplier Names Full legal name, address, and TRNs for both

Invoice Date & Number Unique and sequential

Description of Goods/Services Clear itemization

Date of Supply If different from invoice date

Value & VAT Rate Show net value, applicable VAT (usually 5%), and total

Total Payable Grand total including VAT

Reference to Self-Billing Agreement Recommended in footer

________________________________________

⚠️ Common Mistakes to Avoid

Mistake Risk

No written agreement Non-compliant – may lead to FTA penalty

Both parties issue invoices Duplicate reporting and tax mismatches

TRNs missing or incorrect VAT return may be rejected

Incorrect tax rates or totals Overpayment or underpayment of VAT

Failing to retain records Risk during FTA audit

________________________________________

📌 Best Practices for Self-Billing

• ✅ Use FTA-compliant accounting software like Finabooks

• ✅ Automate invoice creation for multiple suppliers

• ✅ Schedule renewal of self-billing agreements annually

• ✅ Ensure both parties agree on price verification method (e.g., weight, delivery note)

• ✅ Perform quarterly reconciliations between self-billed amounts and supplier acknowledgements

________________________________________

✅ Benefits of Self-Billing

Benefit Description

Improved efficiency Buyer controls invoice generation cycle

Supplier support Helps small vendors comply with VAT

Centralized billing Easier accounting and reconciliation

Audit readiness All invoices are standardized and traceable

Faster payments Invoices can be paid quicker since they're buyer-issued

________________________________________

🧠 Final Thoughts

Self-billed invoices are a powerful tool under UAE VAT Law when used correctly. They offer streamlined operations and help in managing transactions with multiple or informal suppliers. However, strict adherence to FTA requirements is a must, including clear agreements, compliant invoice formats, and proper record-keeping.

💼 Need help drafting a Self-Billing Agreement or setting up automated VAT invoicing?

Contact Sheikh Anwar Accounting & Auditing LLC for end-to-end support on VAT compliance, invoicing, and FTA audits.

📧 info@sa-auditors.com

🌐 www.sa-auditors.com