What is a Qualifying Group?

Introduction

With the implementation of the UAE Corporate Tax Law, businesses are offered several relief mechanisms to ensure smoother transitions and reduce the tax burden in group structures. One such relief is for transactions within a “Qualifying Group”, where gains or losses on transfers of assets or liabilities between group companies can be deferred for tax purposes.

Here, we’ll explain what a Qualifying Group is, the conditions for eligibility, how it differs from a Tax Group, and the benefits and compliance requirements.

________________________________________

🧾 Legal Basis

The concept of a Qualifying Group is outlined in:

• Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses

• Article 26 – Transfers within a Qualifying Group

• Ministerial Decision No. 132 of 2023 – Intragroup Transactions

• FTA Public Clarifications (where available)

________________________________________

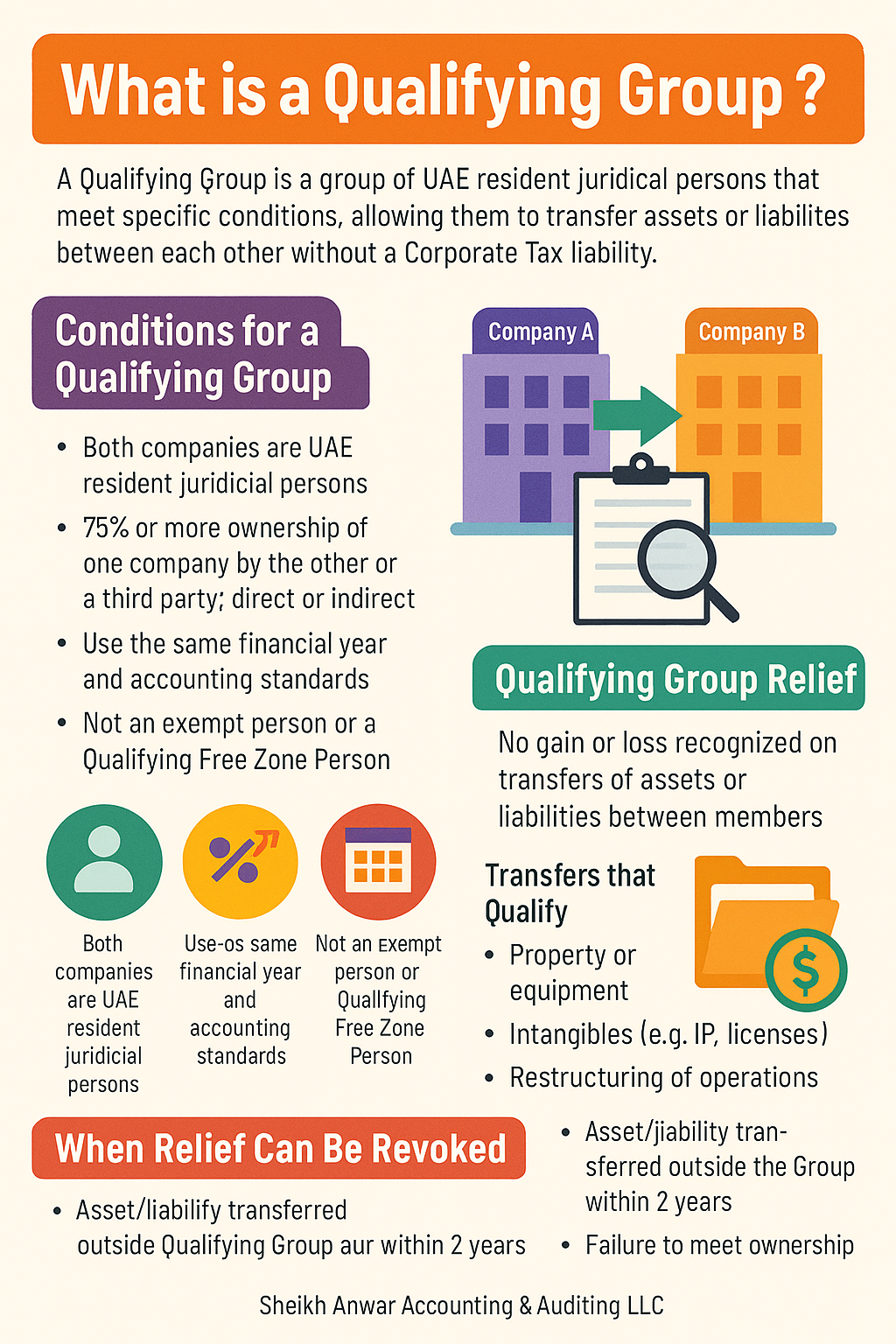

✅ What is a Qualifying Group?

A Qualifying Group is a group of two or more UAE resident juridical persons that meet specific ownership and legal conditions, enabling them to transfer assets or liabilities between each other without triggering a Corporate Tax liability on any gains or losses at the time of transfer.

This is not the same as a Tax Group (which files a single consolidated return), but rather a transaction-level relief provided under Article 26.

________________________________________

🧩 Conditions for a Qualifying Group

For two entities to be considered members of a Qualifying Group, all of the following conditions must be met at the time of the transaction:

1. Both companies are UAE resident juridical persons

o (e.g., LLCs or PSCs registered in the UAE)

2. One entity directly or indirectly owns at least 75% of the other,

or a third entity owns at least 75% of both entities

3. Both entities use the same financial year and accounting standards

4. Neither entity is an exempt person or Qualifying Free Zone Person

________________________________________

🔄 What Transactions Qualify for Relief?

Qualifying Group relief applies to transfers of assets and liabilities, such as:

• Transfer of property or equipment

• Transfer of intangibles (IP, licenses)

• Intragroup asset restructuring

• Consolidation or realignment of business operations

Effect: The transaction is not considered a taxable event. The gain or loss is deferred, and the asset takes on the tax base (cost) from the transferor.

________________________________________

🚫 When Is Relief Denied?

Relief under Article 26 is revoked retroactively if:

• The asset or liability is transferred outside the Qualifying Group within 2 years

• One of the entities ceases to meet the 75% ownership condition

• Either party becomes exempt or Qualifying Free Zone Person

In such cases, the transaction is retrospectively taxed in the original period, and penalties may apply.

________________________________________

📋 Difference: Qualifying Group vs. Tax Group

Feature Qualifying Group Tax Group

Purpose Transfer relief (Article 26) Consolidated CT return (Article 40–42)

Ownership threshold ≥ 75% direct or indirect ≥ 95% direct/indirect control

Tax registration Separate TRNs Single TRN for the group

Filing Separate returns One return filed by parent

Intragroup transactions Deferred tax treatment Eliminated entirely

________________________________________

💡 Practical Example

Company A owns 80% of Company B. Both are mainland UAE companies and prepare accounts using IFRS.

• Company A transfers machinery (book value AED 500,000, market value AED 1 million) to Company B.

• Because they are a Qualifying Group, no gain is recognized on the transfer.

• Company B inherits the tax base of AED 500,000 for depreciation purposes.

________________________________________

🧠 Strategic Benefits

• ✅ Facilitates group reorganizations without triggering tax liabilities

• ✅ Helps align asset management and operations

• ✅ Supports mergers and acquisitions within groups

• ✅ Encourages structuring flexibility

________________________________________

🧾 Key Compliance Considerations

• Must retain documentation proving qualifying status at the time of transfer

• Properly record carried-over tax bases of assets

• Monitor ownership structure and asset movements for 2 years post-transaction

• Include required disclosures in corporate tax returns

________________________________________

🧠 How Sheikh Anwar Accounting & Auditing LLC Can Help

We support businesses in:

✅ Evaluating qualifying group status

✅ Structuring tax-efficient intragroup transfers

✅ Preparing supporting documentation

✅ Monitoring group eligibility post-transfer

✅ Ensuring compliance with CT reporting obligations

Our team ensures that your business benefits fully from all tax reliefs while remaining 100% FTA compliant.

________________________________________

📞 Contact Us

📍 Sheikh Anwar Accounting & Auditing LLC

🌐 www.sa-auditors.com

📧 info@sa-auditors.com

📞 +971-XX-XXX-XXXX