VAT Treatment for Insurance and Reinsurance

Introduction

The UAE’s Value Added Tax (VAT) regime, implemented in 2018, has specific rules for the treatment of insurance and reinsurance services. Businesses operating in this sector must understand how VAT applies to premiums, commissions, and cross-border transactions to remain compliant and avoid penalties.

________________________________________

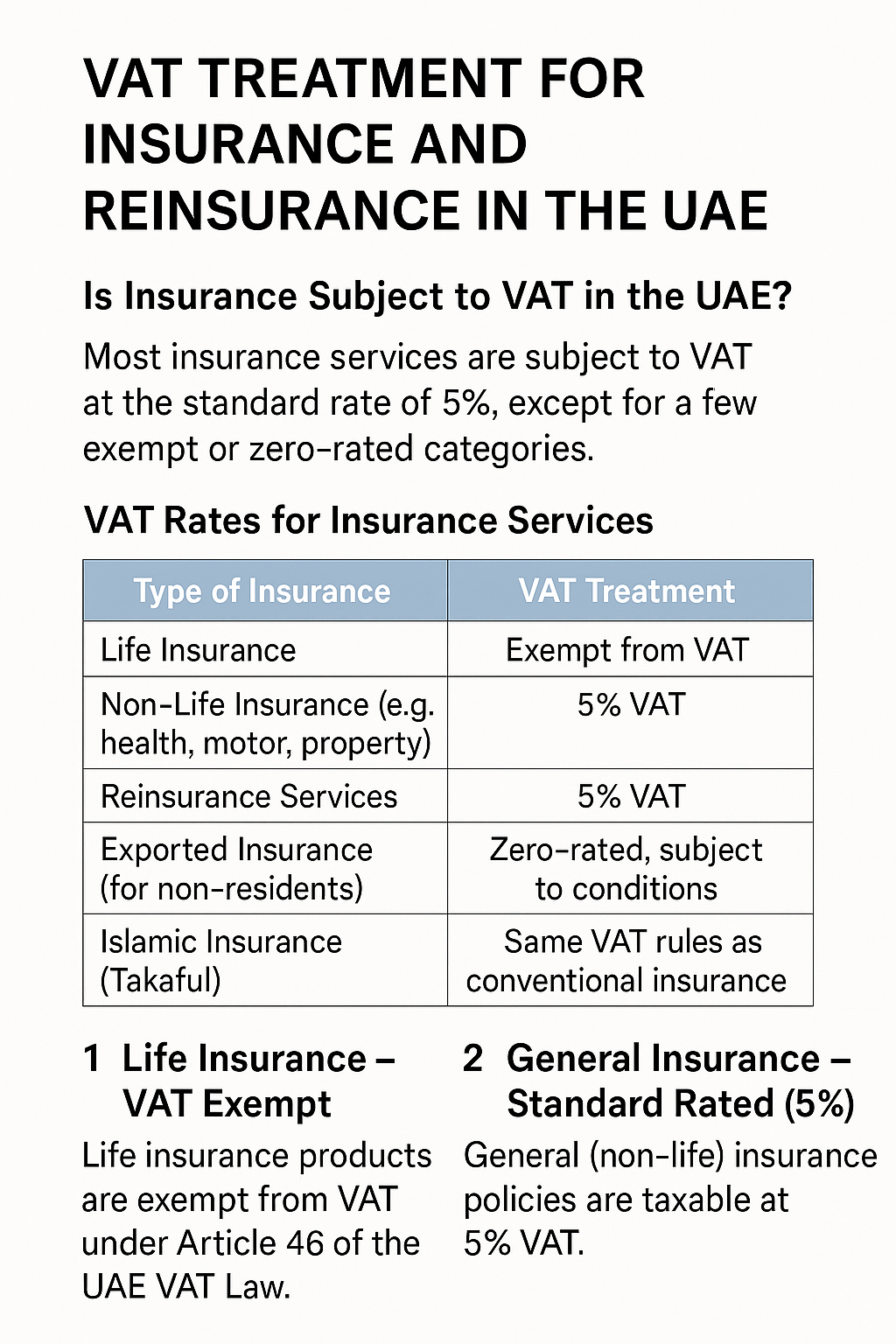

1. Is Insurance Subject to VAT in the UAE?

Yes. Most insurance services are subject to VAT at the standard rate of 5%, except for a few exempt or zero-rated categories. The place of supply, type of policy, and status of the recipient (e.g., individual or business, UAE resident or overseas) determine the VAT treatment.

________________________________________

2. VAT Rates for Insurance Services

Type of Insurance VAT Treatment

Life Insurance Exempt from VAT

Non-Life Insurance (e.g., health, motor, property) 5% VAT

Reinsurance Services 5% VAT

Exported Insurance (for non-residents) Zero-rated, subject to conditions

Islamic Insurance (Takaful) Same VAT rules as conventional insurance

________________________________________

3. Life Insurance – VAT Exempt

Life insurance products, including:

• Term life policies,

• Endowment policies,

• Whole life plans,

are exempt from VAT under Article 46 of the UAE VAT Law. This means insurers cannot charge VAT on life insurance premiums and cannot recover input VAT related to such supplies.

________________________________________

4. General Insurance – Standard Rated (5%)

General (non-life) insurance policies such as:

• Health insurance,

• Motor insurance,

• Property insurance,

• Travel insurance,

are taxable at 5% VAT. Insurers must issue tax invoices and collect VAT on premiums from customers.

________________________________________

5. Reinsurance – Subject to VAT

Reinsurance services are standard-rated at 5% VAT. Whether provided to UAE or foreign insurers, VAT must be charged unless the supply qualifies for zero-rating under export rules.

________________________________________

6. Zero-Rated Insurance Services

Insurance services provided to non-residents may qualify as zero-rated exports under Article 31 of the VAT Executive Regulations if:

• The non-resident is outside the UAE at the time of supply.

• The benefit of the service is not enjoyed within the UAE.

Note: Detailed documentation is required to support zero-rating.

________________________________________

7. VAT on Commission and Fees

Agents and brokers earning commissions or service fees for arranging insurance are providing taxable services, which are subject to 5% VAT, regardless of the underlying policy being exempt or taxable.

________________________________________

8. Input VAT Recovery

• For taxable insurance (general and reinsurance): Input VAT is recoverable.

• For exempt life insurance: Input VAT is not recoverable, unless there’s partial exempt input recovery allowed under the input apportionment method.

________________________________________

9. Important Compliance Considerations

• Issue VAT-compliant invoices for all taxable supplies.

• Apply correct VAT treatment to cross-border supplies.

• Maintain clear segregation of taxable vs exempt services for accurate VAT reporting.

• Use input VAT apportionment calculations for mixed supplies.

________________________________________

Conclusion

The VAT treatment of insurance and reinsurance services in the UAE requires careful classification and documentation. Insurance providers must stay updated with the FTA’s guidelines to ensure accurate VAT application, especially for mixed and international supplies.

________________________________________

📌 Need Help with VAT Compliance?

Sheikh Anwar Accounting & Auditing LLC offers end-to-end VAT advisory and filing services for insurance companies and brokers in the UAE. Contact us to stay compliant and penalty-free.

📧 info@sa-auditors.com

🌐 www.sa-auditors.com