VAT Rules for Restaurants and Cafes

Introduction

Since the introduction of Value Added Tax (VAT) in the UAE in 2018, the hospitality sector, including restaurants, cafes, food trucks, and catering services, has had to adapt its operations to stay VAT-compliant. While food is essential, the act of selling it in a commercial setting makes it a taxable supply.

Here we explores how VAT applies to restaurants and cafes, their invoicing obligations, and best practices to avoid penalties.

________________________________________

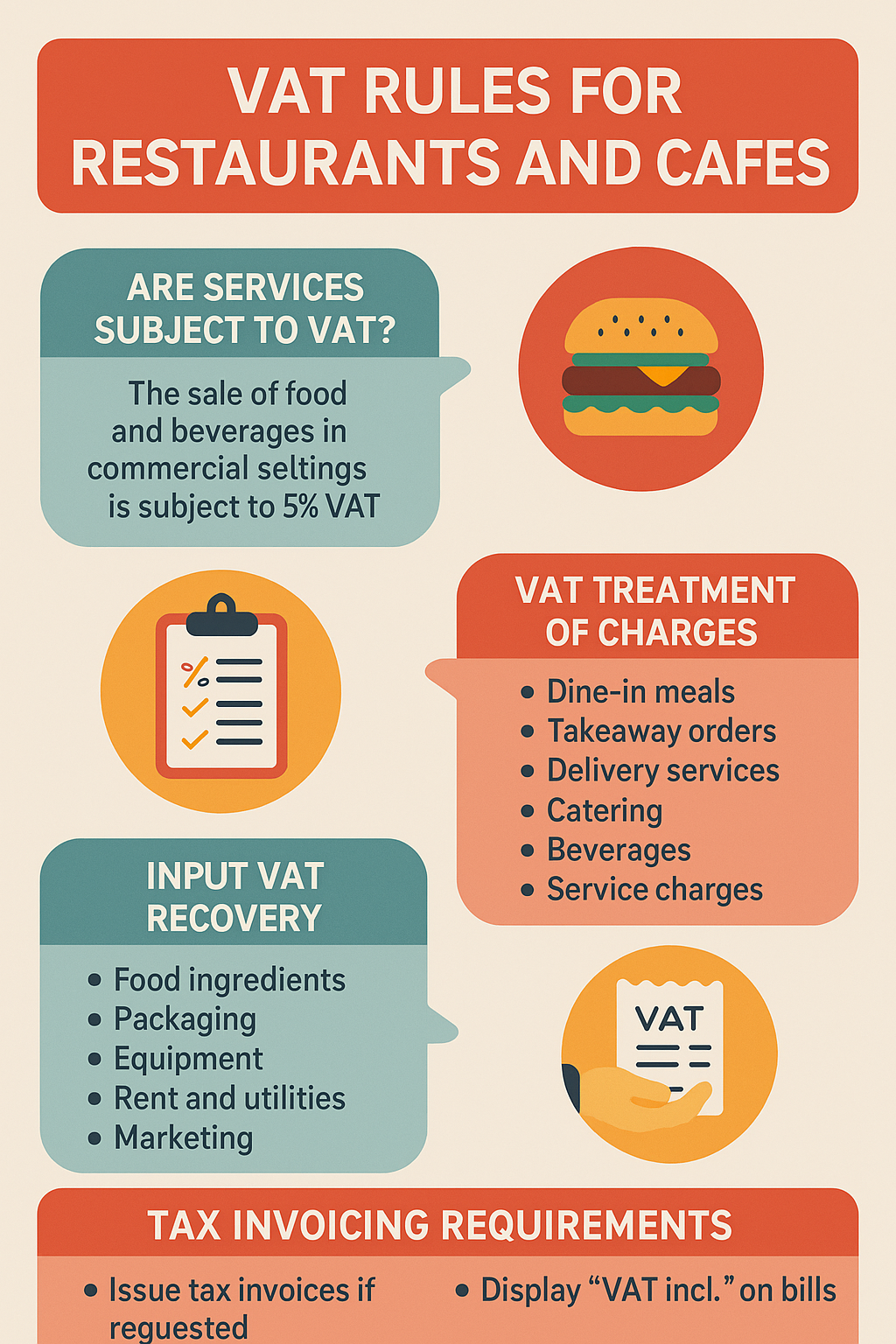

1. Are Restaurant and Café Services Subject to VAT?

Yes. The sale of food and beverages in a commercial setting (restaurants, cafes, cloud kitchens, food trucks, etc.) is subject to 5% VAT under UAE VAT Law.

This includes:

• Dine-in meals

• Takeaway orders

• Delivery services

• Catering and buffet packages

• Beverages, desserts, and snacks

• Service charges (if retained by the business)

________________________________________

2. What Is the VAT Treatment of Different Charges?

Item/Service VAT Rate

Dine-in food and beverages 5%

Takeaway orders 5%

Home delivery (if charged) 5%

Catering services 5%

Water bottles 5%

Non-alcoholic and alcoholic drinks 5% (alcohol also subject to excise duty)

Service charges retained by restaurant 5%

Tips or gratuity voluntarily paid to staff Not taxable

🚫 Note: If the service charge is distributed fully to staff and not retained by the business, it is not subject to VAT.

________________________________________

3. VAT Registration Requirements for Food Businesses

Restaurants and cafes must register for VAT if:

• Their taxable turnover exceeds AED 375,000 annually

Even small outlets, cloud kitchens, and food delivery-only businesses are required to register once this threshold is crossed.

________________________________________

4. VAT on Home Delivery and Online Food Platforms

If a restaurant charges a delivery fee, it must also add 5% VAT on that fee. Similarly:

• Orders placed via aggregators (e.g., Talabat, Deliveroo) may include VAT in the pricing

• The responsibility to issue a VAT invoice lies with the restaurant or aggregator, depending on who collects the payment and acts as the principal

________________________________________

5. Input VAT Recovery for Restaurants and Cafes

Restaurants can recover input VAT on:

• Food ingredients and supplies

• Packaging material

• Equipment (kitchen tools, fridges)

• Rent and utilities

• Marketing and advertising expenses

• Delivery vehicles (if used for business only)

🚫 Not recoverable:

• VAT on personal-use expenses

• Staff entertainment or meals not part of employment contract

________________________________________

6. Tax Invoicing Requirements

Restaurants must issue tax invoices if:

• The customer requests one

• The total bill is more than AED 10,000

For smaller amounts, a simplified tax invoice is acceptable.

A valid invoice should include:

• TRN of the restaurant

• Date of supply

• VAT amount and rate

• Total inclusive price

POS systems must be configured to print VAT-inclusive receipts and maintain records.

________________________________________

7. VAT Challenges in the F&B Sector

Challenge Risk

Not applying VAT on service charges Audit fines

Failing to register after crossing threshold AED 10,000 penalty

Claiming VAT on personal meals Input tax rejection

Not issuing tax invoices FTA compliance issues

Misunderstanding VAT vs Excise on alcoholic drinks Double taxation risk

________________________________________

8. Service Charges and VAT

Service charges are taxable at 5% if:

• They are retained by the restaurant as revenue

If service charges are entirely passed to staff as tips, they are not taxable. It's essential to clearly document this policy in accounts.

________________________________________

9. How to Stay Compliant

• Use VAT-enabled accounting software or POS system

• Display “VAT included” on menus or bills

• Keep detailed purchase and sales records

• File quarterly or monthly VAT returns

• Maintain clear segregation between taxable and exempt income

________________________________________

📌 Conclusion

Restaurants and cafes in the UAE must treat all their sales—dine-in, delivery, or takeaway—as taxable supplies, with VAT applied at 5%. Staying on top of VAT registration, tax invoicing, and proper documentation helps avoid penalties and ensures smooth FTA compliance.

________________________________________

💼 Need VAT Help for Your Restaurant or Café?

At Sheikh Anwar Accounting and Auditing LLC, we provide:

• VAT registration for restaurants and food businesses

• Setup of POS systems for VAT compliance

• VAT return filing and FTA support

• Review of service charge, delivery fee, and aggregator invoicing

📲 Contact us today for a free VAT advisory session.

📧 info@sa-auditors.com

🌐 www.sa-auditors.com