VAT Rules for Export and Import of Goods

Introduction

With the UAE positioned as a global trade hub, import and export activities are central to its economy. Understanding how Value Added Tax (VAT) applies to the movement of goods across borders is essential for businesses engaged in international trade. Failure to comply with UAE VAT rules for imports and exports can lead to costly errors, penalties, or blocked refunds.

Here we outlines the VAT treatment for import and export of goods under UAE VAT Law.

________________________________________

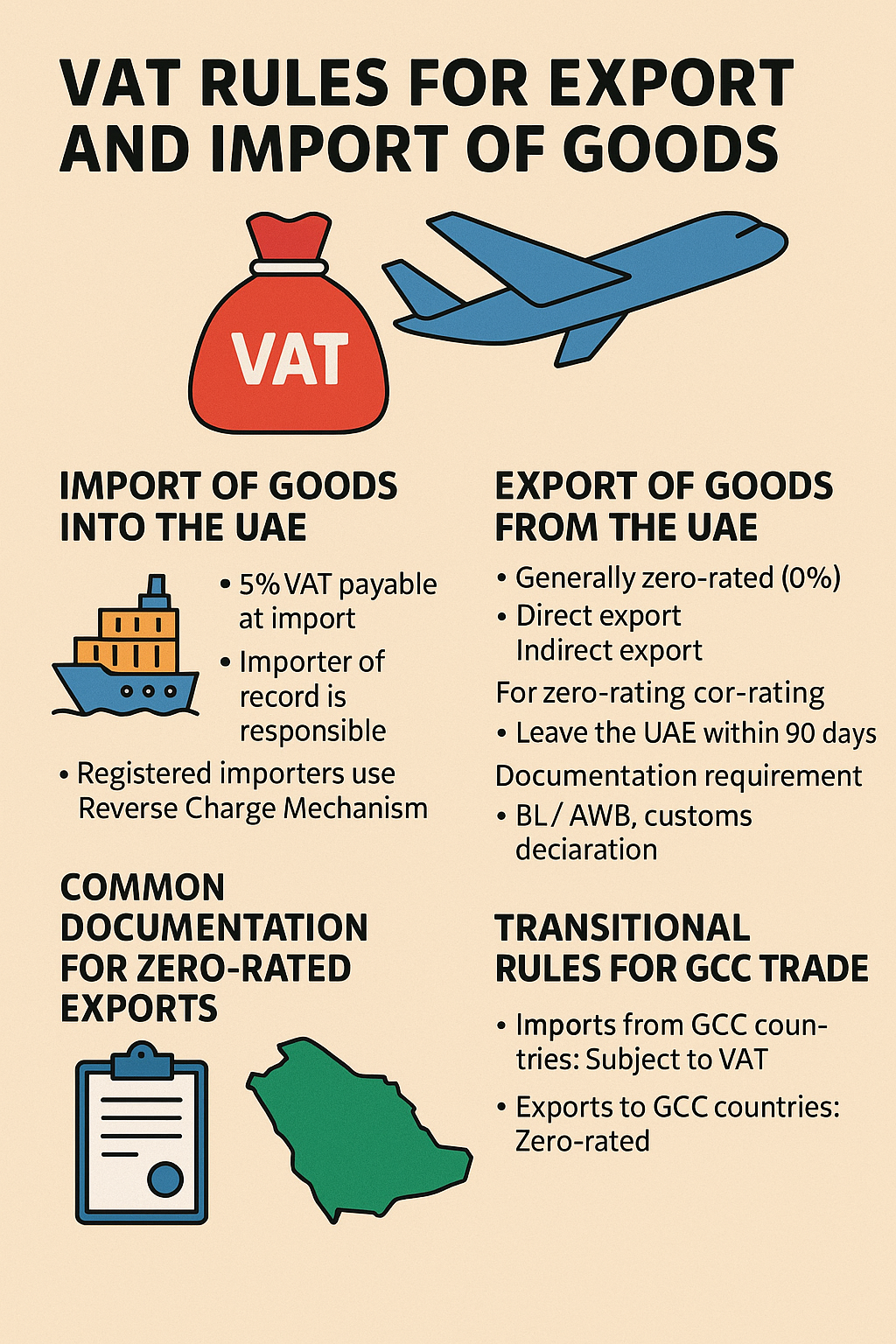

1. Import of Goods into the UAE

What Is Considered an Import?

Under UAE VAT Law, importing goods means bringing goods into the UAE from outside the GCC Implementing States.

VAT Treatment:

• 5% VAT is generally payable at the time of importation, unless you are a VAT-registered business using the reverse charge mechanism.

• VAT is calculated on the CIF value + customs duty (if any).

Who Pays the VAT?

• The importer of record is responsible for paying VAT.

• For VAT-registered importers, VAT is accounted for using Reverse Charge Mechanism (RCM)—no cash payment at customs is needed; the importer declares VAT in their VAT return.

________________________________________

2. Reverse Charge Mechanism for Imports

If the importer is VAT registered, VAT on imports is declared via the reverse charge:

• Input VAT and Output VAT are both recorded in the VAT return (Box 3 and Box 10).

• Net effect is zero, but documentation must be accurate.

If the importer is not registered, VAT must be paid to customs before goods are cleared.

________________________________________

3. Import into Designated Zones

Goods imported into Designated Zones (e.g., JAFZA, DAFZA) are not subject to import VAT, provided the goods:

• Remain within the Designated Zone

• Are not consumed or moved to mainland UAE

However, if the goods are transferred from a Designated Zone to mainland UAE, 5% VAT becomes applicable.

________________________________________

4. Export of Goods from the UAE

Exports are generally zero-rated (0%) under UAE VAT Law.

Types of Exports:

• Direct Export: Goods are physically shipped by the supplier or on their behalf.

• Indirect Export: Goods are collected by the overseas buyer or their agent.

Conditions for Zero-Rating:

• Goods must leave the UAE within 90 days of supply.

• Valid export documentation (BL, AWB, customs export declaration) must be retained.

• Recipient must be located outside the UAE (non-GCC or not VAT-registered in GCC).

If these conditions are not met, the supply becomes standard-rated at 5%.

________________________________________

5. Common Documentation for Zero-Rated Exports

To apply 0% VAT, the following should be maintained:

• Airway Bill (AWB) or Bill of Lading (BL)

• Export customs declaration

• Commercial invoice

• Proof of payment and delivery (e.g., shipping agent confirmation)

________________________________________

6. Transitional Rules for GCC Trade

Currently, the UAE treats GCC countries as non-implementing states, which means:

• Imports from Saudi Arabia, Oman, Qatar, Bahrain, or Kuwait are treated the same as imports from non-GCC countries (subject to VAT).

• Exports to those countries are zero-rated, subject to documentation requirements.

Once VAT becomes fully implemented across all GCC States under a unified system, VAT treatment will change based on whether the recipient is VAT-registered in that GCC state.

________________________________________

7. Re-Exports and Temporary Imports

Re-Exports:

• Re-exported goods can also be zero-rated, if they meet export conditions.

• Refund of import VAT may be possible under specific schemes (e.g., Dubai Customs refund process).

Temporary Imports:

• Temporary import schemes (for exhibitions, demo equipment, repairs) may be exempt from VAT and customs duty if returned within a specified timeframe.

________________________________________

8. Common VAT Errors in Import/Export

Error Risk

Declaring standard-rated export Overpayment or incorrect VAT return

Missing export documents Disqualification of zero-rating

Not applying RCM on imports Under-declared VAT

VAT charged on exempt or zero-rated supplies FTA penalties

Incorrect treatment of goods moved to/from Designated Zones Audit disputes

________________________________________

9. Best Practices for Compliance

✅ Maintain clear import/export documentation

✅ Reconcile customs data with VAT returns

✅ Apply reverse charge correctly

✅ Keep records for at least 5 years

✅ Use FTA’s EmaraTax portal for import VAT tracking

________________________________________

📌 Conclusion

Understanding VAT treatment for imports and exports is critical to cash flow, compliance, and smooth cross-border operations. Businesses must maintain robust documentation and apply correct tax treatment based on destination, zone, and registration status.

________________________________________

💼 Need Help with VAT on International Trade?

At Sheikh Anwar Accounting and Auditing LLC, we offer:

• Import/export VAT advisory

• Reverse charge setup and reconciliation

• Export documentation reviews

• FTA audit preparation

📲 Contact us today for expert VAT support on trade operations.

📧 info@sa-auditors.com

🌐 www.sa-auditors.com

Popular Blogs