VAT Refund for Non-Resident Businesses

Introduction

Businesses outside the UAE that are not VAT-registered locally may still incur VAT on goods and services consumed within the UAE during business operations such as exhibitions, conferences, consultations, or trading arrangements. Fortunately, the Federal Tax Authority (FTA) provides a refund scheme for non-resident foreign businesses, subject to specific eligibility and documentation requirements.

Here, we will explain who qualifies for the UAE VAT refund for non-resident businesses, the process, timelines, and common pitfalls to avoid.

________________________________________

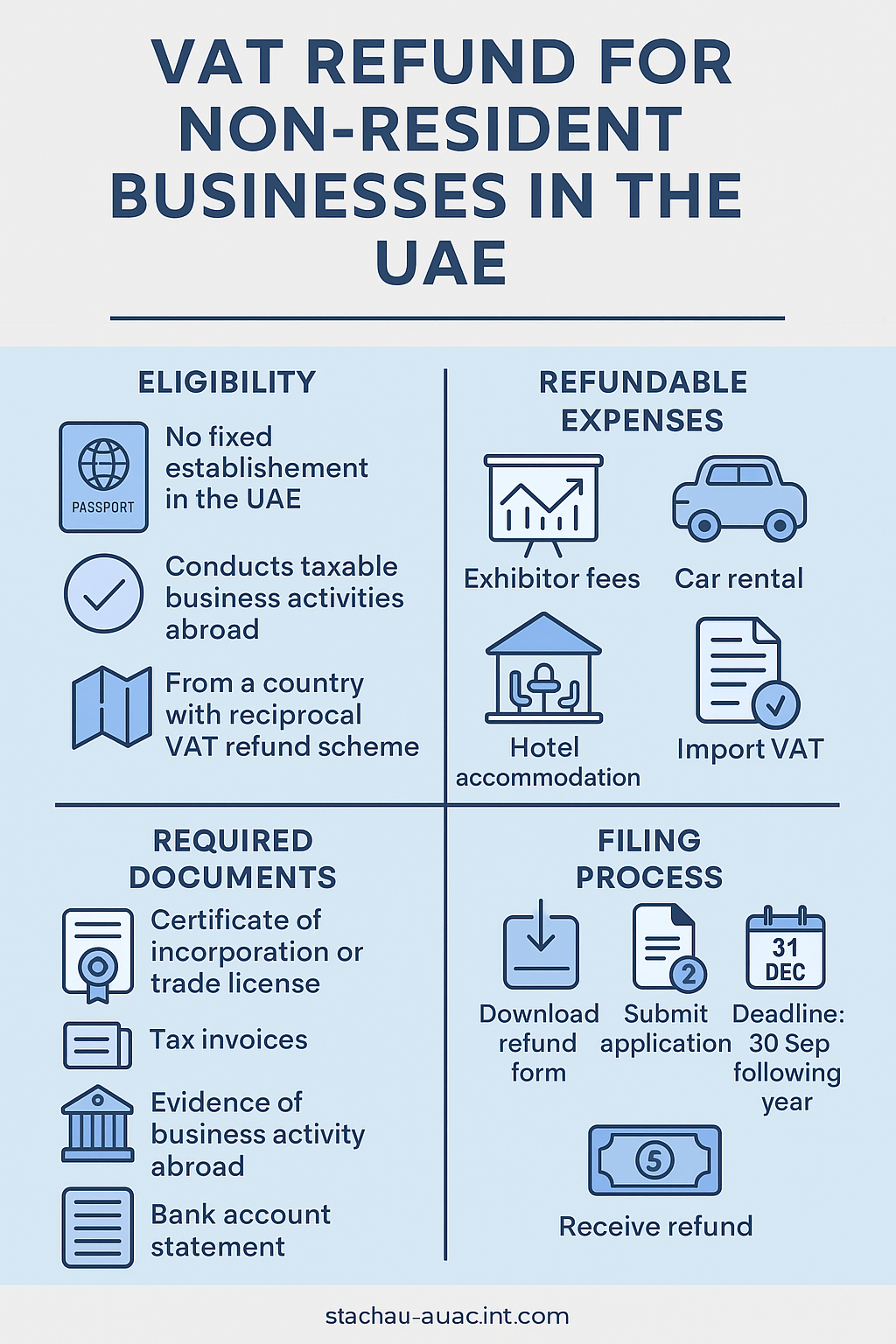

✅ Who Is Eligible for a Non-Resident VAT Refund?

A non-UAE established business may apply for a VAT refund if:

1. It is not a UAE resident or registered for VAT in the UAE

2. It has no fixed establishment in the UAE

3. It has not made any taxable supplies in the UAE

4. It is carrying out taxable business activities in its home country

5. It is from a country that provides reciprocal VAT refund rights to UAE businesses

📌 FTA publishes a list of countries eligible for the refund scheme based on reciprocity. Countries without a similar refund scheme will not qualify.

________________________________________

🚫 Who Is Not Eligible?

❌ Not Eligible if:

You have a UAE VAT registration (TRN)

You made local taxable supplies in the UAE

Your home country has no reciprocal VAT refund policy

You are a tourist or individual (use the tourist refund scheme instead)

________________________________________

🧾 Which Expenses Are Refundable?

Refunds can be claimed on business-related VAT expenses, such as:

✅ Refundable ❌ Not Refundable

Exhibitor fees at UAE expos Entertainment expenses

Hotel accommodation (for business use) Personal expenses

Car rental for business delegates Purchase of goods for resale in UAE

Import VAT (if paid and documented) Capital assets (in most cases)

📌 All claims must be supported by valid tax invoices from VAT-registered suppliers.

________________________________________

📝 Required Documents for Filing

Non-resident businesses must submit:

• Refund application form (available via FTA portal)

• Certificate of incorporation or trade license

• Proof of business activity in the home country

• Tax invoices with UAE VAT shown clearly

• Bank account verification letter (IBAN format, in applicant's name)

• Power of attorney (if filing through a tax agent)

📎 Documents must be notarized and attested in some cases.

________________________________________

📅 Refund Filing Timeline

📆 Period Covered 🕒 Deadline to Submit

1 Jan to 31 Dec 2024 By 30 September 2025

✅ You can file only one refund application per calendar year.

________________________________________

💸 Minimum Refund Thresholds

The total refund amount must meet the following:

• AED 2,000 minimum refund per application

• Can be a total of several invoices — not just one

________________________________________

📥 How to Submit the Refund Application

1. Visit the FTA website

2. Download and complete the "VAT Refund for Foreign Businesses" form

3. Attach supporting documents as listed

4. Email or courier the documents to FTA (check latest method on portal)

5. Await confirmation and further instructions

📌 The application is not filed through EmaraTax, but via a separate FTA process for foreign businesses.

________________________________________

⏱️ Processing Time

• The FTA may take up to 4 months to process the application

• Refund will be transferred to the verified foreign bank account

• Delays may occur if documents are missing or improperly submitted

________________________________________

🔁 Example Scenario

An IT consulting firm based in Singapore participates in GITEX 2024 and pays:

• AED 10,000 for booth rental

• AED 3,000 for hotel accommodation

• AED 1,500 for printing and signage

• Total VAT paid = AED 735

Since Singapore has a reciprocal VAT refund policy, and the firm made no taxable supplies in the UAE, they can apply for a VAT refund of AED 735.

________________________________________

⚠️ Common Mistakes to Avoid

❌ Mistake 🚫 Outcome

Claiming VAT without valid invoice Rejected or delayed

Using a UAE PO Box or agent’s address FTA may suspect UAE establishment

Missing attested documents Refund denied

Late filing after 30 Sep Refund automatically rejected

Claiming for employees’ personal expenses Refund not accepted

________________________________________

📌 Summary: Refund Checklist for Non-Residents

Task Status

Confirm country eligibility (reciprocity) ☐

Prepare attested trade license / COI ☐

Collect VAT-compliant invoices ☐

File before 30 Sep of following year ☐

Avoid taxable activity in UAE ☐

________________________________________

💼 Need Help Filing a Non-Resident VAT Refund?

At Sheikh Anwar Accounting & Auditing LLC, we provide expert assistance to:

• Verify eligibility for non-resident VAT refund

• Prepare and compile all documentation

• File and track your refund with FTA

• Handle FTA clarifications or objections

📧 Email us at: info@sa-auditors.com

🌐 Visit: www.sa-auditors.com