VAT on Financial Services: Exemptions and Challenges

Introduction

The financial services sector is vital to the UAE’s economy, encompassing banks, insurance companies, investment firms, and fintechs. When it comes to Value Added Tax (VAT), this sector faces unique complexities, primarily due to the presence of exempt supplies, mixed-use services, and international transactions.

Here we explains how VAT applies to financial services in the UAE, highlighting exemptions, taxable supplies, and key challenges.

________________________________________

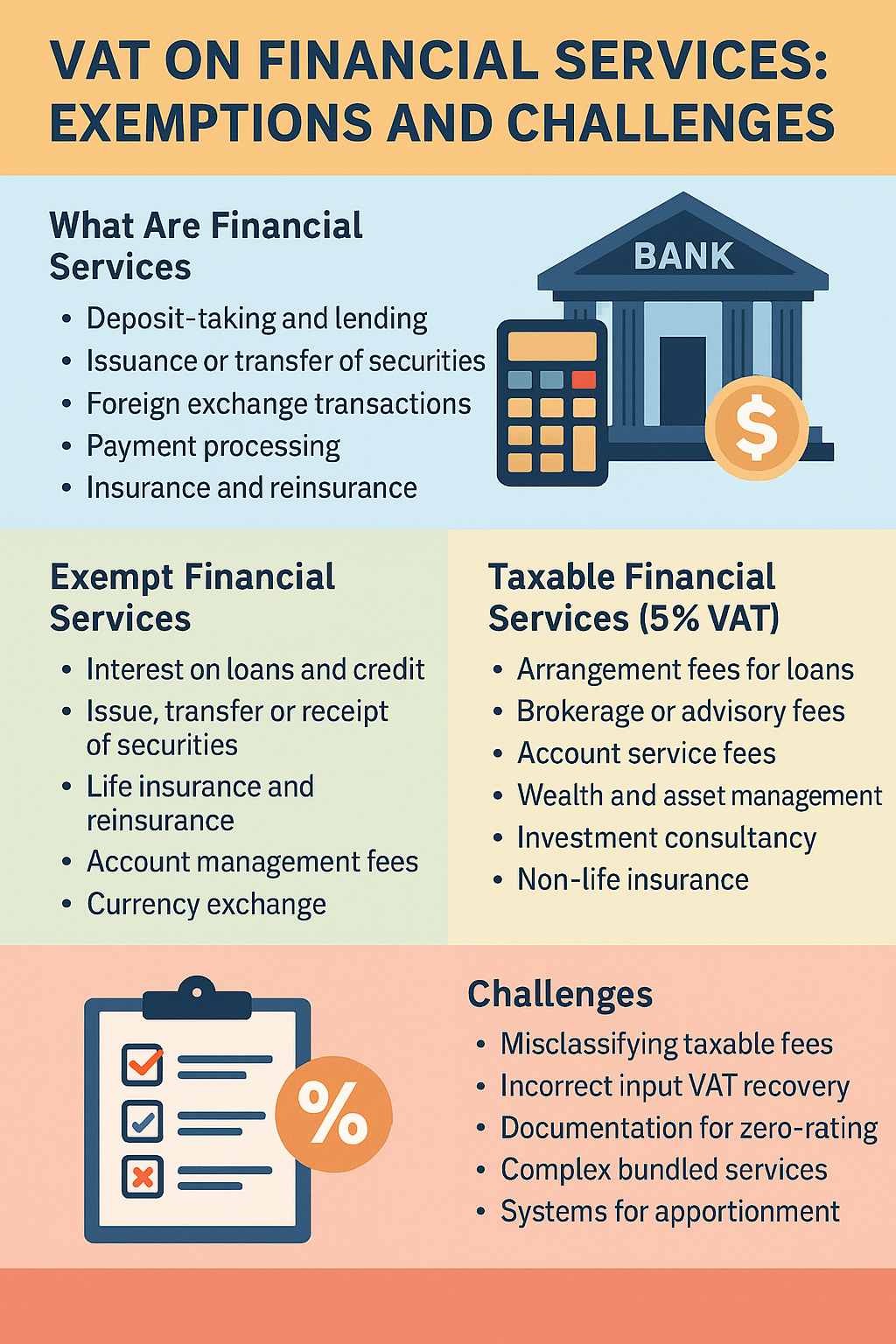

1. What Are Financial Services Under UAE VAT Law?

Financial services generally include:

• Deposit-taking and lending by banks

• Issuance or transfer of debt or equity securities

• Foreign exchange transactions

• Payment processing and money transfers

• Insurance and reinsurance

• Financial advisory and asset management

________________________________________

2. Which Financial Services Are Exempt from VAT?

Under UAE VAT Law, the following services are exempt (i.e., no VAT is charged, and input VAT is not recoverable):

Exempt Financial Services

Interest on loans and credit

Issue, transfer, or receipt of securities

Life insurance and reinsurance

Account management fees on current/savings accounts

Currency exchange (cash-to-cash transactions)

These exemptions apply only when no explicit fee, commission, or discount is charged.

________________________________________

3. Which Financial Services Are Taxable at 5% VAT?

VAT is charged at 5% when a fee, commission, or explicit charge is levied for the service.

Examples:

• Arrangement fees for loans or financing

• Brokerage or advisory fees

• Service fees for account maintenance

• Wealth and asset management

• Investment consultancy

• Non-life insurance (e.g., motor, property)

________________________________________

4. Zero-Rated Financial Services

In limited scenarios, financial services may be zero-rated (0%):

• If provided to recipients outside the UAE/GCC

• Subject to documentation proving the recipient is a non-resident

This typically applies to:

• Cross-border financial advisory

• International investment management services

________________________________________

5. Input VAT Recovery Challenges

Since financial institutions often provide a mix of exempt and taxable supplies, they face difficulty recovering input VAT.

Input VAT Recovery Options:

• Full recovery: Only for inputs related to taxable/zero-rated supplies

• Apportionment: For shared costs (e.g., office rent, utilities) based on revenue ratio

• No recovery: For inputs used solely in exempt supplies

The standard method of apportionment or a special method (approved by FTA) must be used.

________________________________________

6. VAT on Islamic Financial Products

Islamic finance products (like Ijarah, Murabaha) are treated similarly to conventional finance for VAT purposes.

• Where they functionally mirror taxable services → 5% VAT

• Where they mimic exempt financial services → exempt

FTA ensures Sharia-compliant finance is taxed on a substance-over-form basis.

________________________________________

7. VAT Challenges in the Financial Sector

Challenge Risk

Misclassifying taxable fees as exempt Underreporting VAT

Incorrect input VAT recovery Audit penalties

Not maintaining proper documentation for zero-rating FTA rejection

Complex bundled services (e.g., loan + insurance) Misapplication of VAT

Automated systems not configured for apportionment Compliance risk

________________________________________

8. Invoicing and Documentation Requirements

Even if the service is exempt, businesses must:

• Issue invoices when requested

• Maintain detailed records of revenue sources

• Track customer location and VAT status for cross-border supplies

• Retain all contracts, payment proofs, and VAT filings for 5 years

________________________________________

📌 Conclusion

Financial services providers in the UAE must balance between exempt and taxable activities, handle input VAT apportionment, and ensure accurate documentation—all while navigating industry-specific complexities. Proper categorization and VAT planning are essential for avoiding non-compliance.

________________________________________

💼 Need VAT Assistance for Your Financial Institution?

At Sheikh Anwar Accounting and Auditing LLC, we assist:

• Banks, insurance firms, and fintechs with VAT classification

• Input VAT apportionment planning

• Cross-border service zero-rating evaluation

• FTA audit preparation and VAT return filings

📲 Reach out to us for tailored VAT guidance in the financial sector.

📧 info@sa-auditors.com

🌐 www.sa-auditors.com