VAT on Consulting and Professional Services

Introduction

The UAE is home to a wide array of consultants and professionals—from legal and financial advisors to engineers, architects, and business consultants. Understanding how Value Added Tax (VAT) applies to consulting and professional services is crucial for service providers and their clients to remain compliant with UAE VAT law.

Here we cover the VAT treatment, obligations, and best practices for professionals and consulting firms.

________________________________________

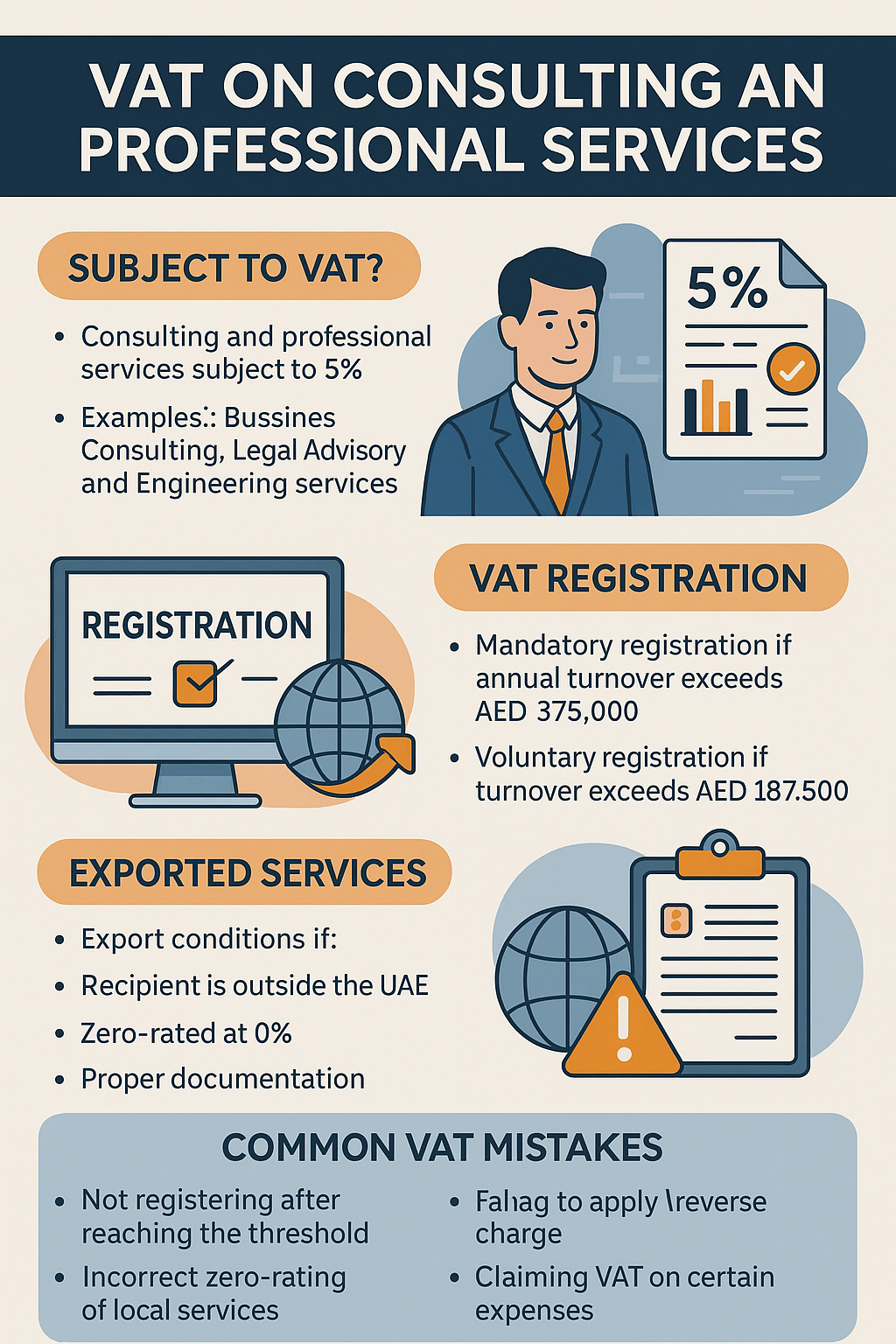

1. Are Consulting and Professional Services Subject to VAT?

Yes. Under UAE VAT law, consulting and professional services are considered taxable supplies and are subject to 5% VAT, unless they qualify for zero-rating or exemption under specific conditions.

Examples of taxable services:

• Business and management consulting

• Legal advisory and court representation

• Financial and tax consulting

• Engineering and architectural services

• IT, HR, and training consulting

• Freelance professional services

________________________________________

2. Who Should Register for VAT?

A consulting firm or individual must register for VAT if their annual taxable turnover exceeds:

• AED 375,000 – Mandatory registration

• AED 187,500 – Voluntary registration

This includes local clients, exports of services, and reverse-charged imported services.

Even freelancers and solo consultants must register once they exceed the threshold.

________________________________________

3. VAT on Local Services

If the service is provided within the UAE to UAE clients:

• 5% VAT applies

• The consultant or firm must issue a valid tax invoice with their TRN

• VAT must be reported and paid in the periodic return

________________________________________

4. VAT on Exported Services (International Clients)

Consulting services may be zero-rated (0%) if:

• The recipient is outside the UAE (non-resident and non-GCC VAT-registered)

• The service is consumed outside the UAE

• The provider maintains proper documentation (contracts, payment records, communication)

✅ Examples that qualify for zero-rating:

• A UAE-based tax advisor offering services to a UK company

• A management consultant advising a client in the USA

❌ Services rendered within the UAE (e.g., physical meetings, onsite work) may still be taxable at 5%, even if the client is foreign.

________________________________________

5. Reverse Charge on Imported Consulting Services

If a UAE VAT-registered business imports professional services from abroad (e.g., legal opinion from the UK, foreign IT consultant):

• They must self-account for VAT under the reverse charge mechanism

• VAT is reported in Box 3 and Box 10 of the return

________________________________________

6. VAT on Retainers and Advance Payments

• Retainer fees and upfront advances are subject to VAT at the time of payment

• A tax invoice must be issued when the advance is received

• Once the service is delivered, a final invoice may be issued, adjusting for VAT if required

________________________________________

7. Input VAT Recovery for Consulting Businesses

VAT-registered consulting firms can claim input VAT on:

• Office rent and utilities

• Software subscriptions and IT tools

• Marketing and advertising services

• Travel expenses (if strictly business-related)

• Legal, audit, and tax advisory services received

Not recoverable:

• VAT on client entertainment

• Non-business or personal expenses

• Services used for exempt supplies

________________________________________

8. Invoicing and Documentation Requirements

Each invoice must include:

• TRN of the provider

• Date and serial number

• Description of the service

• VAT rate and amount (5%)

• Total amount payable

Keep records for 5 years (15 years if related to real estate).

________________________________________

9. Common VAT Mistakes in Consulting Sector

Mistake Risk

Not registering despite reaching the threshold Penalties and fines

Misapplying 0% VAT on ineligible exports Tax audit exposure

Claiming VAT on entertainment/luxury expenses Disallowed input VAT

Not applying reverse charge on imported services Compliance breach

Failing to issue valid tax invoices Disputes and penalties

________________________________________

📌 Conclusion

Consultants and professional service providers must be proactive about VAT compliance—from registration to invoicing and filing. Understanding when to charge 5%, when to zero-rate, and how to apply the reverse charge mechanism is essential to protect your business from penalties and ensure full recovery of eligible input VAT.

________________________________________

💼 Need Help with VAT for Your Consulting Business?

At Sheikh Anwar Accounting and Auditing LLC, we support:

• VAT registration and advisory for consultants

• Reverse charge application and export service evaluation

• Filing of VAT returns and record-keeping setup

• Invoicing review and FTA audit readiness

📲 Contact us today for VAT support tailored to your professional services firm.

📧 info@sa-auditors.com

🌐 www.sa-auditors.com