VAT Implications on Commercial Leasing

Introduction

With the growth of the UAE’s business environment, commercial properties—offices, warehouses, retail units, and factories—play a critical role in economic activity. Understanding the Value Added Tax (VAT) treatment on commercial leases is essential for both landlords and tenants to ensure proper invoicing, compliance, and recovery of VAT.

Here we explains how VAT applies to commercial property leasing in the UAE.

________________________________________

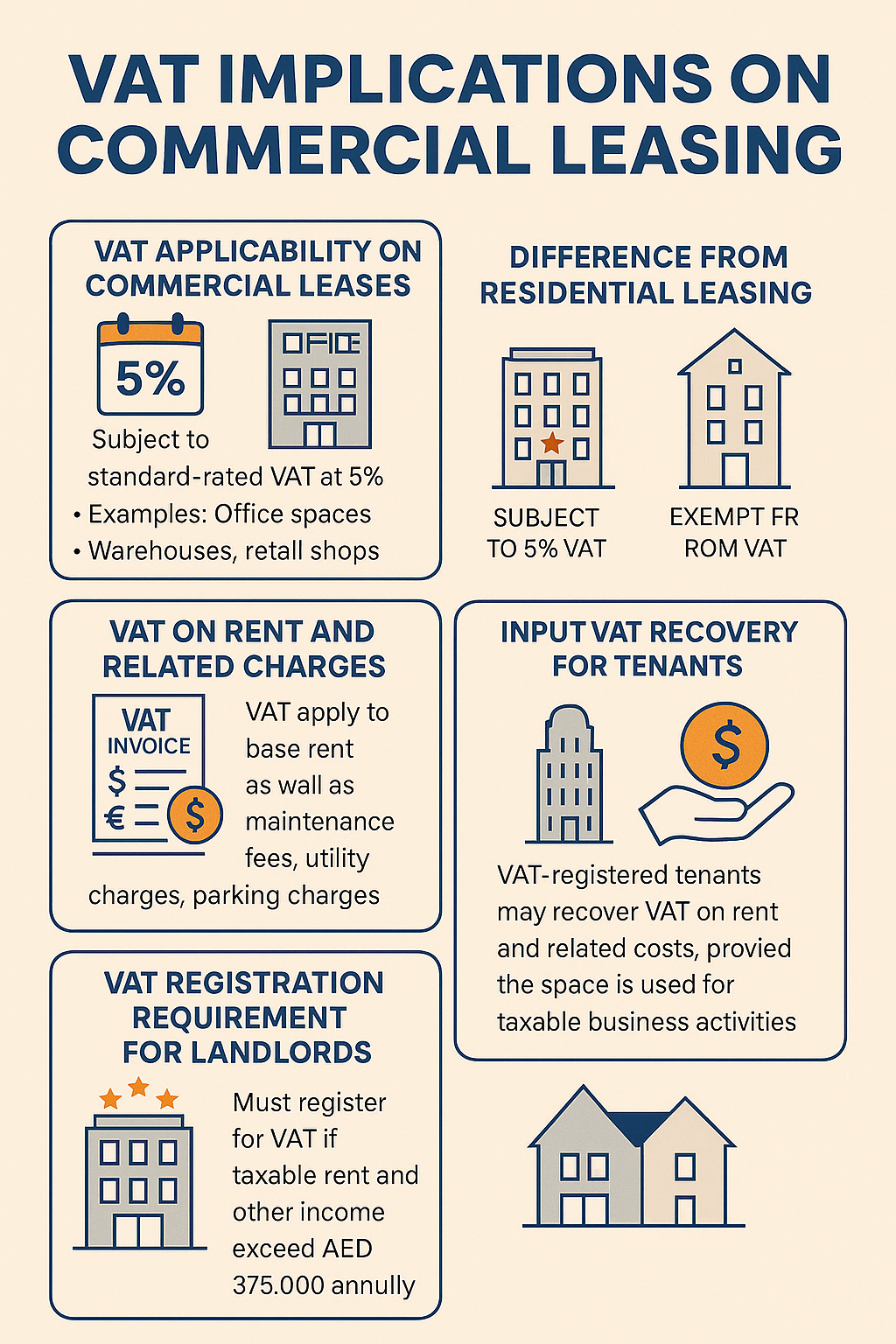

1. VAT Applicability on Commercial Leases

Under the UAE VAT Law, the leasing of commercial properties is considered a taxable supply, and is subject to standard-rated VAT at 5%.

✅ VAT applies to:

• Office space leases

• Warehouse and industrial unit rentals

• Retail shop rentals (e.g., in malls or high streets)

• Short-term commercial facility use (exhibition booths, meeting halls)

________________________________________

2. VAT on Rent and Related Charges

VAT is charged not only on the base rent, but also on associated charges such as:

• Maintenance fees (if not part of a service charge)

• Facility usage fees (e.g., parking, security)

• Utility service charges (if billed by landlord)

• Common area fees (if billed separately)

Landlords must:

• Charge 5% VAT

• Issue a valid tax invoice

• Report the VAT in their periodic VAT return

________________________________________

3. Who Pays the VAT?

• The tenant pays VAT in addition to the agreed rent amount.

• The landlord is responsible for:

o Charging VAT

o Issuing tax-compliant invoices

o Remitting VAT to the FTA

Example:

If rent is AED 100,000 per year, the invoice must include:

AED 100,000 + AED 5,000 VAT = AED 105,000 total

________________________________________

4. VAT Registration Requirement for Landlords

A commercial landlord must register for VAT if:

• Total taxable rent and other income exceed AED 375,000 per year

Once registered, the landlord is required to:

• Charge 5% VAT on all taxable commercial leases

• File VAT returns (monthly or quarterly)

• Maintain proper records and invoices

________________________________________

5. VAT Treatment of Security Deposits

• Refundable deposits (returned after lease ends) are not subject to VAT

• If any part of the deposit is forfeited, VAT becomes due on the retained amount

________________________________________

6. Input VAT Recovery for Tenants

Commercial tenants who are VAT-registered businesses may be able to:

• Recover VAT paid on rent and related costs as input tax

• Claim VAT in their VAT return, provided the space is used for taxable business activities

Not recoverable if:

• Used for exempt activities (e.g., financial services, residential sub-letting)

• No proper tax invoice is available

________________________________________

7. Difference from Residential Leasing

Leasing Type VAT Treatment

Commercial Leasing Subject to 5% VAT

Residential Leasing Exempt from VAT (unless short-term or hotel-style accommodation)

________________________________________

8. Sub-Leasing and Assignment of Lease

• Sub-leases of commercial property are also subject to 5% VAT

• Assignments or transfers of lease rights are taxable unless structured as a transfer of going concern (TOGC)—which may be zero-rated if conditions are met

________________________________________

9. Common VAT Errors in Commercial Leasing

Mistake Risk

Not registering for VAT Fines and backdated tax liabilities

Charging VAT without being registered Legal exposure

Not issuing valid tax invoices Input VAT disallowance for tenants

Treating commercial lease as exempt FTA audit and penalties

________________________________________

10. Key Compliance Tips for Landlords and Tenants

✅ Register for VAT if thresholds are met

✅ Charge and pay VAT on time

✅ Issue proper tax invoices

✅ Keep lease agreements and payment records

✅ For tenants: ensure business use and collect proper invoices for VAT recovery

________________________________________

📌 Conclusion

VAT has a direct impact on the leasing of commercial properties in the UAE. Landlords must charge VAT, tenants may recover it if eligible, and both must follow invoicing and reporting requirements. Missteps in VAT treatment can lead to penalties and disputes.

________________________________________

💼 Need Help With VAT on Commercial Leasing?

At Sheikh Anwar Accounting and Auditing LLC, we assist:

• Landlords with VAT registration and invoicing

• Tenants with input VAT recovery

• Real estate companies with VAT audits and compliance reviews

📲 Contact us for a free VAT consultation today.

📧 info@sa-auditors.com

🌐 www.sa-auditors.com