VAT for Real Estate Developers vs Investors

Introduction

The real estate sector is a key pillar of the UAE economy, and it is subject to special rules under UAE Value Added Tax (VAT) Law. However, the VAT treatment for real estate developers and property investors differs significantly based on the nature of their activities.

It breaks down the VAT implications for both groups and clarifies the rules regarding sales, leases, construction, and VAT recovery.

________________________________________

1. Real Estate: Supply Type Overview

UAE VAT law classifies real estate transactions as either:

Type of Supply VAT Treatment

Sale of residential property (first supply within 3 years) 0% (zero-rated)

Sale of residential property (after first supply) Exempt

Sale or lease of commercial property 5% VAT

Sale or lease of bare land Exempt

Lease of residential property Exempt

Construction services 5% VAT

Sale of property by unregistered individual Outside scope / exempt

________________________________________

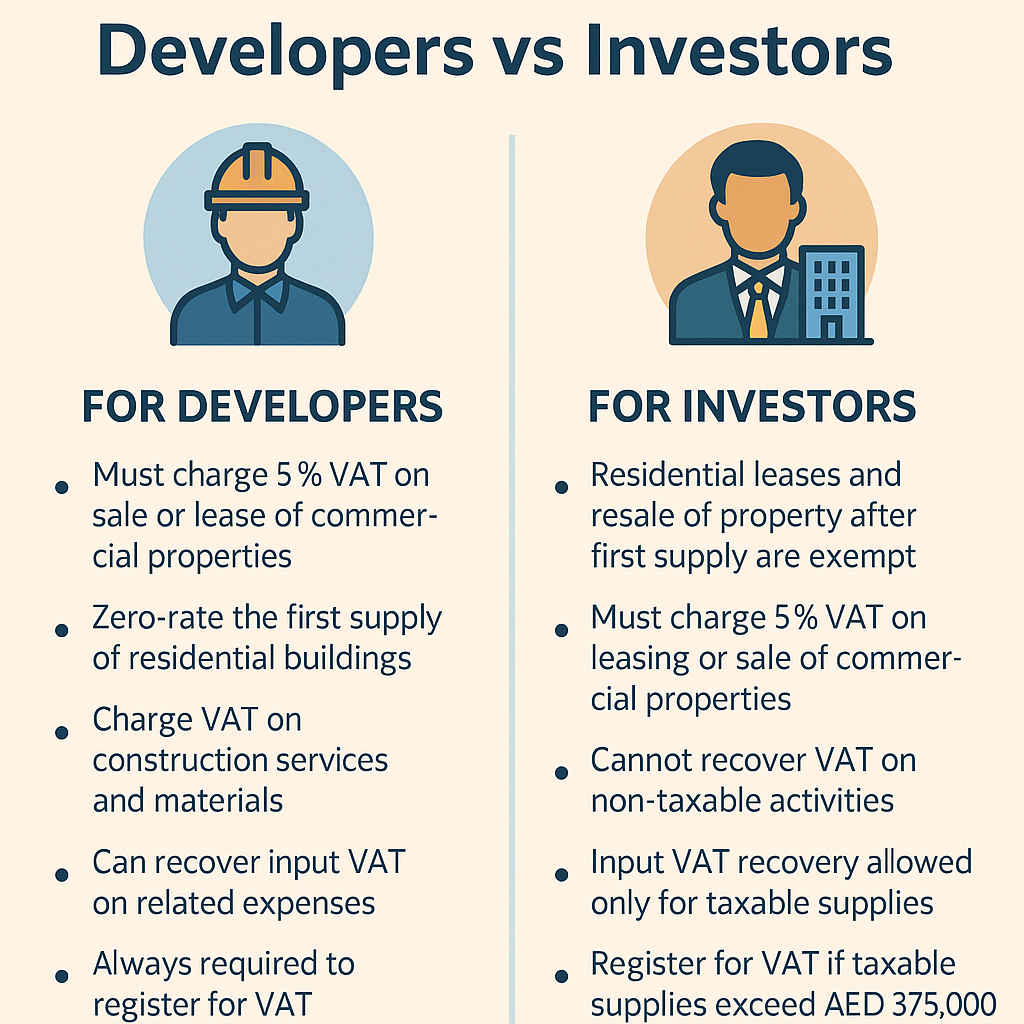

2. VAT for Real Estate Developers

Real estate developers are considered VAT-registered taxable persons engaged in economic activity.

✅ Key VAT Implications:

• Must charge 5% VAT on the sale/lease of commercial properties

• Zero-rate VAT on first supply of new residential buildings (within 3 years of completion)

• Must charge VAT on construction services, materials, and consulting

• Can recover input VAT on related expenses (land development, materials, labour, marketing, legal)

❗Conditions for Zero-Rated First Supply:

• Sale or lease of a newly constructed residential building

• Must occur within 3 years of completion

• Must be to the first buyer or tenant

After the first supply, the building becomes VAT-exempt.

________________________________________

3. VAT for Real Estate Investors

Investors purchase property to generate income, typically through:

• Leasing residential/commercial units

• Holding property for capital appreciation

• Buying/selling ready properties (not under development)

🔹 Key VAT Rules for Investors:

Activity VAT Treatment Input VAT Recoverable?

Leasing residential unit Exempt No

Leasing commercial unit 5% VAT Yes (on related expenses)

Selling commercial unit 5% VAT (if registered) Yes

Selling residential property (after first supply) Exempt No

Property held for capital gain only Outside scope No

📌 Investors leasing commercial units must register for VAT if rental income exceeds AED 375,000/year.

________________________________________

4. VAT Registration Obligations

Party Must Register If...

Developer Always, due to taxable activity

Investor If earning > AED 375,000 from taxable supplies (e.g., commercial leasing)

________________________________________

5. Input VAT Recovery: Developer vs Investor

Expense Type Developer Investor

Construction materials Recoverable Not applicable

Legal & professional fees Recoverable Only if linked to taxable supply

Leasing agent commission Recoverable (commercial only) Recoverable (commercial only)

Residential leasing costs Not recoverable Not recoverable

Input VAT recovery is only allowed where the property is used to make taxable supplies.

________________________________________

6. Common VAT Mistakes in Real Estate

Mistake Risk

Treating resale of residential property as zero-rated Wrong VAT treatment

Not charging VAT on commercial rent Underreporting

Claiming VAT on residential leasing costs Disallowed input VAT

Missing VAT registration for commercial rental income FTA penalty

Not issuing tax invoices for taxable supplies Non-compliance

________________________________________

📌 Conclusion

VAT compliance in the real estate sector depends on whether you're a developer actively constructing and selling properties or an investor managing property assets. Understanding the correct VAT treatment ensures compliance, optimizes recoveries, and helps avoid penalties.

________________________________________

💼 Need Expert VAT Help?

At Sheikh Anwar Accounting and Auditing LLC, we assist:

• Real estate developers with VAT registration and construction VAT planning

• Investors with lease VAT treatment and return filing

• Clarifying input VAT recovery eligibility

• FTA audit support and real estate-specific compliance

📲 Contact us today for tailored VAT consultancy in the real estate sector.

📧 info@sa-auditors.com

🌐 www.sa-auditors.com