VAT for Charitable and Non-Profit Organizations

Introduction

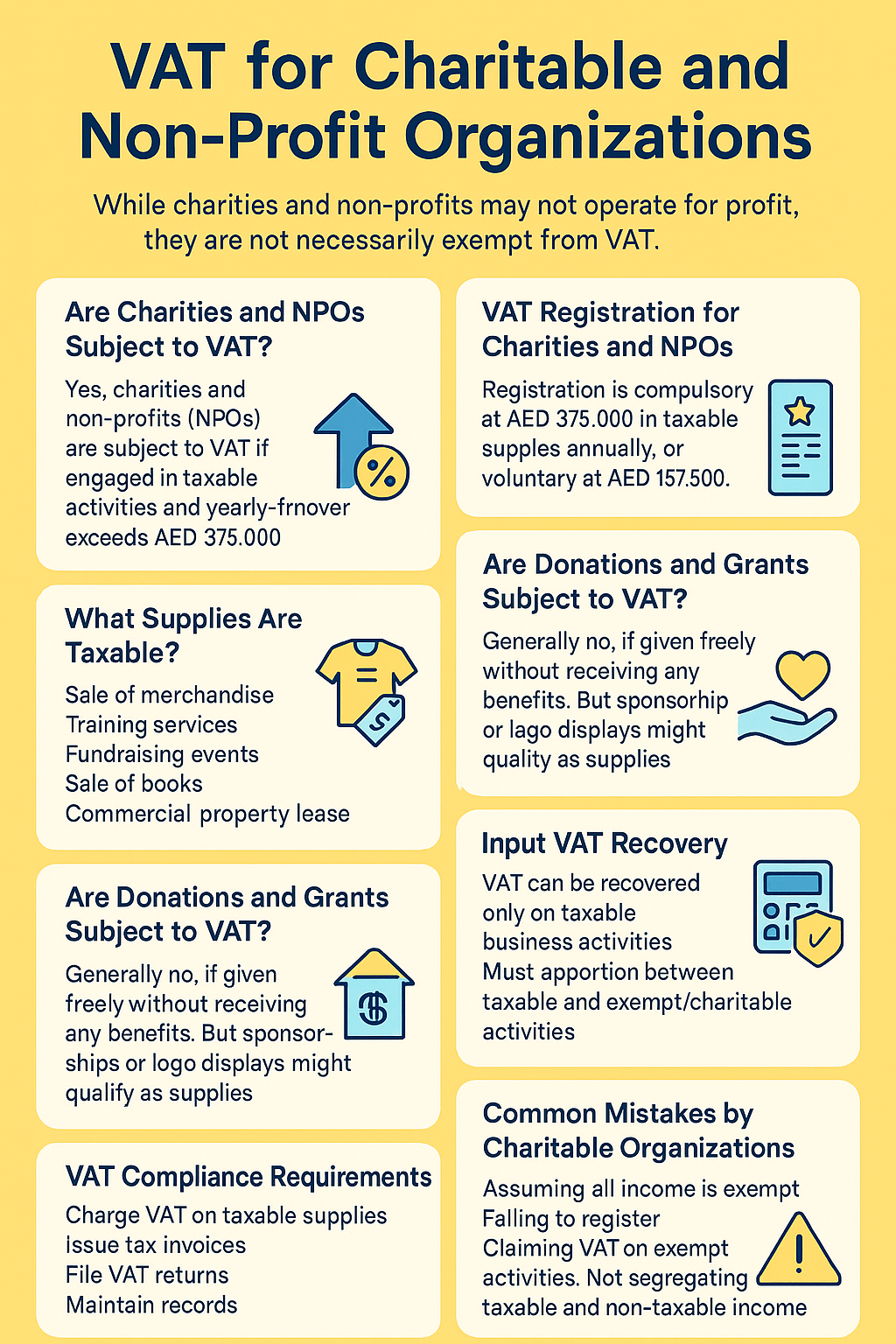

Charitable institutions and non-profit organizations (NPOs) play a vital role in social development by supporting humanitarian, religious, cultural, and educational activities. While they may not operate for profit, they are not automatically exempt from VAT obligations under UAE VAT Law.

Understanding when and how Value Added Tax (VAT) applies to these entities is crucial for compliance and financial transparency.

________________________________________

1. Are Charities and NPOs Subject to VAT?

Yes, charities and NPOs are subject to VAT in the UAE if:

• They are engaged in taxable economic activities, such as selling goods or services

• Their taxable turnover exceeds AED 375,000 annually

Examples of taxable activities:

• Ticketed charity events

• Sale of merchandise or books

• Leasing of property

• Providing paid training or services

________________________________________

2. VAT Registration for Charities and NPOs

A charitable organization must register for VAT if:

• Its taxable supplies (not donations or grants) exceed AED 375,000 in 12 months

• It engages in commercial-like activities on a regular basis

They may also voluntarily register if turnover exceeds AED 187,500.

________________________________________

3. What Supplies Are Taxable?

Activity VAT Treatment

Sale of merchandise 5% VAT

Training services (if not exempt) 5% VAT

Fundraising events with paid tickets 5% VAT

Sale of books or printed material 5% VAT

Commercial property lease 5% VAT

Free grants/donations (no benefit to donor) Not taxable

________________________________________

4. Are Donations and Grants Subject to VAT?

Generally, donations and grants are not subject to VAT, if:

• They are given freely without receiving goods or services in return

• There is no benefit or right provided to the donor

However:

• If the donor receives advertising (e.g., logo display), branding, or naming rights, then the contribution may be considered a supply and subject to 5% VAT

________________________________________

5. VAT Exemptions and Zero-Rating

✅ Exempt Supplies (No VAT charged, no input recovery)

• Residential property leases by charities (in most cases)

• Certain financial services

✅ Zero-Rated Supplies (0% VAT charged, input recovery allowed)

• International donations or aid sent outside the GCC (if conditions met)

• Some healthcare or education-related services by approved bodies

To apply exemptions or zero-rating, the charity must often:

• Be approved by the UAE Cabinet as a "Designated Charity"

• Provide the service for public benefit

• Maintain proper records and approvals

________________________________________

6. Input VAT Recovery

Only VAT related to taxable business activities can be recovered.

Expense Type Input VAT Recovery

Event expenses (with VAT-charged tickets) Yes

Goods for resale (with VAT-charged revenue) Yes

Office rent for general operations Partial (depends on taxable use)

Purely charitable activities (free services, no revenue) No

Charities must apportion input VAT between:

• Taxable activities (recoverable)

• Exempt/charitable activities (non-recoverable)

________________________________________

7. VAT Compliance Requirements

Charities that are VAT-registered must:

• Charge VAT on taxable supplies

• Issue proper tax invoices

• File VAT returns on time

• Maintain detailed financial records

• Segregate taxable and non-taxable income

________________________________________

8. Common Mistakes by Charitable Organizations

Mistake Risk

Assuming all income is exempt Incorrect returns

Failing to register when required Fines and penalties

Claiming VAT on exempt activities Input VAT disallowance

Not segregating taxable and non-taxable activities Audit issues

Misclassifying donations vs sponsorships Incorrect VAT treatment

________________________________________

📌 Conclusion

While charitable organizations may not operate for profit, they still fall under the UAE VAT regime when engaging in taxable activities. Understanding the difference between donations, sponsorships, sales, and services is critical to ensure accurate VAT compliance, reduce risk, and retain public trust.

________________________________________

💼 Need Help With VAT for Your Charity or NPO?

At Sheikh Anwar Accounting and Auditing LLC, we help:

• Charities with VAT registration and classification

• Identification of exempt, zero-rated, and taxable income

• Input VAT apportionment

• VAT audits and reporting compliance

📲 Contact us today for VAT solutions tailored to your non-profit mission.

📧 info@sa-auditors.com

🌐 www.sa-auditors.com