VAT and Subscription-Based Businesses

Introduction

With the rise of the subscription economy, businesses offering recurring services—whether digital (e.g., software, media streaming) or physical (e.g., food boxes, maintenance plans)—must ensure they comply with UAE VAT regulations. The VAT treatment of subscription-based business models depends on the type of supply, customer location, and billing structure.

Here we explains how VAT applies to subscription services, invoicing requirements, and common pitfalls.

________________________________________

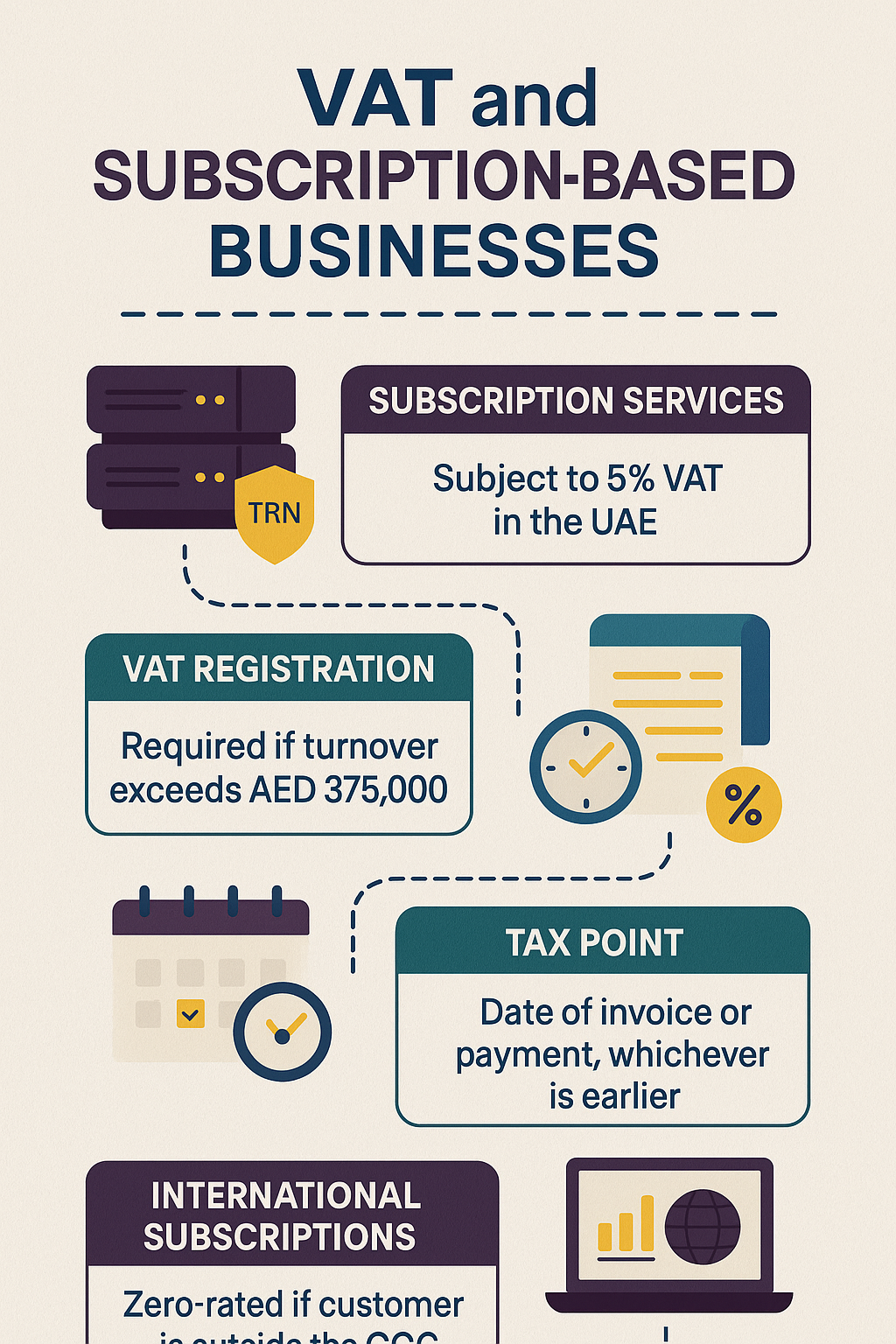

1. Are Subscription Services Subject to VAT?

Yes. Subscription-based services are subject to 5% VAT in the UAE, provided they meet the definition of a taxable supply.

This includes:

• SaaS (Software-as-a-Service) platforms

• Online streaming services

• Digital magazines or training portals

• Monthly food boxes or wellness products

• Gym memberships or coworking subscriptions

• Maintenance plans and annual service contracts

________________________________________

2. VAT Registration for Subscription Businesses

If your annual taxable turnover exceeds AED 375,000, VAT registration is mandatory. Subscription businesses must monitor:

• Recurring billing revenue

• Advance payments

• Sign-up fees

• Add-on purchases

Even freelancers or small startups offering recurring services must register if they cross the threshold.

________________________________________

3. Tax Point for Subscription Billing (Time of Supply)

The tax point (when VAT is due) is usually:

• The date of invoice

• OR the date of payment, whichever comes first

For recurring billing, this means:

• VAT is due at the start of each billing cycle, not when the service is used

E.g., a client is billed annually upfront for a 12-month software subscription → full VAT is payable at the time of billing.

________________________________________

4. VAT on Domestic vs International Subscriptions

🔹 UAE Customers (B2C or B2B)

• Charge 5% VAT

• Issue proper tax invoice

• Collect and remit VAT in VAT return

🔹 Non-UAE Customers (Outside GCC)

• If the customer is outside the UAE and unregistered in GCC, the supply of services may qualify for zero-rating (0%)

• Conditions must be met (e.g., customer location evidence, service use outside UAE)

✅ Exported digital services and SaaS to non-residents may be zero-rated

________________________________________

5. Reverse Charge for Import of Subscription Services

If a UAE VAT-registered business purchases subscription-based services from overseas (e.g., Google Workspace, Canva Pro, or Zoom):

• It must apply the Reverse Charge Mechanism (RCM)

• Declare VAT under Box 3 (output) and Box 10 (input) of VAT return

🚫 Not doing this is a common FTA audit red flag.

________________________________________

6. Input VAT Recovery

VAT-registered businesses offering subscriptions can recover input VAT on:

• Software tools

• Hosting and IT infrastructure

• Marketing and customer service tools

• Office space and salaries (if used for taxable supply)

Not recoverable:

• Expenses related to free trials, gifts, or B2C entertainment

• Non-business-related software use

________________________________________

7. VAT on Free Trials and Promotions

• Free trials → Not subject to VAT (no consideration)

• Discounted plans → VAT applies on actual amount charged

• Bundled packages → Each component must be assessed for VAT separately if different treatments apply

________________________________________

8. Invoicing Requirements for Subscriptions

For each billing cycle:

• A valid tax invoice or simplified invoice must be issued

• The invoice must show:

o Supplier’s TRN

o Description of service

o VAT amount (5%)

o Date of supply

Digital invoices are acceptable under FTA guidelines.

________________________________________

9. Common VAT Mistakes in Subscription Models

Mistake Risk

Not applying VAT to UAE subscribers Tax underpayment

Charging VAT on foreign subscribers incorrectly Client disputes

Not using reverse charge for imported tools FTA penalties

Treating free trials as taxable Overstated output VAT

Not issuing tax invoices per billing cycle Non-compliance

________________________________________

📌 Conclusion

VAT compliance for subscription-based businesses goes beyond just charging 5%—it involves understanding billing cycles, customer location, tax points, and the reverse charge mechanism. Clear documentation and proper invoicing help avoid penalties and maintain customer trust.

________________________________________

💼 Need Help With VAT for Your Subscription-Based Business?

At Sheikh Anwar Accounting and Auditing LLC, we help:

• SaaS providers and digital platforms with VAT classification

• Automated invoicing and tax compliance setup

• Cross-border VAT planning and zero-rating validation

• VAT returns and reverse charge declarations

📲 Contact us today for specialized VAT advisory.

📧 info@sa-auditors.com

🌐 www.sa-auditors.com