VAT and Cryptocurrency Transactions

Introduction

As cryptocurrencies such as Bitcoin, Ethereum, and stablecoins gain popularity in the UAE’s business landscape, questions around their tax treatment under Value Added Tax (VAT) have started to emerge. With the UAE being a growing hub for blockchain innovation and virtual assets, it is crucial for businesses and individual investors to understand the VAT implications of dealing with cryptocurrencies.

In this article, Sheikh Anwar Accounting and Auditing LLC provides a clear and practical explanation of how VAT law in the UAE applies to cryptocurrency transactions.

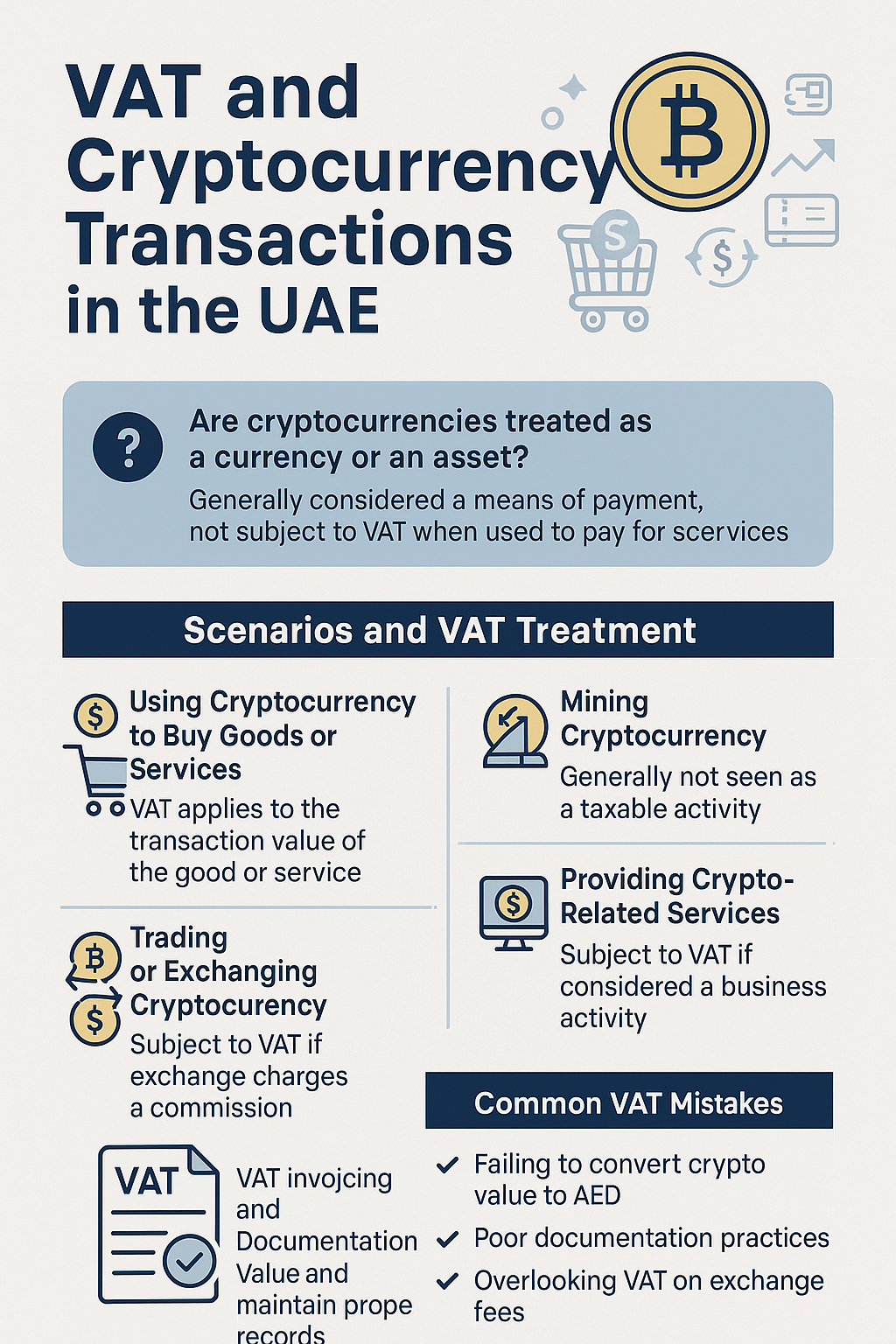

📌 Are Cryptocurrencies Treated as a Currency or an Asset Under VAT?

The UAE Federal Tax Authority (FTA) has not yet issued a comprehensive legal framework specifically for cryptocurrencies under VAT. However, based on global VAT principles (such as those followed by the UK, EU, and GCC), cryptocurrencies are generally treated as a means of payment (similar to fiat currency) when used for goods or services.

Key Point: Cryptocurrencies are not treated as goods or services, so their use as a payment method is not subject to VAT.

🔍 Scenarios and VAT Treatment

1. Using Cryptocurrency to Buy Goods or Services

When a customer uses cryptocurrency (e.g., Bitcoin) to pay for a taxable product or service:

VAT applies to the transaction value of the good or service, not the cryptocurrency.

The supplier must still issue a VAT invoice and report the value in AED.

✅ Example: If you sell a laptop for AED 5,000 worth of Bitcoin, you must issue a tax invoice for AED 5,000 + 5% VAT.

2. Mining Cryptocurrency

Mining activities involve the use of computing power to validate crypto transactions in return for newly issued coins or transaction fees.

If no direct consideration is received from another party, VAT is not applicable (non-taxable activity).

If mining is carried out as a business activity for a reward, the FTA may view it as a taxable service.

⚠️ Note: The issue of whether mining is a supply under UAE VAT remains a gray area and should be reviewed case-by-case.

3. Trading or Exchanging Cryptocurrency

Buying and selling cryptocurrencies as a speculative activity (like on exchanges) is generally not subject to VAT, unless:

The platform charges transaction or commission fees, which are VATable if the provider is UAE-based.

✅ Example: A UAE-based crypto exchange charges a 1% fee for each trade — the fee is subject to 5% VAT.

4. Providing Crypto-related Services

Businesses that offer crypto advisory, wallet management, blockchain consulting, or exchange services may be subject to VAT if:

They are established in the UAE, and

Their services fall under taxable business activities.

✅ Example: A blockchain consulting firm in Dubai charges clients for crypto wallet setup and security training — this service is VATable.

5. Receiving Payment in Cryptocurrency

If a VAT-registered business accepts cryptocurrency as payment:

The VAT must be calculated based on the AED equivalent of the crypto value at the time of transaction.

Proper documentation and valuation method must be maintained.

✅ Tip: Use a recognized crypto pricing source (like Binance or CoinMarketCap) to determine fair AED value at time of sale.

📁 VAT Invoicing and Documentation for Crypto Transactions

For businesses involved in crypto-related activities:

Issue VAT invoices in AED, even when payment is in crypto.

Maintain:

Transaction screenshots,

Exchange rate reference,

Wallet address logs,

Proof of receipt and payment.

⚠️ Non-compliance in invoicing can trigger VAT penalties during FTA audits.

❌ Common VAT Mistakes in Crypto Transactions

Treating crypto as exempt or zero-rated.

Not converting crypto value to AED for VAT invoicing.

Failing to document mining or trading activities.

Ignoring VAT on exchange fees or advisory services.

Accepting crypto payments without VAT registration.

🧠 Expert Insight: What to Expect in the Future?

As the UAE continues to embrace virtual asset regulation through authorities like VARA (Virtual Assets Regulatory Authority) in Dubai and ADGM in Abu Dhabi, the FTA is expected to:

Provide official guidance on crypto VAT treatment,

Define rules for DeFi (Decentralized Finance), NFTs, and staking rewards,

Increase audit scrutiny of businesses accepting or dealing with crypto.

🛡️ How We Can Help

At Sheikh Anwar Accounting and Auditing LLC, we assist clients with:

VAT registration for crypto businesses,

Compliance audits for exchanges and wallet platforms,

Drafting crypto VAT accounting policies,

VAT advisory for crypto investors, miners, and consultants.

📍Conclusion

While the UAE does not yet have a dedicated crypto VAT framework, existing VAT laws still apply to many crypto-related activities. Entrepreneurs and investors must proactively document transactions, understand taxable events, and stay ahead of regulatory updates to avoid penalties.

Need clarity on crypto and VAT?

Contact Sheikh Anwar Accounting and Auditing LLC for specialized advisory support.

📧 Email: info@sa-auditors.com

🌐 Website: www.sa-auditors.com

📞 Phone: +971-XXX-XXXX