UAE Corporate Tax and Accounting Standards (IFRS

Introduction

The implementation of UAE Corporate Tax (CT) from 1 June 2023 under Federal Decree-Law No. 47 of 2022 has brought significant changes to how businesses report their financial performance. One of the key pillars of Corporate Tax compliance is the use of International Financial Reporting Standards (IFRS) as the basis for accounting.

This explains the link between UAE Corporate Tax and IFRS, who must follow it, and how proper adoption impacts taxable income and compliance.

________________________________________

📚 What is IFRS?

International Financial Reporting Standards (IFRS) are globally accepted accounting principles used to prepare and present financial statements. They are designed to ensure consistency, transparency, and comparability in financial reporting across jurisdictions.

In the UAE, IFRS is the required accounting standard for most businesses, especially those subject to Corporate Tax.

________________________________________

🧾 Legal Basis for IFRS in Corporate Tax

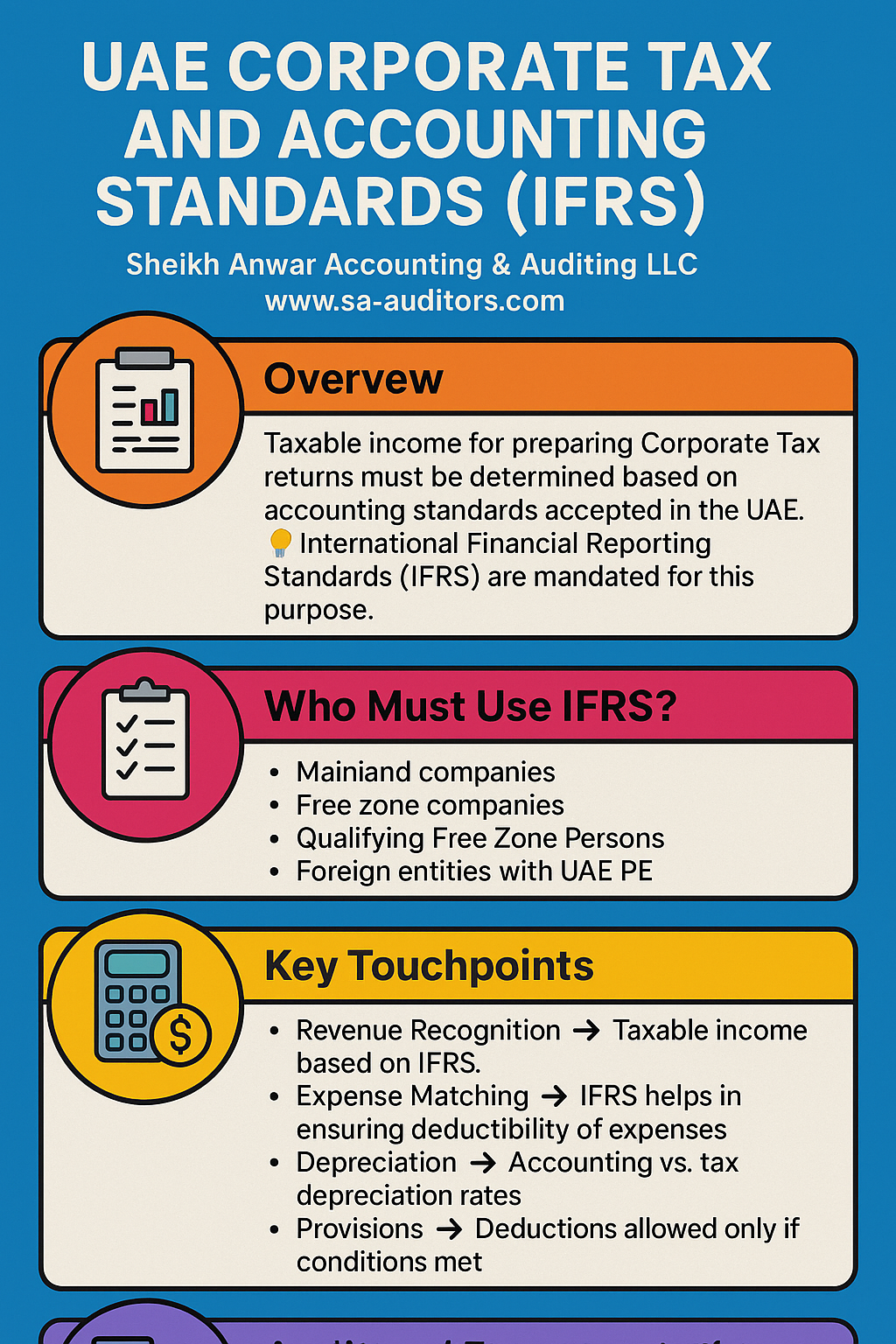

Under Article 20 of the UAE Corporate Tax Law, taxable income must be determined based on accounting standards accepted in the UAE, which refers to IFRS for most businesses.

✅ IFRS-compliant financials are mandatory for preparing corporate tax returns and calculating taxable income.

________________________________________

✅ Who Must Use IFRS?

Entity Type IFRS Required?

Mainland companies (LLCs, PJSCs, etc.) ✅ Yes

Free Zone companies (FZCO, FZE, branches) ✅ Yes

Qualifying Free Zone Persons (QFZPs) ✅ Yes, audited IFRS needed

Foreign entities with PE in UAE ✅ Yes

Natural persons (individuals in business) ❌ May use cash/other basis if < AED 3M revenue

________________________________________

🔍 IFRS and Corporate Tax – Key Touchpoints

1. Revenue Recognition

IFRS 15 governs revenue recognition from contracts. It may differ from invoicing or payment timing.

➡️ Taxable income is based on revenue recognized under IFRS, not necessarily received cash.

________________________________________

2. Expense Matching

Only expenses recognized under IFRS and wholly and exclusively incurred for business purposes are deductible.

➡️ IFRS helps establish proper expense accruals, provisions, and timing differences.

________________________________________

3. Depreciation (IFRS vs. Tax)

• IFRS uses accounting depreciation (IAS 16)

• Tax depreciation follows prescribed rates (as per Ministerial Decision No. 120 of 2023)

➡️ Differences lead to temporary timing adjustments → require Deferred Tax tracking.

________________________________________

4. Impairment Losses

IFRS 9 requires recognition of expected credit losses (ECL) on trade receivables.

➡️ These impairments may be tax deductible if justified and documented properly.

________________________________________

5. Provisions and Accruals

IFRS allows creating provisions (e.g., for warranties, bonuses, legal claims). CT allows deduction only if payment is expected and relates to business.

➡️ Need to reconcile differences during CT computation.

________________________________________

6. Leases (IFRS 16)

Under IFRS, leases are capitalized (ROU asset + liability). For CT, actual lease payments are typically deductible.

➡️ Temporary differences may arise in CT vs. accounting depreciation.

________________________________________

7. Deferred Tax Assets/Liabilities (IAS 12)

Applicable if there are timing differences between accounting and taxable income.

➡️ Not required for CT filing, but important for financial reporting accuracy.

________________________________________

📊 IFRS vs. Corporate Tax Adjustments – Common Differences

Area IFRS Treatment CT Adjustment

Depreciation Based on useful life Adjust to CT depreciation rates

Provisions Recognized per IAS 37 Allowed if related to business + probable

Revenue recognition Accrual basis (IFRS 15) Follows IFRS

Unrealized FX gains/losses Recognized in P&L Taxable/deductible based on realization rules

Related party transactions Fair value + disclosures required Must follow CT arm’s length principle

________________________________________

🧮 Example: IFRS Impact on CT Calculation

Particulars Amount (AED)

Accounting Profit (IFRS) 850,000

Add back: Non-deductible expenses 100,000

Less: Tax depreciation (70,000)

Less: Participation exemption (200,000)

Taxable Income 680,000

CT @ 9% on (680,000 - 375,000) 27,450

________________________________________

🧾 Audit and Documentation Requirements

• ✅ Maintain audited IFRS-compliant financial statements (mandatory for QFZPs and large businesses)

• ✅ Ensure consistency between EmaraTax filings and accounting books

• ✅ Track and reconcile all temporary and permanent tax adjustments

• ✅ Retain documentation for 7 years (contracts, invoices, depreciation schedules, etc.)

________________________________________

⚠️ Risks of Non-Compliance

❌ Misreporting due to non-IFRS books

❌ Errors in taxable income calculation

❌ Rejection of deductions and exemptions

❌ FTA penalties and audits

________________________________________

🧠 How Sheikh Anwar Accounting & Auditing LLC Can Help

We offer:

✅ IFRS-compliant bookkeeping and financial reporting

✅ Reconciliation of accounting and tax figures

✅ Corporate Tax computation and return filing

✅ Fixed asset register and depreciation alignment

✅ Free Zone and group structuring under IFRS

________________________________________

📞 Contact Us

📍 Sheikh Anwar Accounting & Auditing LLC

🌐 www.sa-auditors.com

📧 info@sa-auditors.com

📞 +971-XX-XXX-XXXX