Treatment of Interest Expenses

Interest expense is one of the most common financial costs for businesses—particularly those that rely on loans, credit facilities, or financing arrangements. However, under the UAE Corporate Tax regime, not all interest expenses are automatically deductible. The law provides a detailed framework for determining when and how interest costs can be claimed to reduce taxable income.

Sheikh Anwar Accounting & Auditing LLC explains the legal basis, limitations, and practical application of interest expense treatment under UAE Corporate Tax Law.

________________________________________

📜 Legal Reference

The treatment of interest expenses is governed by:

• Article 29 of Federal Decree-Law No. 47 of 2022

• Ministerial Decision No. 126 of 2023

• Ministerial Decision No. 132 of 2023 (Transfer Pricing)

________________________________________

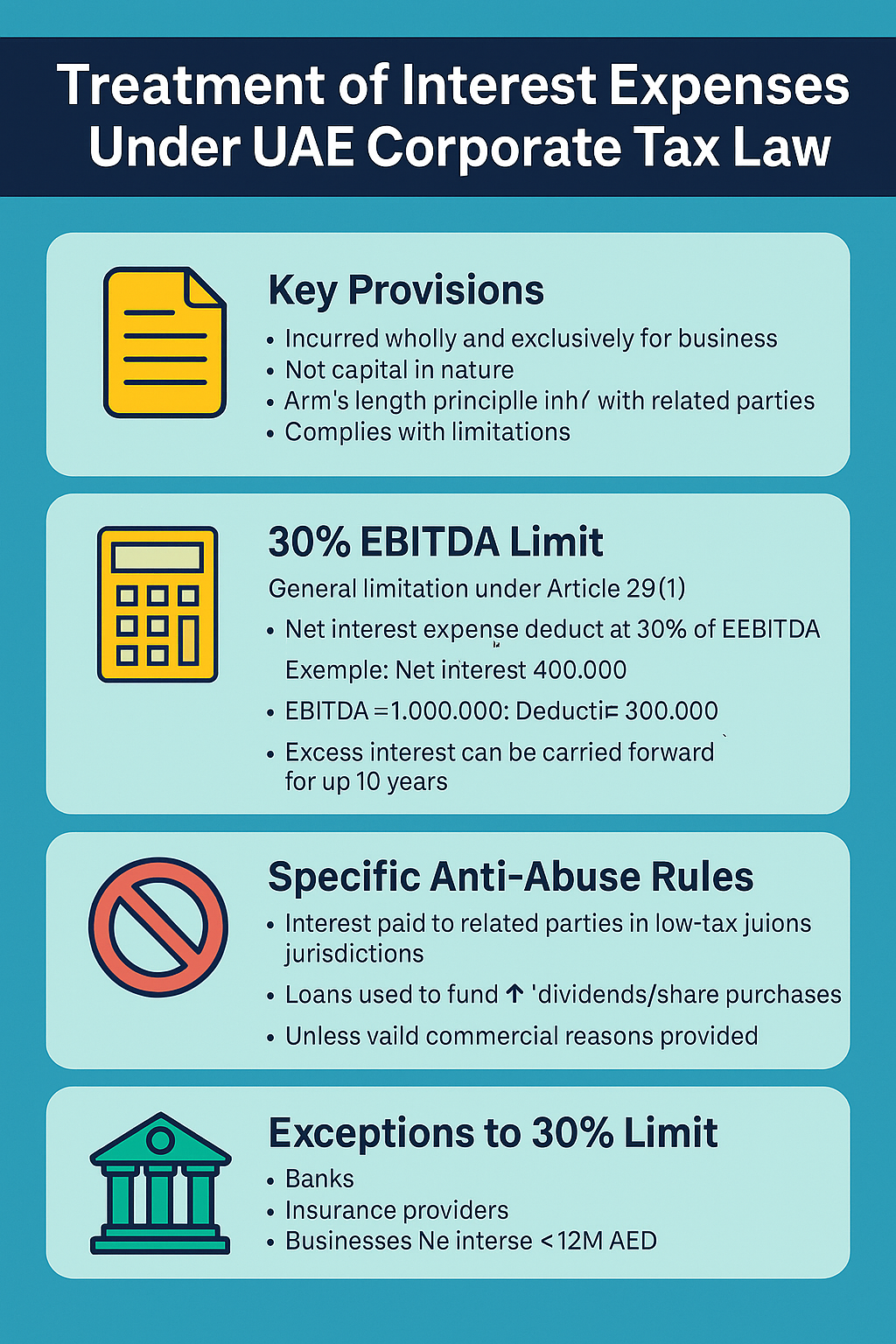

✅ When is Interest Deductible?

Interest is generally deductible if:

1. It is incurred wholly and exclusively for the purposes of the taxable business;

2. It is not capital in nature;

3. It is at arm’s length (i.e., market rate if paid to related parties);

4. It complies with thin capitalization rules and other limitations.

________________________________________

📊 General Limitation – 30% EBITDA Rule

A key limitation under Article 29(1) is the “interest deduction cap”, which limits net interest deductions to 30% of EBITDA (Earnings Before Interest, Tax, Depreciation, and Amortization).

📌 Net Interest Expense = Interest Expense – Interest Income

🧮 Example:

Item Amount (AED)

Interest Expense 500,000

Interest Income (100,000)

Net Interest Expense 400,000

EBITDA 1,000,000

30% of EBITDA 300,000

✅ Deductible Interest = AED 300,000

❌ Excess = AED 100,000 (can be carried forward for up to 10 years)

________________________________________

🏢 Who is Subject to the Cap?

All businesses except the following:

1. Banks and Insurance Companies

2. Natural Persons (individuals)

3. Businesses where net interest is below AED 12 million per year (de minimis threshold)

________________________________________

🧾 Specific Anti-Abuse Provisions

To prevent base erosion and profit shifting, additional limitations apply when:

1. Interest is paid to related parties in low-tax jurisdictions

2. The loan is used to:

o Pay dividends

o Purchase shares

o Pay capital contributions to related parties

🛑 In these cases, interest may be fully disallowed, unless the taxpayer demonstrates valid commercial reasons and no principal purpose of tax avoidance.

________________________________________

🔁 Carry Forward of Disallowed Interest

Interest exceeding the 30% EBITDA limit can be carried forward for 10 years, provided the taxpayer continues to carry on the business.

This provision ensures that businesses with initially high interest costs (e.g., due to capital investment) are not unfairly penalized.

________________________________________

🔍 Transfer Pricing & Arm’s Length Requirement

If interest is paid to related parties (such as group companies or shareholders), the following must be ensured:

✅ The rate must be comparable to market rates

✅ The financing must be commercially justified

✅ Transfer Pricing documentation (Master File and Local File) must be maintained

Failure to comply can result in reduced deductibility or penalties under UAE CT Law.

________________________________________

❌ Non-Deductible Interest Situations

• Interest on non-business loans (e.g., used for personal or capital investments)

• Excess interest beyond 30% EBITDA cap

• Interest on related party loans used for equity/debt restructuring without commercial reason

• Interest paid to tax haven-related entities with no economic substance

________________________________________

📌 Summary Table

Topic Treatment

Interest Expense Generally deductible

Net Interest Limit 30% of EBITDA

Exempt from Cap Banks, insurers, small businesses (<AED 12M)

Disallowed Situations Related-party loans for dividends or shares

Excess Interest Can be carried forward 10 years

Transfer Pricing Mandatory for related-party interest

________________________________________

🧠 Expert Insight – Sheikh Anwar Accounting & Auditing LLC

At Sheikh Anwar Accounting & Auditing LLC, we regularly assist clients with:

✅ Structuring loans to ensure deductibility

✅ Transfer pricing analysis and benchmarking of interest rates

✅ Preparing TP documentation and tax filings

✅ Avoiding disallowance under anti-abuse provisions

✅ Maximizing legitimate interest deductions

________________________________________

📞 Need Help With Interest Expense Compliance?

Let us help you optimize your tax position while ensuring full compliance.

📍 Sheikh Anwar Accounting & Auditing LLC

🌐 www.sa-auditors.com

📧 info@sa-auditors.com

📞 +971-XX-XXX-XXXX