Transfer Pricing Documentation Requirements

Introduction

With the introduction of the UAE Corporate Tax Law (Federal Decree-Law No. 47 of 2022), Transfer Pricing (TP) compliance has become a key priority for businesses, especially those involved in related-party or connected-person transactions. The Federal Tax Authority (FTA) requires companies to maintain and submit TP documentation to prove that their transactions follow the Arm’s Length Principle (ALP).

Proper documentation not only ensures compliance but also protects businesses during tax audits and preserves Free Zone tax incentives.

1. Why Transfer Pricing Documentation Matters

Demonstrates fair pricing of related-party transactions.

Reduces the risk of tax reassessments and penalties.

Provides transparency and supports UAE’s OECD-aligned tax framework.

Helps maintain 0% Free Zone Corporate Tax benefits by showing compliance.

2. Types of Transfer Pricing Documentation in the UAE

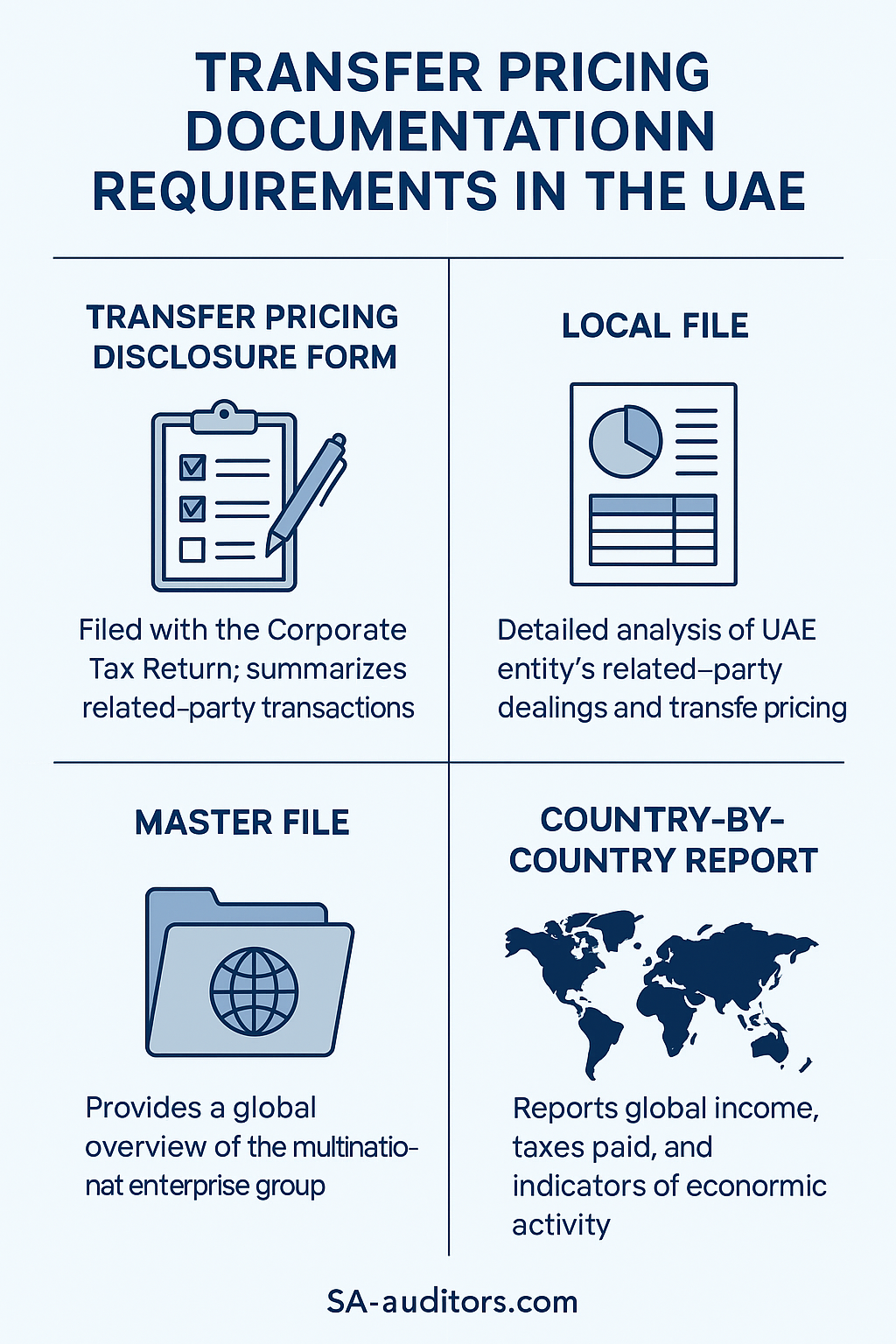

a) Transfer Pricing Disclosure Form

Filed with the annual Corporate Tax Return.

Summarises:

Related parties and connected persons.

Nature of related-party transactions.

Value of transactions during the tax year.

Required for all businesses with related-party transactions.

b) Local File

Provides a detailed analysis of the UAE entity’s related-party dealings.

Required if:

Annual revenue or related-party transactions exceed materiality thresholds set by the FTA.

Contents include:

Business and industry overview.

Functional, Assets, and Risk (FAR) analysis.

Description of controlled transactions.

Selection of TP method (CUP, TNMM, etc.).

Benchmarking studies and comparability analysis.

Financial results of the tested party.

c) Master File

Required for businesses that are part of a Multinational Enterprise (MNE) group meeting certain thresholds.

Provides a group-level perspective, including:

Global organizational structure.

Description of the group’s business operations.

Details of group intangibles and IP arrangements.

Intercompany financing arrangements.

Consolidated group financials.

d) Country-by-Country Report (CbCR)

Applicable to MNE groups with consolidated revenues of AED 3.15 billion or more.

Provides tax authorities with global income, tax, and business activity distribution.

Ensures transparency and prevents profit shifting.

3. Thresholds for Documentation

Disclosure Form: Required for all businesses with related-party transactions.

Local File & Master File: Required for large businesses meeting FTA thresholds (usually tied to revenue and transaction values).

CbCR: Required for UAE-headquartered MNEs with revenue ≥ AED 3.15 billion.

4. Record-Keeping Requirements

Businesses must retain TP documentation for at least 7 years. Records should include:

Intercompany agreements.

Benchmarking reports.

Invoices and supporting evidence of services.

Loan agreements and royalty contracts.

Any cost-sharing or management fee allocation reports.

5. Risks of Non-Compliance

Administrative Penalties by the FTA.

Profit adjustments if transactions are not at arm’s length.

Loss of Free Zone benefits (if TP compliance is not proven).

Higher scrutiny during tax audits.

6. Best Practices for Businesses

Map related-party transactions early in the financial year.

Conduct a FAR analysis to identify risks and functions.

Use benchmarking studies to justify margins.

Draft or update intercompany agreements consistent with TP documentation.

Align TP documentation with financial statements and VAT returns.

Review and update annually, or when significant business changes occur.

Conclusion

Transfer Pricing documentation is not just a compliance exercise — it’s a critical risk management tool under the UAE Corporate Tax regime. By maintaining Disclosure Forms, Local and Master Files, and CbCR where required, businesses can ensure alignment with OECD standards, protect themselves from tax disputes, and secure Free Zone benefits.

A proactive approach — with proper FAR analysis, benchmarking, and intercompany contracts — will help businesses stay audit-ready and compliant in the evolving UAE tax landscape.

✍️ By Sheikh Anwar Accounting and Auditing LLC (SA-Auditors)

📍 Dubai, United Arab Emirates

🌐 www.sa-auditors.com

| ✉️ info@sa-auditors.com