Top 10 Misconceptions About Corporate Tax

Top 10 Misconceptions About Corporate Tax

Since the introduction of Corporate Tax (CT) in the UAE, many businesses have been grappling with the new rules. While the Federal Tax Authority (FTA) has provided detailed guidelines, misconceptions and myths still circulate among business owners and even professionals. These misunderstandings can lead to compliance risks, penalties, or missed opportunities for tax optimization.

Below, we debunk the Top 10 misconceptions about UAE Corporate Tax with clarity and practical insights.

________________________________________

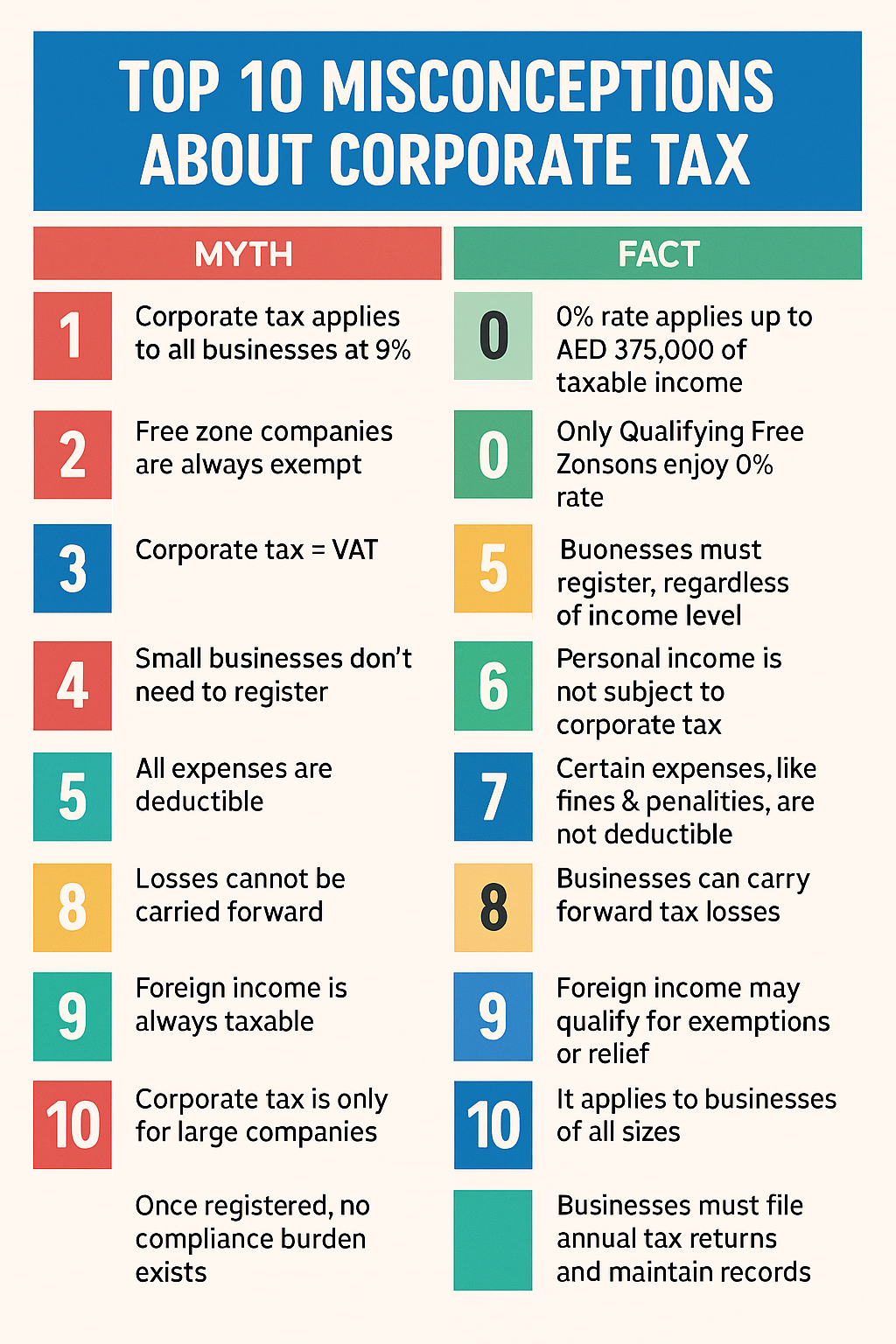

1. Corporate Tax Applies to All Businesses at 9%

Reality:

Not all businesses are taxed at 9%. The UAE Corporate Tax law provides:

• 0% on taxable income up to AED 375,000.

• 9% on taxable income exceeding AED 375,000.

• 0% for Qualifying Free Zone Persons (QFZP) on qualifying income, subject to meeting conditions.

________________________________________

2. Free Zone Companies Are Always Exempt

Reality:

Free Zone entities are not automatically exempt. Only companies that qualify as QFZPs enjoy 0% tax on qualifying income. If they earn non-qualifying income (e.g., mainland trading without meeting conditions), it may be subject to 9%.

________________________________________

3. Corporate Tax = VAT

Reality:

Many confuse Corporate Tax with VAT.

• VAT (5%) is a transaction-based indirect tax on goods and services.

• Corporate Tax is a profit-based direct tax levied on the net income of businesses.

They are separate regimes with different compliance requirements.

________________________________________

4. Small Businesses Don’t Need to Register

Reality:

Even small businesses must register for Corporate Tax with the FTA, regardless of income level. While their liability may be zero (if below the AED 375,000 threshold), non-registration can attract penalties.

________________________________________

5. Personal Income Is Taxed

Reality:

The UAE Corporate Tax does not apply to personal income earned from:

• Employment,

• Real estate held in a personal capacity,

• Investments in shares or securities,

• Bank deposits.

Only business profits are subject to CT.

________________________________________

6. All Expenses Are Deductible

Reality:

Not all expenses qualify as deductions. For example:

• Deductible: Salaries, rent, depreciation, professional fees.

• Non-Deductible: Personal expenses, fines, penalties, and donations to unapproved entities.

Proper classification is essential to avoid disputes during audits.

________________________________________

7. Losses Cannot Be Carried Forward

Reality:

Businesses can carry forward tax losses and offset them against future taxable income (subject to conditions). This helps reduce future tax liabilities and supports cash flow planning.

________________________________________

8. Foreign Income Is Always Taxable

Reality:

Foreign income is not automatically taxable. For instance:

• Dividends and capital gains from qualifying foreign subsidiaries may be exempt.

• Relief is available to avoid double taxation if the income has already been taxed abroad.

________________________________________

9. Corporate Tax Is Only for Large Companies

Reality:

Corporate Tax applies to all legal entities and natural persons conducting business in the UAE, regardless of size. Even sole proprietors and freelancers may fall within the scope if their activities qualify as a business.

________________________________________

10. Once Registered, No Compliance Burden Exists

Reality:

Corporate Tax compliance is ongoing and requires:

• Maintaining audited financial statements (for many businesses).

• Preparing and filing annual corporate tax returns.

• Ensuring transfer pricing compliance for related-party transactions.

Failure to comply can lead to administrative penalties.

________________________________________

📊 Key Takeaway

Misconceptions about Corporate Tax can expose businesses to penalties, overpayment, or compliance gaps. Business owners must distinguish facts from myths, seek professional advice, and stay updated with FTA guidelines.

________________________________________

🏢 About Us

At Sheikh Anwar Accounting & Auditing LLC (MOE Reg. Entry No. 5817 | LC4695-01), we provide expert guidance on UAE Corporate Tax, VAT, AML, and audit compliance. Our specialized team ensures that your business remains compliant while optimizing tax efficiency.

📩 Email: info@sa-auditors.com

🌐 Website: www.sa-auditors.com