Time Limits for VAT Reassessments and Corrections

Introduction

Value Added Tax (VAT) in the UAE is governed by Federal Decree-Law No. 8 of 2017 and its implementing regulations. As part of ongoing compliance, it’s crucial for businesses to understand the time limits for reassessing, correcting, and disclosing errors in VAT returns. Missing these deadlines can result in penalties, delayed refunds, or audit investigations by the Federal Tax Authority (FTA).

________________________________________

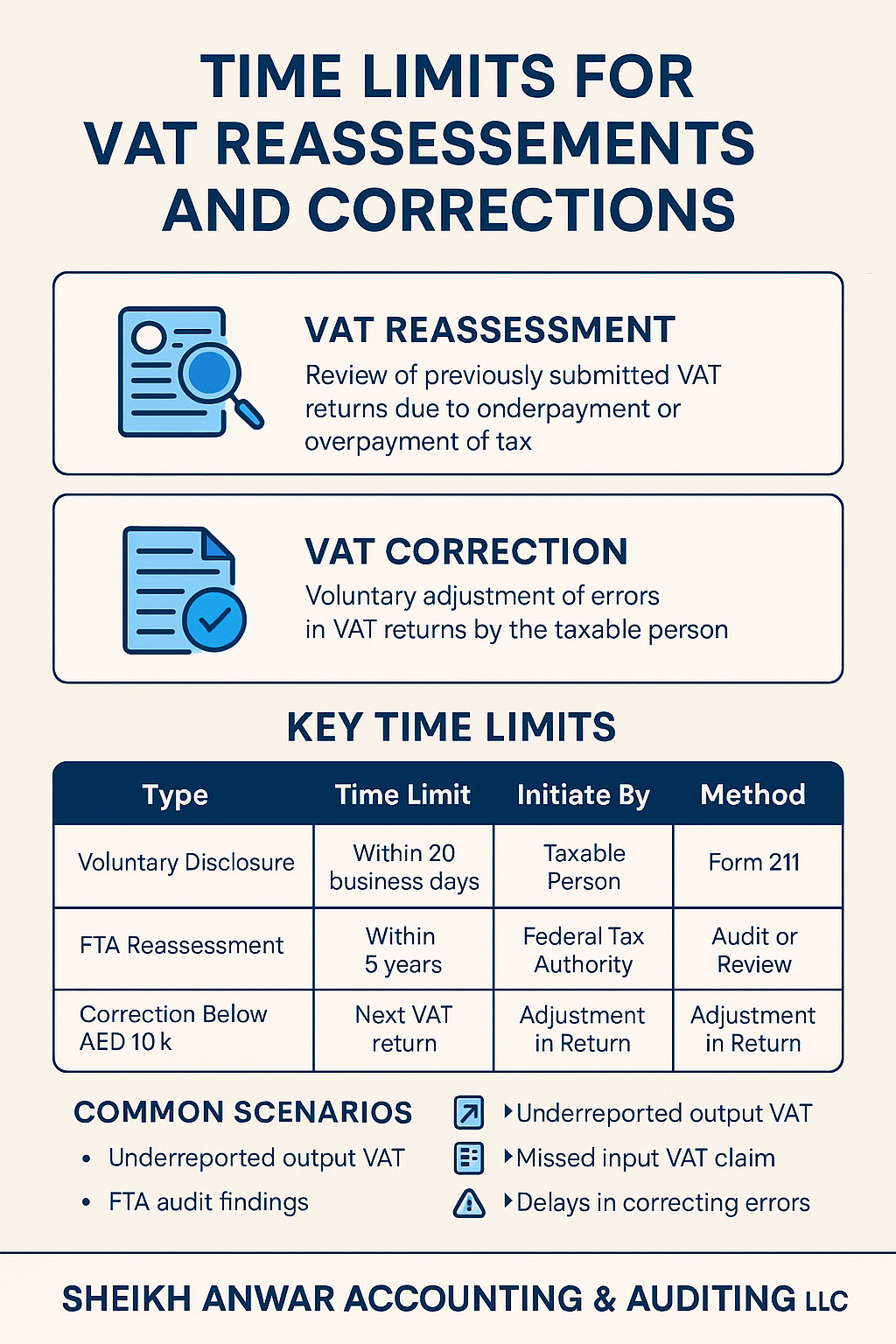

✅ What is a VAT Reassessment?

A VAT reassessment refers to the review or re-calculation of VAT liability due to:

• Errors in previously submitted returns

• Omitted transactions

• Discovery of underpayment or overpayment of VAT

• Findings during a tax audit

Both the FTA and the taxable person can initiate reassessments, depending on the scenario.

________________________________________

🔁 What is a VAT Correction?

A VAT correction is when a registered person voluntarily corrects a previously submitted VAT return due to:

• Clerical or calculation errors

• Omissions of input/output tax

• Incorrect tax treatment

If the net difference in tax payable is more than AED 10,000, the correction must be done through a Voluntary Disclosure (Form 211).

________________________________________

🕒 Key Time Limits for VAT Corrections and Reassessments

Type Time Limit Initiated By Method

Voluntary Disclosure Within 20 business days of discovering error Taxable Person Form 211 via FTA Portal

FTA Reassessment Within 5 years from the end of the tax period Federal Tax Authority Audit, investigation, or desk review

Correction Below AED 10k In the next VAT return Taxable Person Include adjustment directly

Correction Above AED 10k Within 20 business days using Voluntary Disclosure Taxable Person Form 211 required

Refund Reassessment Within 5 years of original refund application Federal Tax Authority Post-refund audit or request

________________________________________

⚠️ Common Scenarios Where Time Limits Apply

1. Underreported Output VAT

→ Must file Voluntary Disclosure within 20 days if impact > AED 10,000

2. Missed Input VAT Claim

→ Input VAT must be claimed within 6 months from the tax invoice date

3. FTA Audit Findings

→ FTA may issue a Tax Assessment within 5 years of the return date

4. Delays in Correcting Errors

→ Late disclosures invite penalties ranging from AED 3,000 to AED 5,000 plus a percentage of the tax difference

________________________________________

🧾 Penalties for Missing Correction Deadlines

Error Type Penalty (as per Cabinet Decision No. 40 of 2017)

Failure to submit disclosure AED 3,000 (first time) / AED 5,000 (repeated)

Incorrect tax treatment 50% of the tax difference

Late payment of VAT 2% per day (up to 300%)

________________________________________

🧠 Best Practices for Businesses

• Reconcile VAT returns monthly with accounting records

• Review all input/output tax entries within the return cycle

• Track invoices nearing the 6-month input VAT claim limit

• Maintain a VAT correction log with all adjustments

• Seek professional advice from Sheikh Anwar Accounting & Auditing LLC before submitting Voluntary Disclosure

________________________________________

📌 Summary

Understanding and respecting time limits for VAT corrections and reassessments is essential for avoiding fines and ensuring compliance. Whether you’ve underpaid, overclaimed, or omitted VAT, timely disclosure and accurate reassessment are your best defense.

________________________________________

🤝 Need Help with VAT Corrections or Disclosures?

At Sheikh Anwar Accounting & Auditing LLC, our experts can:

• Review your VAT return history

• Identify and quantify discrepancies

• File voluntary disclosures and amendments

• Handle FTA audits and reassessments professionally

📧 Contact us at: info@sa-auditors.com

🌐 Visit: www.sa-auditors.com

📞 Call: +971-XX-XXXXXXX