Tax Implications for Event Management Firms

Introduction

The UAE has become a global hub for events, exhibitions, and conferences, ranging from international trade shows and music festivals to corporate launches and weddings. Event management firms are at the center of this thriving industry, coordinating logistics, entertainment, and hospitality services.

With the introduction of UAE Corporate Tax (Federal Decree-Law No. 47 of 2022) alongside Value Added Tax (VAT), event management firms must now align their operations with new tax obligations. Effective tax planning ensures compliance, cost efficiency, and smooth delivery of events.

________________________________________

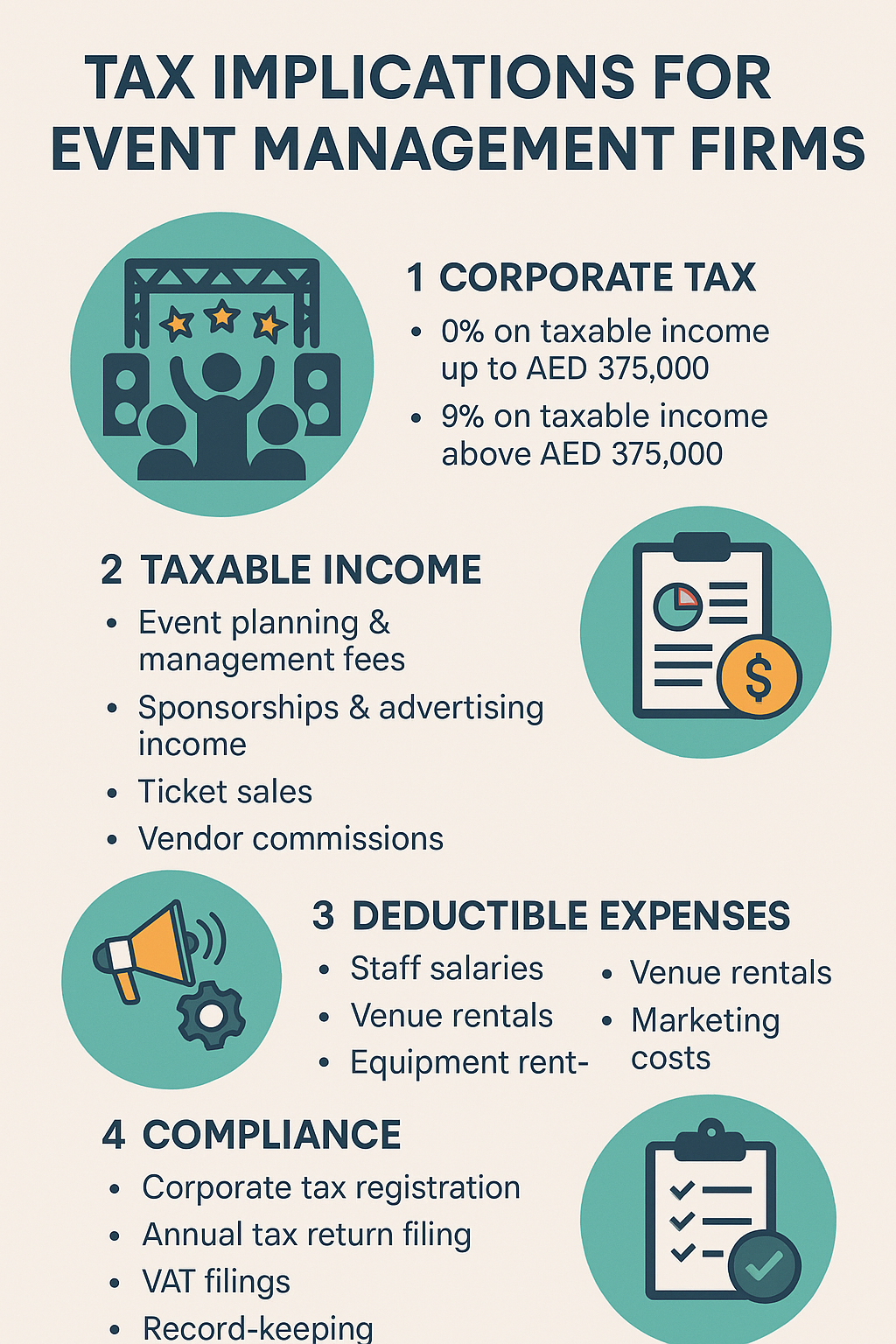

1. Applicability of Corporate Tax to Event Management Firms

• Mainland Event Companies: Fully subject to Corporate Tax on net profits.

• Free Zone Firms: May benefit from 0% Corporate Tax on qualifying cross-border services or Free Zone-to-Free Zone transactions, but 9% applies to mainland projects.

• Foreign Event Firms: Liable if they have a permanent establishment (PE) in the UAE (e.g., branch office, agent, or event infrastructure).

________________________________________

2. Corporate Tax Rates

• 0% on taxable income up to AED 375,000.

• 9% on taxable income above AED 375,000.

• Free Zone Entities: Must meet substance requirements to qualify for 0% tax. Mainland income usually taxed at 9%.

________________________________________

3. Taxable Income for Event Firms

Event management firms typically earn income from:

• Event Planning & Management Fees.

• Sponsorships & Advertising Income.

• Ticket Sales for concerts, exhibitions, or conferences.

• Vendor Commissions from catering, decoration, or sound/light suppliers.

• Corporate Launches & Private Events (weddings, parties).

All these income streams are considered taxable unless specifically exempt.

________________________________________

4. Deductible vs. Non-Deductible Expenses

Event companies incur significant project-based costs.

• Deductible Expenses:

o Staff salaries and temporary event staff.

o Venue rentals and logistics.

o Stage, lighting, and sound equipment rentals.

o Marketing and advertising costs.

o Travel and accommodation for event teams.

o Sponsorship costs for promotional events.

• Non-Deductible Expenses:

o Regulatory fines.

o Personal or unrelated expenses.

o Certain entertainment expenses not tied to client events.

________________________________________

5. VAT Implications for Event Firms

VAT has a significant role in the event industry:

• Standard 5% VAT applies on event tickets, sponsorships, and services.

• Zero-Rated: Exported services to clients outside UAE (subject to conditions).

• Reverse Charge Mechanism (RCM): Applies to cross-border services procured for UAE events.

VAT must be reconciled with Corporate Tax to ensure accurate filings.

________________________________________

6. Free Zone Benefits for Event Companies

Event firms in Free Zones such as DIFC, Dubai Media City, or TwoFour54 enjoy advantages:

• 0% Corporate Tax on qualifying income (e.g., cross-border events).

• Access to specialized media infrastructure.

• Lower operational costs for international productions.

• Substance requirements (local staff, office, governance) must be satisfied.

________________________________________

7. Transfer Pricing in Large Event Groups

Event management groups with multiple subsidiaries or international operations face Transfer Pricing (TP) obligations:

• Related-party sponsorship deals.

• Intercompany event services.

• Shared marketing and IP usage (branding, ticketing platforms).

• Firms must follow the arm’s length principle and prepare TP documentation where thresholds apply.

________________________________________

8. Compliance Requirements

• Corporate Tax Registration with the Federal Tax Authority (FTA).

• Annual Corporate Tax Return within 9 months of the financial year-end.

• VAT Filings (quarterly/monthly depending on turnover).

• Audited Financial Statements required for many medium and large firms.

• Record-Keeping: Contracts, invoices, and sponsorship deals must be kept for at least 7 years.

________________________________________

9. Strategic Tax Planning for Event Management Firms

• Expense Optimization: Ensure all allowable costs are properly recorded.

• Leverage Free Zone Benefits: Route international event services via Free Zone entities.

• Loss Relief: Carry forward tax losses to offset future taxable profits.

• ERP & Technology: Integrate event booking systems with VAT and Corporate Tax compliance.

• Cross-Border Structuring: Use favorable structures for international event collaborations.

________________________________________

Conclusion

Event management firms in the UAE face multiple tax obligations under the new Corporate Tax regime and VAT. While the 9% rate is competitive, compliance requires accurate record-keeping, cost control, and careful structuring of income sources.

By adopting robust tax planning strategies, leveraging Free Zone incentives, and ensuring proper VAT & Corporate Tax reconciliation, event companies can remain compliant while delivering memorable experiences in the UAE’s thriving events industry.

________________________________________

✍️ By Sheikh Anwar Accounting and Auditing LLC (SA-Auditors)

📍 Dubai, United Arab Emirates

🌐 www.sa-auditors.com | ✉️ info@sa-auditors.com