Start-Up Expenses and Corporate Tax

Introduction

Setting up a new business involves various preliminary expenses—legal fees, licensing, consultancy, market studies, branding, and office setup. These costs, known as start-up expenses, are often significant. As the UAE moves forward with its Corporate Tax regime under Federal Decree-Law No. 47 of 2022, a common question arises:

Are start-up expenses tax deductible under UAE Corporate Tax Law?

Sheikh Anwar Accounting and Auditing LLC explains the tax treatment of start-up costs, eligibility for deductions, and best practices for recording and reporting them to ensure compliance.

________________________________________

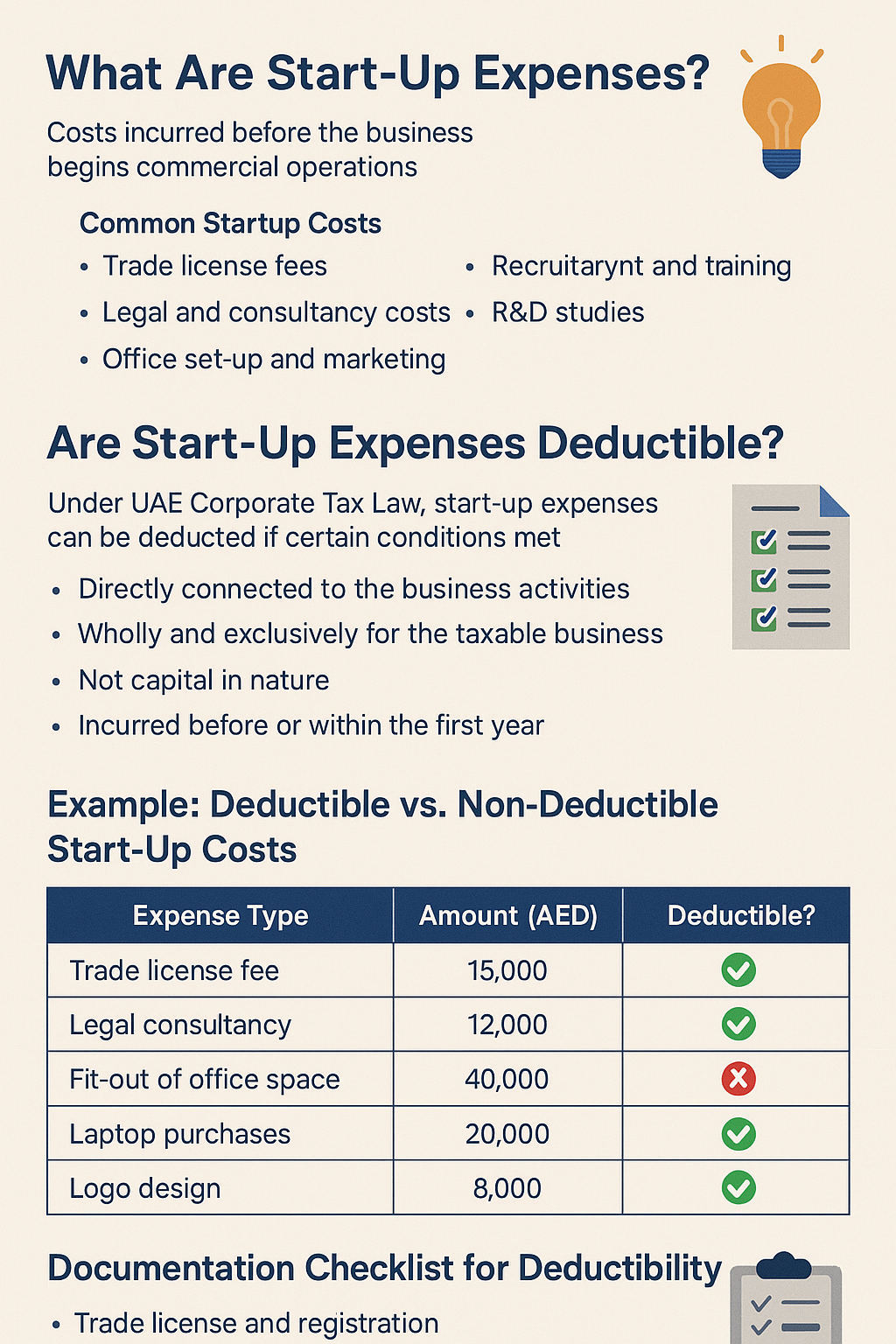

📜 What Are Start-Up Expenses?

Start-up expenses are costs incurred before the business begins commercial operations. These are necessary to establish the business and make it operational.

Common Start-Up Costs Include:

• Trade license and company registration fees

• Initial legal and professional consultancy fees

• Premises set-up and renovations

• Branding, website development, and marketing

• Staff recruitment and training

• Government approvals and regulatory fees

• Initial R&D or feasibility studies

________________________________________

✅ Are Start-Up Expenses Deductible?

Yes—UAE Corporate Tax Law allows the deduction of start-up expenses provided they meet certain conditions:

Deductibility Conditions:

1. ✅ The expenses are directly connected to the business activities

2. ✅ They are incurred wholly and exclusively for the taxable business

3. ✅ They are not capital in nature (e.g., purchase of land, building)

4. ✅ The expenses are incurred before the first tax period begins or within the first year

5. ✅ Proper accounting treatment and documentation is in place

📌 Key Rule: If the expense results in the acquisition of a long-term asset, it should be capitalized and depreciated rather than fully expensed.

________________________________________

🧾 Legal Framework

Relevant references include:

• Federal Decree-Law No. 47 of 2022 (Articles on deductible expenditures)

• Ministerial Decision No. 114 of 2023 – Conditions and categories of deductible expenses

• IFRS Standards – For accounting treatment of pre-operating costs and deferred assets

________________________________________

🧮 Example: Deductible vs. Non-Deductible Start-Up Costs

Expense Type Amount (AED) Deductible? Notes

Trade license fee 15,000 ✅ Yes Administrative start-up cost

Legal consultancy for company formation 12,000 ✅ Yes Professional services for business setup

Fit-out of office space 40,000 ❌ No Capital expense; depreciated over years

Laptop purchases for new employees 20,000 ❌ No (fully) Capitalized and depreciated

Logo and website design 8,000 ✅ Yes Intangible service, deductible if not capitalized

Initial staff recruitment fees 10,000 ✅ Yes Allowed if linked to first-year operations

________________________________________

🏢 Capital vs. Revenue Treatment

Capital Start-Up Costs Revenue (Deductible) Start-Up Costs

Purchase of machinery, computers, or office furniture Legal, accounting, or consulting fees

Leasehold improvements or renovations Marketing and branding services (non-capital)

Development of long-term intellectual property Temporary business licenses or approvals

⚠️ Capital start-up costs are not deducted immediately—they are subject to depreciation/amortization rules under UAE Corporate Tax Law.

________________________________________

📂 Documentation Checklist for Deductibility

Businesses must retain the following to support the deduction of start-up costs:

• Trade license and registration documents

• Vendor contracts and invoices

• Bank payment confirmations

• Board resolution or business plan showing timeline of start-up

• Fixed asset register (for capital items)

• Accounting journal entries classifying the expense correctly

Sheikh Anwar Accounting and Auditing LLC helps businesses structure and categorize their initial costs to optimize tax compliance.

________________________________________

💡 Special Consideration: Pre-Incorporation Expenses

Expenses incurred before legal incorporation may still be deductible if later reimbursed by the business and properly documented. For instance, a founder may pay for legal consultancy and later get reimbursed by the company. This must be:

• Authorized via board resolution

• Documented with receipts/invoices in the founder’s name

• Reimbursed within a reasonable time

________________________________________

🧠 Pro Tip: Use a Deferred Expense Account

Many companies choose to capitalize start-up expenses as deferred expenses and amortize them over 3–5 years. This is particularly helpful when large one-time expenses need to be spread out for better tax planning.

Our team at Sheikh Anwar Accounting and Auditing LLC assists in implementing this approach with compliance to IFRS and tax rules.

________________________________________

📣 Final Thoughts

Start-up costs are a necessary investment in your business’s foundation. Fortunately, the UAE Corporate Tax Law provides a structured and business-friendly approach to deducting these costs. However, to take full advantage, you must:

• Understand which costs qualify as deductible

• Separate capital and non-capital expenses

• Maintain detailed supporting documentation

• Apply correct accounting and tax treatment

________________________________________

📩 Starting a business in the UAE? Need to ensure your pre-operating expenses are compliant and deductible?

📧 Email: info@sa-auditors.com

🌐 Website: www.sa-auditors.com