Reverse Charge vs Input VAT Recovery

Introduction

Freelancers, startups, and growing businesses often find UAE VAT compliance tricky—especially when dealing with cross-border transactions. Two commonly misunderstood concepts in this context are:

• The Reverse Charge Mechanism (RCM)

• Input VAT Recovery

While both deal with VAT accounting and reporting, they serve different purposes and apply under different circumstances. At Sheikh Anwar Accounting & Auditing LLC, we break down the distinction in simple yet technical terms to help you stay compliant and avoid costly errors.

________________________________________

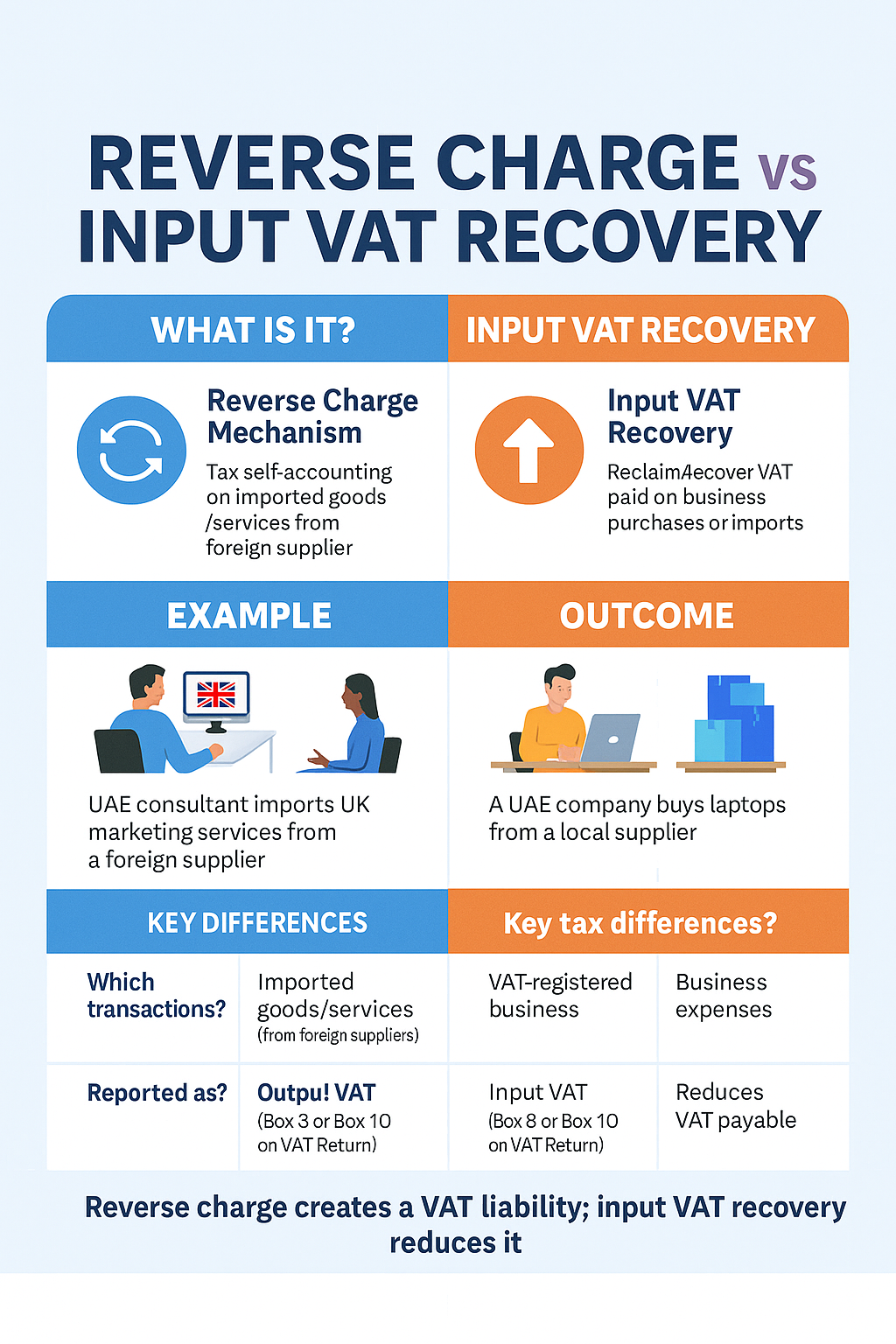

🔁 What is Reverse Charge Mechanism (RCM)?

The Reverse Charge Mechanism is a VAT treatment where the recipient (importer) of a service or good is liable to account for VAT on behalf of the foreign supplier.

🧩 Why is it needed?

RCM is used when:

• The supplier is not registered for VAT in the UAE

• The recipient is VAT-registered in the UAE

• The transaction involves imported services or goods

This ensures VAT is collected even when the supplier is outside the UAE jurisdiction.

📜 Legal Reference:

Federal Decree-Law No. 8 of 2017, Article 48:

The recipient of a taxable supply shall be responsible for calculating and reporting the tax under RCM if the supplier is not UAE VAT-registered.

________________________________________

💼 Example 1: Reverse Charge in Action

A Dubai-based VAT-registered consultant purchases marketing services from a UK agency. The UK supplier is not VAT-registered in the UAE.

✅ The UAE consultant must:

• Self-account for 5% VAT on the value of the invoice

• Report it as output VAT under Box 3 in the VAT return

________________________________________

💰 What is Input VAT Recovery?

Input VAT Recovery refers to the mechanism through which a VAT-registered person can reclaim VAT paid on eligible business expenses or imports.

This is a separate process from RCM, and applies to both:

• VAT paid to UAE suppliers

• VAT accounted for under RCM (in some cases)

________________________________________

✅ Conditions for Input VAT Recovery:

According to Article 54 of the UAE VAT Law, the following must be satisfied:

• The purchased goods/services are used for taxable supplies

• The VAT invoice is properly documented

• The expense is not explicitly blocked (e.g., entertainment, motor vehicles for personal use)

________________________________________

📤 Example 2: Input VAT Recovery Scenario

A VAT-registered software company purchases laptops for developers and pays AED 5,000 in VAT to a local supplier.

✅ If the laptops are used for taxable activities:

• The AED 5,000 VAT is reported as Input VAT under Box 10 in the VAT return

• It reduces the net VAT payable

________________________________________

🔄 How RCM & Input VAT Recovery Interact

In many RCM transactions, the same person:

• Pays the output VAT via self-assessment (RCM)

• Recovers the input VAT in the same return (if eligible)

🔄 Example 3: RCM + Input VAT Recovery

• A UAE design firm buys online design software from the USA for AED 10,000

• It applies RCM (5% of AED 10,000 = AED 500 output VAT)

• Since it uses the software for its taxable services, it can recover the same AED 500 as input VAT

📊 The net effect on the VAT return = Zero, but reporting is mandatory.

________________________________________

🚫 Common Mistakes to Avoid

Mistake Why It's a Problem

Failing to apply RCM on imports Leads to underreporting and penalties

Trying to recover VAT on ineligible expenses Risk of rejection during audit

Confusing RCM as a recovery mechanism RCM creates a liability first; recovery is separate

________________________________________

🧠 Summary: Key Differences

Feature Reverse Charge Mechanism (RCM) Input VAT Recovery

Purpose Tax self-accounting for imports Reclaim tax paid on purchases

Applies to Imported goods/services from non-VAT suppliers Eligible business expenses

Requires VAT registration? Yes Yes

Reported as Output VAT (Box 3) Input VAT (Box 10)

Net tax effect Often neutral if recovered Reduces VAT payable

________________________________________

🧾 Final Thoughts from Sheikh Anwar Accounting & Auditing LLC

Understanding the distinction between RCM and Input VAT Recovery is essential for accurate VAT reporting and audit readiness. While they often appear together in cross-border transactions, they play different roles and must be accounted for correctly in the VAT return.

🔍 Need help reviewing your VAT return or understanding RCM implications?

📩 Contact us today at info@sa-auditors.com or visit www.sa-auditors.com