Restructuring Offshore vs. Onshore Entities

As global tax laws evolve and compliance becomes stricter, businesses are rethinking how they structure their entities. One of the most critical decisions in restructuring is whether to operate through offshore entities or onshore entities. Each option offers unique tax, regulatory, and strategic advantages, but the wrong choice can expose a business to heavy tax liabilities or compliance risks.

This explores the differences between offshore and onshore entities, their tax implications, and when businesses should consider restructuring.

________________________________________

What are Offshore and Onshore Entities?

Offshore Entity

• A company incorporated in a jurisdiction outside the country of residence of its owners or primary operations.

• Commonly set up in tax-neutral jurisdictions such as Cayman Islands, British Virgin Islands (BVI), or Mauritius.

• Typically used for asset protection, international trading, or investment holding.

Onshore Entity

• A company incorporated in the same jurisdiction where it primarily operates.

• For UAE businesses, this means either a Mainland LLC or a Free Zone company.

• Designed for businesses engaged in local trade, services, and regulated industries.

________________________________________

Why Businesses Restructure Entities

1. Tax Efficiency – Optimize tax liability under UAE Corporate Tax and global tax treaties.

2. Compliance with ESR & BEPS – Meet Economic Substance Regulations and OECD’s Base Erosion and Profit Shifting (BEPS) rules.

3. Market Access – Offshore entities may ease global expansion, while onshore entities allow local UAE market access.

4. Risk Management – Offshore structures protect assets; onshore entities ensure local credibility.

5. Exit Planning – Preparing for IPO, M&A, or succession requires proper structuring.

________________________________________

Tax Implications of Offshore vs. Onshore Restructuring

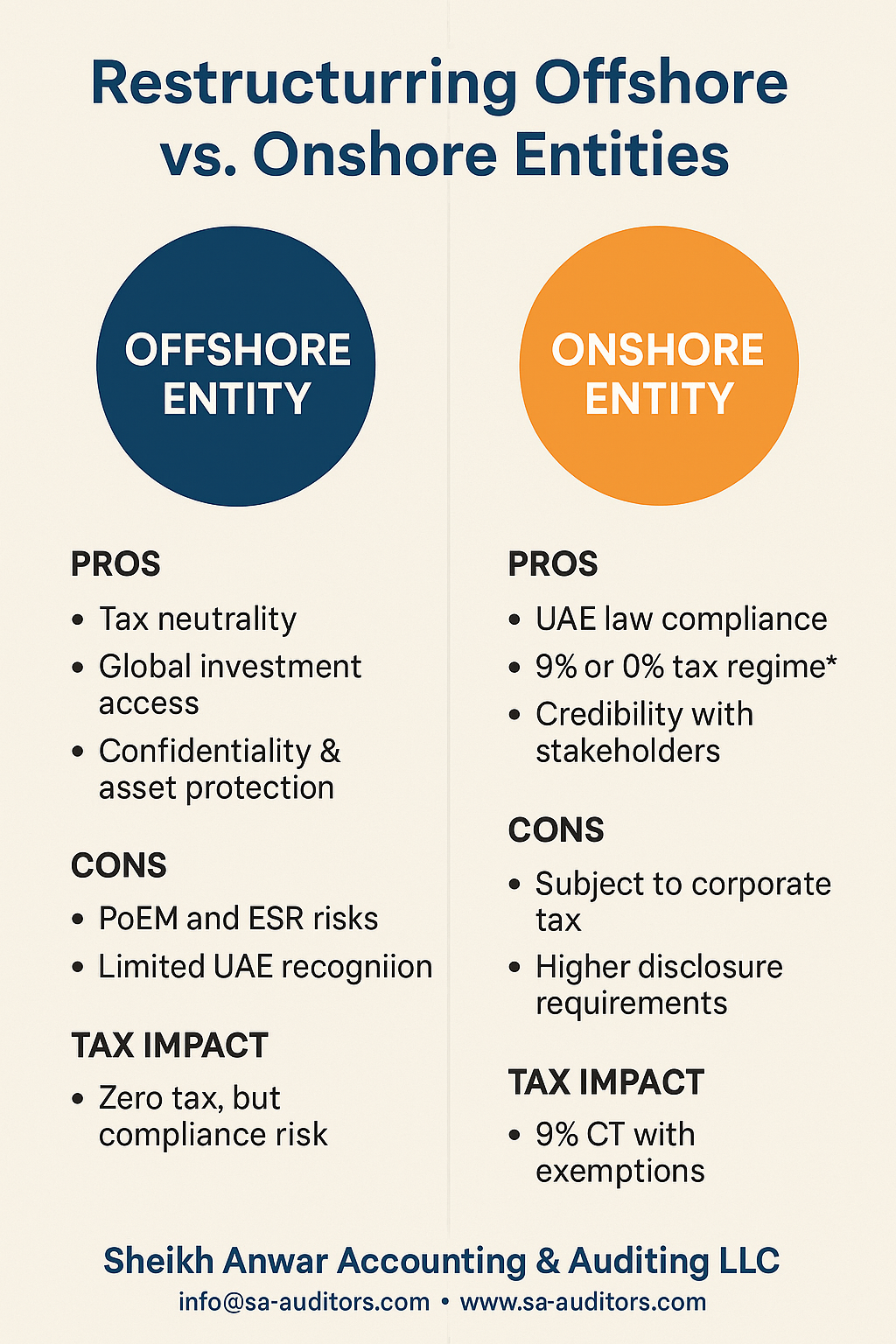

1. Offshore Entities

• Pros:

o Tax neutrality (low or zero corporate tax).

o Access to global investment opportunities.

o Confidentiality and asset protection.

• Cons:

o Risk of PoEM (Place of Effective Management) in India or other countries where promoters reside, leading to taxation there.

o Non-compliance with ESR can attract penalties.

o Limited recognition by UAE banks and regulators for operating businesses.

________________________________________

2. Onshore Entities (Mainland & Free Zones in UAE)

• Pros:

o Clear compliance under UAE law.

o Eligible for 9% corporate tax regime with exemptions (0% for Qualifying Free Zone Persons).

o Stronger credibility with banks, regulators, and clients.

o Access to Double Tax Treaties signed by the UAE.

• Cons:

o Subject to corporate tax (except qualifying Free Zone income).

o Higher compliance and reporting requirements (audit, VAT, ESR, transfer pricing).

o Disclosure requirements reduce confidentiality compared to offshore.

________________________________________

When to Choose Offshore vs. Onshore

Scenario Offshore Entity Onshore Entity

Holding & IP Structures Best for global holdings & IP planning Suitable if UAE-based operations manage the IP

International Expansion Flexible for cross-border investments UAE Free Zones offer tax-efficient regional hubs

Local Business Operations Not practical Mandatory for trading/service businesses in UAE

Tax Planning Zero-tax advantage, but risky under PoEM/ESR 9% CT, with Free Zone 0% option for qualifying income

Exit/IPO Often needs restructuring before listing Preferred structure for IPO or M&A deals

________________________________________

Risks to Consider

• Anti-Avoidance Rules (GAAR): Aggressive offshore tax planning may be challenged.

• Banking Restrictions: Offshore companies face difficulty opening UAE bank accounts.

• Regulatory Scrutiny: ESR non-compliance can attract penalties in both offshore and UAE jurisdictions.

• Reputation Risk: Offshore-only structures may be viewed negatively by investors or regulators.

________________________________________

Best Practices in Entity Restructuring

1. Assess Business Needs First – Tax benefits must align with commercial realities.

2. Use Hybrid Structures – Combine offshore holding with UAE onshore operational subsidiaries.

3. Substance Matters – Ensure board meetings, management, and staff are in the chosen jurisdiction.

4. Plan for Exit – Consider how investors or buyers will perceive your structure.

5. Engage Experts – Work with tax, legal, and compliance professionals to avoid costly mistakes.

________________________________________

Conclusion

Restructuring between offshore and onshore entities is not just about tax—it’s about creating a sustainable, compliant, and growth-oriented structure.

• Offshore entities offer tax neutrality but carry compliance and reputation risks.

• Onshore entities provide legitimacy, access to tax treaties, and long-term stability under UAE Corporate Tax.

The right balance often lies in hybrid structures—offshore for holding and international assets, onshore for operations and compliance. With careful planning, businesses can achieve both tax efficiency and regulatory confidence.

________________________________________

📌 Sheikh Anwar Accounting & Auditing LLC

Approved Auditor – UAE Ministry of Economy (Entry No. 5817)

📧 info@sa-auditors.com

🌐 www.sa-auditors.com