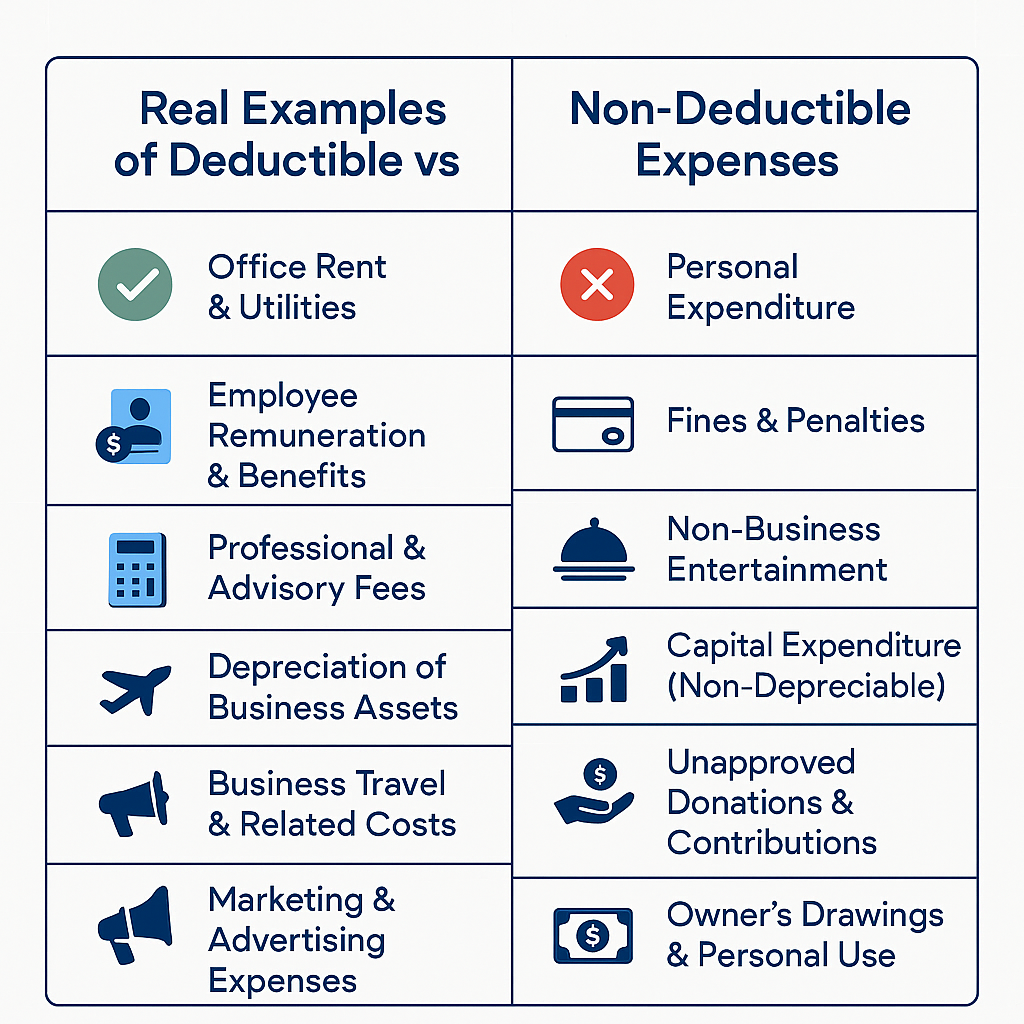

Real Examples of Deductible vs Non-Deductible Expenses

Real Examples of Deductible vs Non-Deductible Expenses

Accurate classification of business expenses is a cornerstone of effective financial management and tax compliance. The distinction between deductible and non-deductible expenses directly impacts taxable income, profitability, and audit readiness. Below, we highlight real-world examples to illustrate this difference with practical clarity.

________________________________________

✅ Deductible Business Expenses

These are expenses that are ordinary, necessary, and directly related to generating business income. They are recognized by tax authorities and reduce the overall taxable base.

1. Office Rent & Utilities

• Example: A trading firm in Dubai pays AED 15,000 monthly rent and utilities for its Business Bay office. Both are fully deductible, as they are incurred for business operations.

2. Employee Remuneration & Benefits

• Example: Salaries, end-of-service benefits, and medical insurance provided to employees are deductible, as they represent legitimate business obligations.

3. Professional & Advisory Fees

• Example: Engaging auditors, corporate tax consultants, or legal advisors to ensure compliance. These professional fees are deductible as they are essential for lawful business conduct.

4. Depreciation of Business Assets

• Example: A gold trading company acquires a weighing machine for AED 50,000. Depreciation charged annually is deductible, in line with accounting standards.

5. Business Travel & Related Costs

• Example: Travel to London to attend an international jewelry exhibition. Airfare, accommodation, and exhibition participation fees are deductible when documented as business-related.

6. Marketing & Advertising Expenses

• Example: A software company invests AED 20,000 in online campaigns to promote its ERP system. These promotional costs are deductible since they directly contribute to revenue generation.

________________________________________

❌ Non-Deductible Expenses

These are costs that cannot be claimed as tax deductions, often due to their personal nature, non-compliance elements, or classification as capital rather than operating expenses.

1. Personal Expenditure

• Example: The business owner charges a family vacation to company accounts. Such personal expenses are not deductible, even if paid from business funds.

2. Fines & Penalties

• Example: A logistics company pays AED 50,000 in penalties for late VAT filing. Regulatory fines are not deductible under UAE tax law.

3. Non-Business Entertainment

• Example: Hosting a private dinner for friends at a luxury hotel and recording it as a company expense. Since it does not serve a business purpose, it is non-deductible.

4. Capital Expenditure (Non-Depreciable)

• Example: Acquisition of land worth AED 2 million for a warehouse. The cost of land itself is not deductible (only depreciation on constructed assets may qualify).

5. Unapproved Donations & Contributions

• Example: Contributing AED 100,000 to an overseas NGO without authorization. Only donations to approved and qualifying entities are deductible.

6. Owner’s Drawings & Personal Use

• Example: The owner withdraws AED 30,000 from business funds for household expenses. Such drawings represent personal use and are not deductible.

________________________________________

📊 Key Insights

• Deductible expenses must be business-related, necessary, and well-documented.

• Non-deductible expenses typically fall under personal, penal, or unapproved categories.

• Proper classification safeguards against penalties, tax reassessments, and reputational risks.

________________________________________

🏢 About Us

At Sheikh Anwar Accounting & Auditing LLC (MOE Reg. Entry No. 5817 | LC4695-01), we provide specialized advisory in Corporate Tax, VAT, AML compliance, and audit services across the UAE. Our expertise ensures that clients—especially those in the gold, diamond, and trading sectors—classify expenses correctly, optimize tax positions, and remain fully compliant with evolving regulations.

📩 Email: info@sa-auditors.com

🌐 Website: www.sa-auditors.com