RCM on Gold and Precious Metals

Introduction

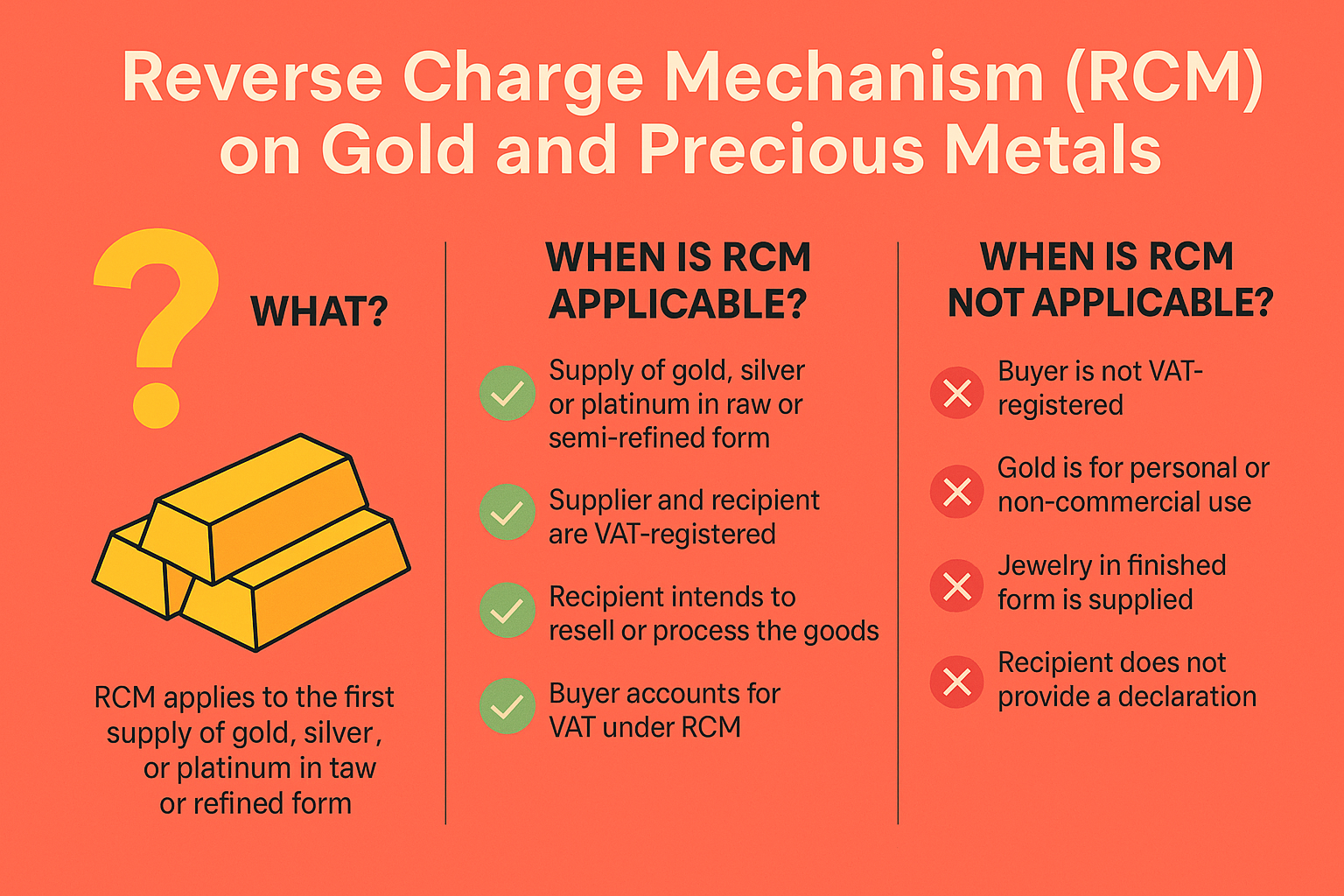

The gold and precious metals sector in the UAE is subject to specific VAT rules due to its high-value nature and vulnerability to tax evasion. One such provision is the Reverse Charge Mechanism (RCM), which shifts the VAT liability from the supplier to the recipient under certain conditions.

It provides an in-depth explanation of how RCM applies to gold and precious metals in the UAE, along with legal references, conditions, and practical examples.

________________________________________

🔍 Legal Basis for RCM on Gold and Precious Metals

The application of RCM in this sector is governed by:

• Federal Decree-Law No. 8 of 2017 on VAT

• Cabinet Decision No. 25 of 2018 (amending Cabinet Decision No. 59 of 2017)

• FTA Public Clarifications VATP016 and VATP029

These rules aim to combat fraud and ensure transparency in the gold and precious metals trade.

________________________________________

🧾 What Supplies Are Covered?

The RCM applies specifically to the first supply of the following, when made in raw form or refined form:

• Gold

• Silver

• Platinum

Condition: The supply must be made to a VAT-registered recipient who intends to resell or further process the goods.

________________________________________

✅ When is RCM Applicable on Gold?

RCM applies if all the following conditions are met:

1. Type of Goods: Supply involves gold, silver, or platinum in raw or semi-refined form.

2. Supplier: VAT-registered in the UAE.

3. Recipient: Also VAT-registered and declares in writing that the purchase is for:

o Resale, or

o Manufacturing or production of gold/similar products.

4. No VAT Charged by Supplier: The supplier does not charge VAT on the invoice.

5. VAT Reported by Buyer: The recipient self-accounts for VAT in their VAT return under Box 3 and Box 10 of VAT 201.

________________________________________

🛑 When is RCM Not Applicable?

RCM does not apply in these situations:

• The recipient is not VAT registered

• The gold is used for personal or non-commercial use

• The supply is for jewellery in finished form

• The recipient does not issue the declaration that the supply is for resale or manufacturing

• The supplier and recipient are connected persons with non-arm’s length pricing

In these cases, Forward Charge applies, and the supplier must charge VAT on the invoice.

________________________________________

✍️ Format of Declaration (from Buyer)

To apply RCM, the recipient must provide a declaration (usually on company letterhead) stating:

“We confirm that the purchase of gold in raw/refined form from [Supplier Name] will be used in the course of our business for resale or production purposes. We undertake to self-account for VAT under the Reverse Charge Mechanism in accordance with Cabinet Decision No. 25 of 2018.”

________________________________________

📊 Practical Example

Scenario:

• A gold refiner in Dubai sells 10 kg of 24K gold bars to a VAT-registered wholesaler.

• The wholesaler provides a declaration that the gold is for resale.

• The refiner does not charge VAT on the invoice.

• The wholesaler self-accounts for VAT (AED 100,000 on AED 2 million gold) and claims it as input tax in the same return (if eligible).

________________________________________

🔎 Key Compliance Points

• Keep the recipient’s declaration on file.

• Do not issue tax invoice with VAT if RCM applies.

• Ensure the TRN of the buyer is valid and active.

• Clearly state “VAT to be accounted for by recipient under RCM” on the invoice.

• RCM is applicable only for business-to-business transactions.

________________________________________

⚖️ FTA Clarifications

According to FTA VATP016:

“The supplier must not charge VAT on the supply if the recipient provides a written confirmation that the goods are being acquired for resale or production. The burden of proof is on the supplier to maintain records.”

________________________________________

🧠 Summary Table: When Does RCM Apply on Gold?

Criteria RCM Applies RCM Does Not Apply

Buyer VAT-registered ✅ Yes ❌ No

Declaration provided ✅ Yes ❌ No

Gold in raw/refined form ✅ Yes ❌ No (e.g., jewellery)

Intended for resale/production ✅ Yes ❌ No (e.g., investment)

Personal use ❌ No ✅ Yes

________________________________________

📌 Conclusion

The Reverse Charge Mechanism on gold and precious metals is a critical compliance area for businesses in the UAE dealing with raw materials. Proper application of RCM reduces the risk of fraud and maintains VAT neutrality.

💡 If your business is engaged in the gold trade, refining, or wholesale jewellery, ensure your RCM procedures, invoices, and declarations are aligned with FTA rules to avoid penalties.

🌐 Visit us: www.sa-auditors.com

📧 Email: info@sa-auditors.com

📱 WhatsApp: +971-XX-XXXXXXX