RCM and Import VAT Adjustments

Introduction

Reverse Charge Mechanism (RCM) and Import VAT are two key concepts that businesses in the UAE must understand to stay VAT-compliant. Many importers, especially those dealing in goods and international services, often find it tricky to account for VAT correctly when imports are involved. Let’s break it down step-by-step.

________________________________________

📌 What is Reverse Charge Mechanism (RCM)?

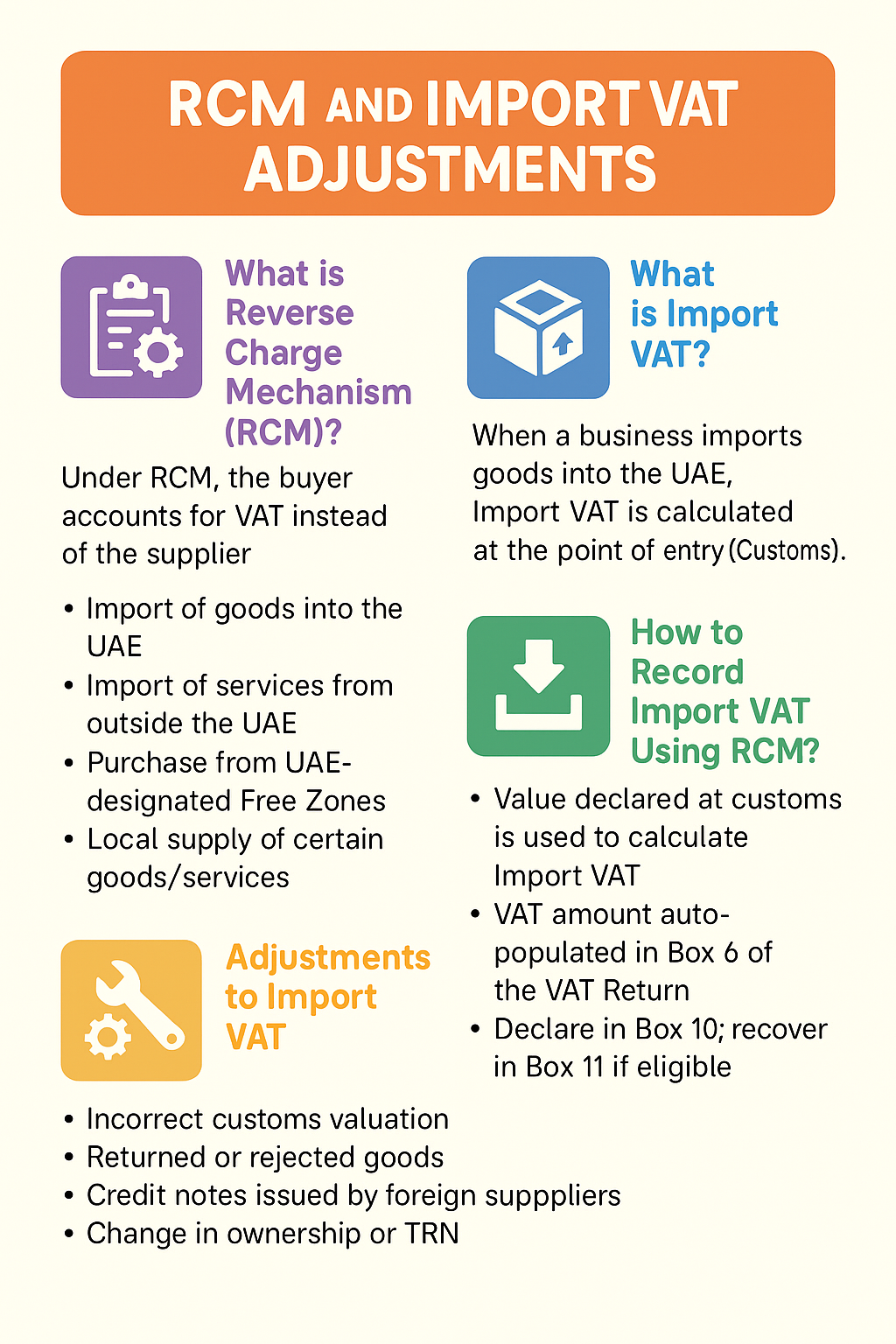

Under the Reverse Charge Mechanism, the buyer (recipient) of goods or services is required to account for VAT, instead of the supplier. This is mainly applicable in cross-border transactions.

✅ When is RCM applicable?

• Import of goods into the UAE.

• Import of services from outside the UAE.

• Purchase from UAE-designated Free Zones.

• Local supply of certain goods/services such as gold, hydrocarbons, or crude oil (in some cases).

________________________________________

🧾 What is Import VAT?

When a business imports goods into the UAE, Import VAT is calculated at the point of entry (Customs). However, if the business has a valid TRN (Tax Registration Number), the VAT is not paid at customs, but rather reported and adjusted in the VAT Return (Form 201) under RCM.

________________________________________

📥 How to Record Import VAT Using RCM?

When goods are imported:

1. The value declared at customs is used to calculate the import VAT (usually CIF value + duties).

2. The VAT amount is auto-populated in Box 6 of the VAT Return.

3. The same amount should be declared in Box 10 (RCM - Output VAT) and, if eligible, recovered in Box 11 (Input VAT).

📊 Example:

• CIF value: AED 100,000

• Import VAT @ 5% = AED 5,000

• Box 6: AED 5,000 (Import VAT auto-filled)

• Box 10: AED 5,000 (RCM Output VAT)

• Box 11: AED 5,000 (Input VAT recoverable)

So the net VAT payable = AED 0, if you’re eligible to fully recover input tax.

________________________________________

🔄 Adjustments to Import VAT

Sometimes, the import VAT amount needs to be adjusted due to:

• Incorrect customs valuation

• Returned or rejected goods

• Credit notes issued by foreign suppliers

• Change in ownership or TRN

🔧 How to Adjust?

• Submit Import VAT Adjustment Requests via the EmaraTax portal.

• Provide supporting documents: commercial invoices, bills of entry, credit notes, etc.

• Adjust in the subsequent VAT return period if approved.

________________________________________

🛑 Common Mistakes to Avoid

❌ Forgetting to include RCM on imported services.

❌ Claiming Input VAT without proper documentation.

❌ Not reconciling customs data with your VAT return.

❌ Not correcting mismatches in Box 6 vs Box 10.

________________________________________

✅ Best Practices for RCM & Import VAT

✔ Always reconcile Customs Import Code data with VAT return figures.

✔ Maintain proper documentation: invoices, customs declarations, import permits.

✔ Automate tracking using your accounting or ERP software.

✔ If unsure, consult a VAT expert to avoid penalties.

________________________________________

🧠 Conclusion

RCM and Import VAT are crucial in cross-border trade compliance. While they may seem complex, a structured approach to recording and adjusting these in your VAT return ensures smooth compliance and avoids penalties. Regular reconciliation and maintaining accurate records are the keys to mastering VAT in the UAE.

🌐 Visit us: www.sa-auditors.com

📧 Email: info@sa-auditors.com

📱 WhatsApp: +971-XX-XXXXXXX