R&D Expenditures and Tax Treatment

Introduction

Research and Development (R&D) plays a critical role in driving innovation, improving business processes, and creating competitive advantages. In recognition of this, jurisdictions around the world, including the UAE, provide specific tax treatments for R&D expenditures to encourage investment in innovation.

Sheikh Anwar Accounting and Auditing LLC explains the tax implications of R&D costs under UAE Corporate Tax Law and how businesses can benefit from proper classification and documentation of such expenditures.

________________________________________

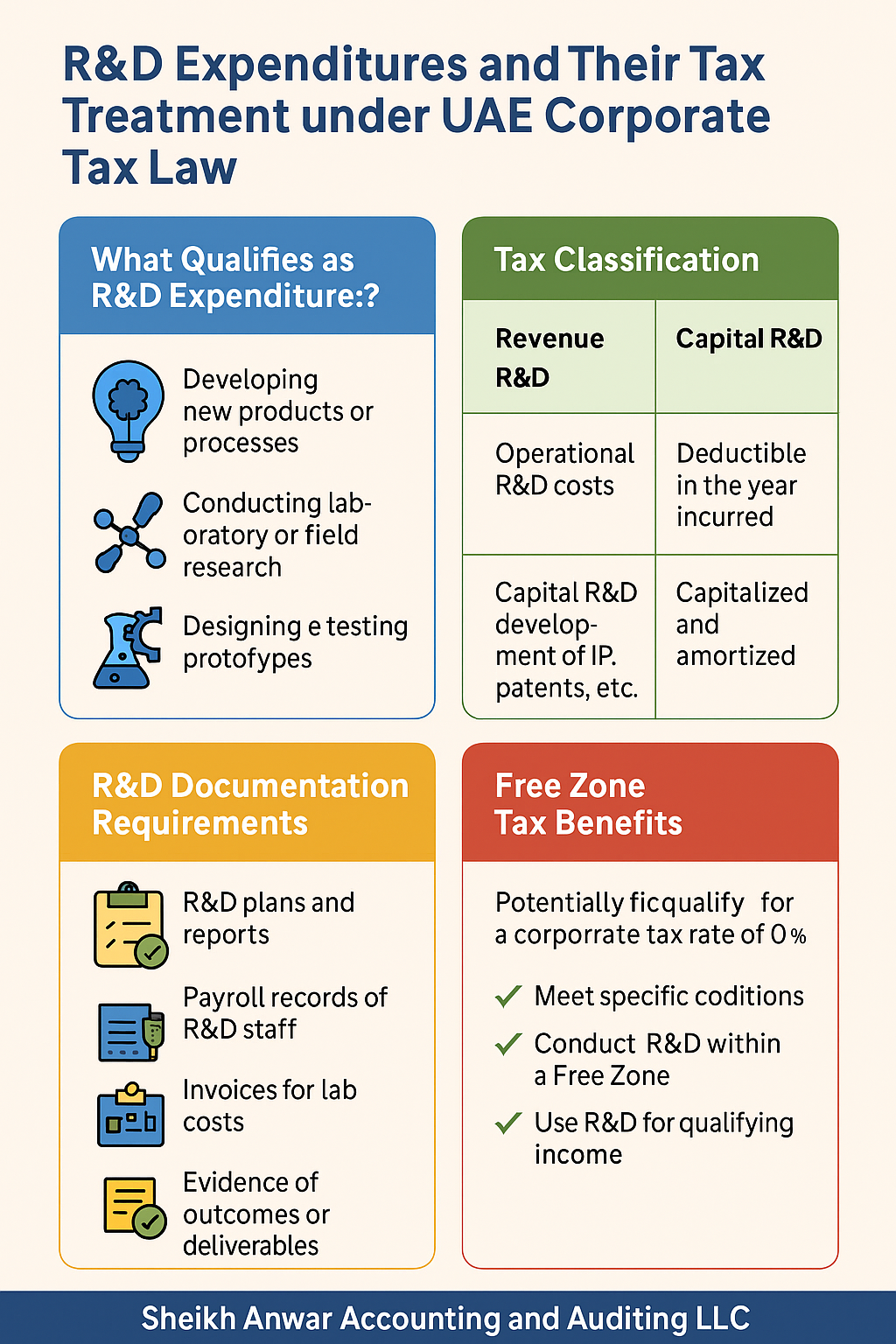

✅ What Qualifies as R&D Expenditure?

R&D expenditures generally refer to the costs incurred in developing new products, services, systems, or processes, or significantly improving existing ones. These activities must involve a level of scientific or technical uncertainty and aim to produce new knowledge or capabilities.

Examples of qualifying R&D activities include:

• Developing new software or apps

• Creating prototypes and conducting lab tests

• Engineering new manufacturing methods

• Conducting market feasibility studies for innovative products

• Experimenting with new technologies

________________________________________

🧾 Tax Classification of R&D Expenditures in the UAE

Under Federal Decree-Law No. 47 of 2022, R&D expenditures are considered deductible expenses provided they are:

1. Wholly and exclusively incurred for business purposes

2. Not capital in nature, unless they relate to qualifying intangible assets

3. Properly documented and supported by evidence of business use

________________________________________

🧮 Capital vs. Revenue Expenditure

In UAE Corporate Tax, it is important to distinguish between:

Type Description Tax Treatment

Revenue R&D Recurring operational R&D costs (e.g., employee wages, testing) Fully deductible in the year incurred

Capital R&D Long-term development of IP, software, or patents Capitalized and depreciated/amortized over time

Sheikh Anwar Accounting and Auditing LLC helps businesses categorize and account for their R&D spend accurately to ensure optimal tax treatment.

________________________________________

📌 Deductibility Conditions for R&D Expenses

To be allowed as a deduction, R&D expenses must:

• Be directly linked to business activities

• Be incurred within the tax period

• Not be listed as a non-deductible expense (e.g., entertainment, personal expenses)

• Be substantiated with contracts, invoices, and R&D project documentation

________________________________________

🧠 Intellectual Property (IP) and R&D

Where R&D leads to the creation of intangible assets like patents or software, the costs may be:

• Capitalized and amortized over the asset’s useful life

• Subject to separate treatment under transfer pricing, if the IP is transferred to related parties

• Eligible for special treatment under Free Zone qualifying income rules, in specific R&D-based business models

At Sheikh Anwar Accounting and Auditing LLC, we evaluate the IP implications of R&D spend and guide clients on amortization, capitalization, and intercompany use.

________________________________________

🧩 Free Zone Companies & R&D

Some Designated Free Zones allow R&D-focused entities to benefit from a 0% corporate tax rate on qualifying income—if they meet conditions related to:

• Substance (employees, assets, activities in the Free Zone)

• Maintenance of adequate R&D functions within the UAE

• Use of IP in generating qualifying income

We support Free Zone clients in assessing whether their R&D activities meet the criteria under Cabinet Decision No. 55 of 2023 and Ministerial Decision No. 139 of 2023.

________________________________________

📂 Documentation Requirements

Maintaining proper documentation is critical for supporting tax deductibility of R&D expenses. Required documents include:

• R&D project plans and technical documentation

• Timesheets and payroll records of R&D personnel

• Vendor invoices and lab/testing bills

• Evidence of project outcomes or deliverables

• Capitalization schedules (if applicable)

As part of our compliance service, Sheikh Anwar Accounting and Auditing LLC helps businesses set up R&D tracking systems to maintain audit-ready documentation.

________________________________________

🔍 Example – R&D Expense Breakdown

ABC Tech Solutions LLC incurs the following in 2024:

Expenditure Amount (AED) Tax Treatment

R&D engineer salaries 250,000 Fully deductible

Cloud computing software for testing 30,000 Deductible operational cost

Patent registration fees 50,000 Capitalized and amortized

Market survey for new product 15,000 Deductible

Team training on R&D tools 10,000 Deductible (subject to limits)

________________________________________

🛡️ Common Mistakes to Avoid

• Treating capital R&D as fully deductible in one year

• Failing to separate business-related R&D from general admin costs

• Missing documentation to support the nature and purpose of R&D

• Ignoring transfer pricing obligations if R&D results are shared across related parties

Our tax consultants at Sheikh Anwar Accounting and Auditing LLC ensure these pitfalls are avoided during corporate tax filings.

________________________________________

✅ Summary

Key Point Details

R&D can be deductible Yes, if incurred wholly for business and properly documented

Capital R&D must be capitalized Yes, and amortized over useful life

R&D can impact Free Zone eligibility Yes, for qualifying income treatment

Documentation is essential To claim deductions and defend against FTA queries

________________________________________

📣 Final Thoughts

R&D is not just an investment in innovation—it's an opportunity to optimize your tax position under UAE Corporate Tax Law. By correctly identifying, categorizing, and documenting R&D costs, businesses can significantly reduce their taxable income and leverage tax incentives, especially in Free Zones.

At Sheikh Anwar Accounting and Auditing LLC, we specialize in R&D tax advisory, IP structuring, and Free Zone compliance. Let our team help you turn innovation into tax savings.

________________________________________

www.sa-auditors.com