Permanent Establishment in Corporate Tax

Introduction

The concept of Permanent Establishment (PE) is a cornerstone of international taxation and plays a vital role in determining when a non-resident entity is liable to pay Corporate Tax in the UAE. Under the UAE Federal Decree-Law No. 47 of 2022, a non-resident person will be subject to Corporate Tax if they have a PE in the UAE.

Here, we explain what a PE is, its types, the criteria that establish one, and the consequences under UAE Corporate Tax Law.

________________________________________

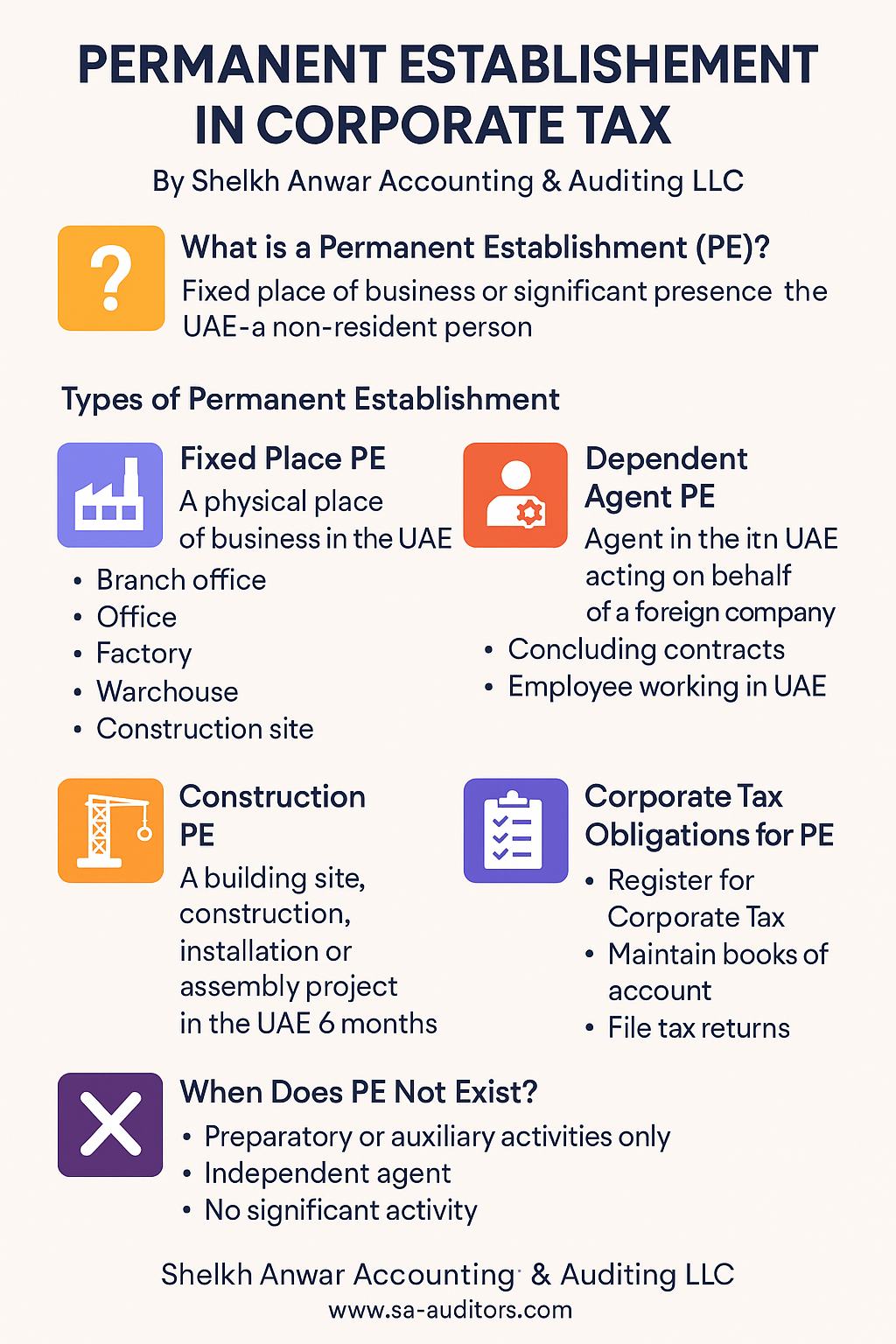

🧾 What Is a Permanent Establishment (PE)?

A Permanent Establishment refers to a fixed place of business or significant presence through which a non-resident person carries out business or commercial activities in the UAE, wholly or partly.

This concept ensures that foreign companies are taxed in the UAE if they maintain sufficient presence or activities within the country, even if they are not incorporated here.

________________________________________

⚖️ Legal Basis in UAE

• Article 14 of UAE Corporate Tax Law (Federal Decree-Law No. 47 of 2022)

• Cabinet Decision No. 56 of 2023 on Nexus and PE

• Aligned with the OECD Model Tax Convention and BEPS Action Plan

________________________________________

🧩 Types of Permanent Establishment

1. Fixed Place PE

A physical place of business in the UAE that is used to carry out the activities of a foreign entity.

Examples:

• Branch office

• Office premises

• Factory

• Warehouse

• Construction site (if exceeds 6 or 12 months as per treaty)

• Workshop or retail outlet

To qualify, the following must apply:

• Fixed location

• Habitual use for business

• Conduct of core business activities

________________________________________

2. Dependent Agent PE

This arises when a person or agent in the UAE acts on behalf of a foreign enterprise and has authority to conclude contracts in the name of the enterprise.

Examples:

• A sales agent consistently negotiating and finalizing deals

• An employee of the foreign company working remotely from UAE

It does not apply to independent agents acting in the ordinary course of business, such as legal or audit firms.

________________________________________

🏗️ Construction PE

A building site, construction, installation, or assembly project in the UAE constitutes a PE if it lasts more than 6 months, unless a relevant tax treaty provides a different threshold.

________________________________________

📍 Nexus in the UAE (For Non-Resident Juridical Persons)

Even without a physical presence, a Nexus may be deemed to exist if the non-resident derives income from real estate or other assets in the UAE. This can result in tax liability under the Corporate Tax Law.

________________________________________

🧠 PE vs. Branch vs. Subsidiary

Feature Permanent Establishment Branch Office Subsidiary Company

Legal registration Not separately registered Registered in UAE Separate UAE legal entity

Tax liability Yes Yes Yes

Control Managed by foreign entity Managed by parent Locally managed

A PE is a functional concept, while a branch or subsidiary is a legal structure.

________________________________________

💼 When Does PE Not Exist?

A foreign company will not be considered to have a PE if:

• The UAE activities are preparatory or auxiliary in nature (e.g., storage, collecting data, market research).

• The UAE person is acting as an independent agent.

• No significant activity or presence exists in the UAE.

However, these exceptions are narrowly interpreted.

________________________________________

📝 Corporate Tax Obligations for PE

If a PE is established, the foreign entity must:

1. Register for Corporate Tax in the UAE

2. Maintain proper books of accounts

3. Prepare financial statements for UAE-source income

4. File annual Corporate Tax returns

5. Pay 9% tax on UAE-source taxable income (after AED 375,000)

________________________________________

⚠️ Risks of Ignoring PE Rules

• Unregistered PE may face:

o Penalties

o Back taxes

o Reputational damage

o Audit investigations

Misclassifying a PE can lead to non-compliance and result in substantial penalties under UAE law.

________________________________________

🌐 Treaty Considerations

The UAE has signed more than 130 Double Tax Treaties (DTTs). These treaties may:

• Provide additional PE thresholds

• Override domestic UAE law in certain cases

• Prevent double taxation on the same income

Tip: Always consider DTT provisions if your business operates in multiple jurisdictions.

________________________________________

🧠 How Sheikh Anwar Accounting & Auditing LLC Can Help

Our tax advisory team provides:

✅ PE risk assessment

✅ Corporate Tax registration for non-residents

✅ Cross-border structuring for tax efficiency

✅ Treaty interpretation and advisory

✅ Ongoing compliance and tax filing for PEs

With deep expertise in international taxation and UAE compliance, we ensure your operations remain lawful and tax-optimized.

________________________________________

📞 Contact Us

Sheikh Anwar Accounting & Auditing LLC

🌐 www.sa-auditors.com

📧 info@sa-auditors.com

📞 +971-XX-XXX-XXXX