Penalties for Transfer Pricing Non-Compliance

Introduction

Transfer Pricing (TP) has become one of the most critical areas of corporate tax compliance across the globe, including in the UAE under the Federal Decree-Law No. 47 of 2022 on Corporate Tax. Multinational groups and even domestic businesses engaged in related-party transactions are required to maintain proper documentation, ensure arm’s length pricing, and file necessary disclosures.

Non-compliance with TP obligations not only attracts financial penalties but can also trigger reputational risks, disputes with tax authorities, and even increased audit scrutiny. Below is a detailed breakdown of the penalties and consequences.

________________________________________

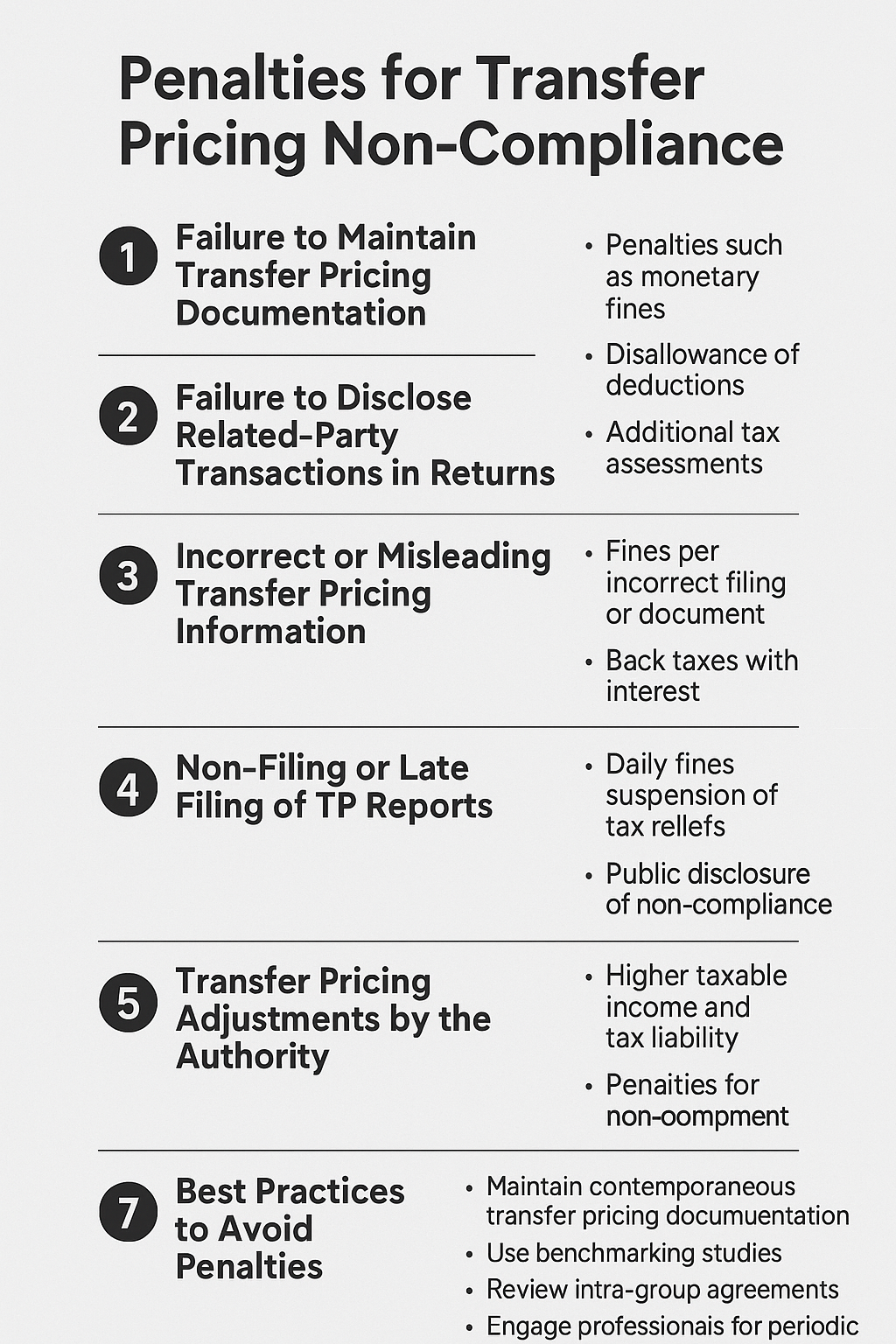

1. Failure to Maintain Transfer Pricing Documentation

Businesses are required to prepare and maintain:

• Master File (group-level overview).

• Local File (entity-specific detailed TP documentation).

• Country-by-Country Report (CbCR) (for large multinational groups, where applicable).

Penalties may include:

• Monetary fines for not maintaining or failing to provide documentation upon request by the tax authority.

• Disallowance of deductions for intra-group payments if arm’s length evidence is absent.

• Additional tax assessments based on adjustments made by the authority.

________________________________________

2. Failure to Disclose Related-Party Transactions in Returns

The UAE requires businesses to submit a Related Party Disclosure Form with their corporate tax return.

Consequences of failure:

• Penalties for incomplete, inaccurate, or false declarations.

• Interest charges on underpaid tax resulting from misreporting.

• Increased risk of audit selection.

________________________________________

3. Incorrect or Misleading Transfer Pricing Information

If a business provides inaccurate or misleading information (deliberately or negligently), the authority may impose strict penalties.

Examples include:

• Inflated expenses on intercompany management fees.

• Understated revenues from related-party sales.

• Manipulation of interest rates on intercompany loans.

Penalties may include:

• Fines per incorrect filing or document.

• Back taxes with interest.

• Additional administrative penalties for misrepresentation.

________________________________________

4. Non-Filing or Late Filing of TP Reports

For CbCR and other mandated filings, non-filing or late submissions can result in heavy administrative penalties.

• Daily fines for delayed submissions (subject to maximum caps).

• Suspension of certain tax reliefs until compliance is achieved.

• Public disclosure of non-compliance in extreme cases.

________________________________________

5. Transfer Pricing Adjustments by the Authority

If the tax authority determines that a company has not applied the Arm’s Length Principle, it has the power to adjust taxable profits.

Implications include:

• Higher taxable income and tax liability.

• Penalties for underpayment of tax (often a percentage of the unpaid amount).

• Possible double taxation if no relief is available in cross-border scenarios.

________________________________________

6. Reputational and Operational Consequences

Beyond monetary penalties, non-compliance can bring:

• Increased scrutiny: More frequent and detailed audits.

• Reputational risk: Negative perception from regulators, investors, and business partners.

• Operational disruption: Time, resources, and costs diverted to handling disputes.

________________________________________

7. Best Practices to Avoid Penalties

• Maintain contemporaneous TP documentation.

• Ensure accurate disclosures in returns.

• Use benchmarking studies to support arm’s length pricing.

• Review intra-group agreements regularly.

• Engage professionals for periodic TP health checks.

________________________________________

✅ Conclusion

Transfer Pricing non-compliance is costly, not only financially but also reputationally. With the UAE Corporate Tax law aligning with OECD guidelines, businesses should adopt a proactive approach: prepare proper documentation, disclose transactions correctly, and follow the arm’s length principle. This will safeguard against penalties and build stronger compliance credibility.

________________________________________

Would you like me to also add the specific UAE Corporate Tax penalty amounts (as per Cabinet Decision No. 75 of 2023 and updates) in a table format, so that your readers get exact figures alongside the explanation?

You said:

also mention compay deetails

ChatGPT said:

Got it ✅. I’ll expand the blog to include your company details so that it doubles as an informative article and a subtle marketing piece for Sheikh Anwar Accounting & Auditing LLC.

Here’s the revised version with company branding included:

________________________________________

Penalties for Transfer Pricing Non-Compliance

Transfer Pricing (TP) has become one of the most critical areas of corporate tax compliance across the globe, including in the UAE under the Federal Decree-Law No. 47 of 2022 on Corporate Tax. Multinational groups and even domestic businesses engaged in related-party transactions are required to maintain proper documentation, ensure arm’s length pricing, and file necessary disclosures.

Non-compliance with TP obligations not only attracts financial penalties but can also trigger reputational risks, disputes with tax authorities, and even increased audit scrutiny. Below is a detailed breakdown of the penalties and consequences.

________________________________________

1. Failure to Maintain Transfer Pricing Documentation

Businesses are required to prepare and maintain:

• Master File (group-level overview).

• Local File (entity-specific detailed TP documentation).

• Country-by-Country Report (CbCR) (for large multinational groups, where applicable).

Penalties may include:

• Monetary fines for not maintaining or failing to provide documentation upon request by the tax authority.

• Disallowance of deductions for intra-group payments if arm’s length evidence is absent.

• Additional tax assessments based on adjustments made by the authority.

________________________________________

2. Failure to Disclose Related-Party Transactions in Returns

The UAE requires businesses to submit a Related Party Disclosure Form with their corporate tax return.

Consequences of failure:

• Penalties for incomplete, inaccurate, or false declarations.

• Interest charges on underpaid tax resulting from misreporting.

• Increased risk of audit selection.

________________________________________

3. Incorrect or Misleading Transfer Pricing Information

If a business provides inaccurate or misleading information (deliberately or negligently), the authority may impose strict penalties.

Examples include:

• Inflated expenses on intercompany management fees.

• Understated revenues from related-party sales.

• Manipulation of interest rates on intercompany loans.

Penalties may include:

• Fines per incorrect filing or document.

• Back taxes with interest.

• Additional administrative penalties for misrepresentation.

________________________________________

4. Non-Filing or Late Filing of TP Reports

For CbCR and other mandated filings, non-filing or late submissions can result in heavy administrative penalties.

• Daily fines for delayed submissions (subject to maximum caps).

• Suspension of certain tax reliefs until compliance is achieved.

• Public disclosure of non-compliance in extreme cases.

________________________________________

5. Transfer Pricing Adjustments by the Authority

If the tax authority determines that a company has not applied the Arm’s Length Principle, it has the power to adjust taxable profits.

Implications include:

• Higher taxable income and tax liability.

• Penalties for underpayment of tax (often a percentage of the unpaid amount).

• Possible double taxation if no relief is available in cross-border scenarios.

________________________________________

6. Reputational and Operational Consequences

Beyond monetary penalties, non-compliance can bring:

• Increased scrutiny: More frequent and detailed audits.

• Reputational risk: Negative perception from regulators, investors, and business partners.

• Operational disruption: Time, resources, and costs diverted to handling disputes.

________________________________________

7. Best Practices to Avoid Penalties

• Maintain contemporaneous TP documentation.

• Ensure accurate disclosures in returns.

• Use benchmarking studies to support arm’s length pricing.

• Review intra-group agreements regularly.

• Engage professionals for periodic TP health checks.

________________________________________

✅ About Us – Sheikh Anwar Accounting & Auditing LLC

At Sheikh Anwar Accounting & Auditing LLC, we specialize in Transfer Pricing, Corporate Tax, VAT, and AML compliance in the UAE. Our expertise in TP documentation (Master File, Local File, and Benchmarking Reports) ensures that businesses stay fully compliant with the Federal Tax Authority’s requirements while minimizing risks of penalties and disputes.

• MOE Registered Auditor – Entry No. 5817

• Company Entry No. LC4695-01

• Offices in Dubai & India

• Sector expertise: Gold, Diamond, Jewellery, Manufacturing, Real Estate, Retail, Free Zone Companies, and Multinational Groups

We help businesses with:

• Preparation of Master File & Local File.

• Benchmarking Studies (AED 5,500 onwards).

• TP Risk Assessment & Health Checks.

• Advisory on Related Party Disclosures.

• End-to-end UAE Corporate Tax Compliance.

📞 Contact Us Today

🌐 www.sa-auditors.com

✉️ info@sa-auditors.com