Overview of UAE Corporate Tax Law

The United Arab Emirates (UAE), known for its business-friendly environment, made a landmark shift by introducing a federal Corporate Tax regime, effective from 1st June 2023, under Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses.

This move aligns the UAE with global standards on tax transparency and the OECD’s Base Erosion and Profit Shifting (BEPS) project. Here, we present a comprehensive overview of the UAE Corporate Tax Law, who it applies to, what it covers, and what businesses must do to stay compliant.

________________________________________

📚 Legal Framework

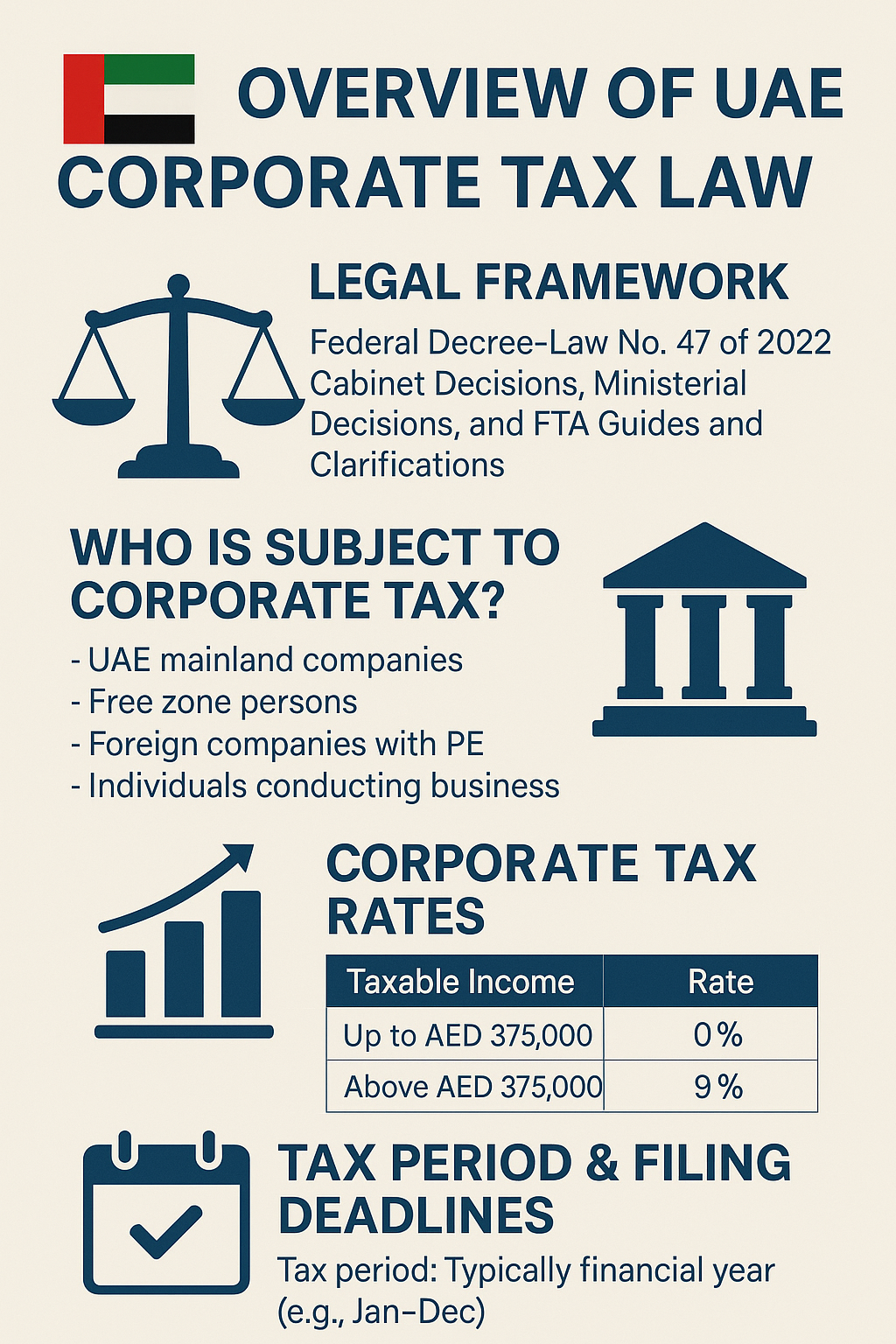

The UAE Corporate Tax regime is governed by:

• Federal Decree-Law No. 47 of 2022

• Cabinet Decisions, Ministerial Decisions, and FTA Guides and Clarifications

• OECD’s BEPS Pillar Two framework for large multinational groups

The Federal Tax Authority (FTA) is responsible for tax administration and compliance enforcement.

________________________________________

💼 Who is Subject to Corporate Tax?

The UAE Corporate Tax applies to:

• UAE mainland companies

• Free zone persons (subject to 0% or 9% based on qualifying conditions)

• Foreign companies with a Permanent Establishment (PE) in the UAE

• Individuals conducting business activities under a license (sole establishments)

• Partnerships, depending on legal structure

❌ Exempt Persons

Some entities are exempt from Corporate Tax, including:

• Government and government-controlled entities

• Public benefit entities

• Qualifying investment funds

• Entities engaged in natural resource extraction (already taxed at the Emirate level)

________________________________________

📈 Corporate Tax Rates

Taxable Income Rate

Up to AED 375,000 0%

Above AED 375,000 9%

Multinationals under Pillar Two (revenue ≥ €750m) 15% (once implemented)

________________________________________

🧮 Calculation of Taxable Income

Taxable income is calculated as:

Net Profit/Loss as per IFRS-compliant financials

➕/➖ Adjustments under the Corporate Tax Law

➖ Exempt income (e.g., qualifying dividends, foreign branch profits)

➖ Deductions (subject to limitations and rules)

💡 Common Adjustments:

• Unrealised gains/losses

• Related party transactions (Arm’s Length Principle)

• Entertainment expense caps (50%)

• Interest deduction caps (30% EBITDA rule)

________________________________________

📆 Tax Period & Filing Deadlines

• Tax period: Typically aligns with the financial year (e.g., Jan–Dec).

• Filing deadline: Within 9 months of the end of the relevant tax period.

• Payment: Also due within the same 9-month window.

• Registration: Mandatory for all taxable and exempt persons (via EmaraTax).

________________________________________

🏢 Free Zone Corporate Tax Regime

Free zone entities can benefit from 0% tax on Qualifying Income, subject to:

• Maintaining adequate economic substance in the UAE

• Preparing audited financial statements

• Not electing to be taxed under the standard regime

• Earning income from qualifying activities (e.g., re-export, warehousing, inter-group services, etc.)

Failure to meet any of these conditions may result in a 9% Corporate Tax being applied to all income.

________________________________________

📜 Transfer Pricing (TP) and Related Party Rules

Transfer Pricing rules apply to transactions with related parties and connected persons. Businesses must:

• Comply with Arm’s Length Principle

• Prepare and maintain Transfer Pricing Documentation, including:

o Master File

o Local File

o TP Disclosure Form (annexed with return)

________________________________________

💳 Administration and Penalties

The Federal Tax Authority (FTA) has wide powers to audit, assess, and enforce the law.

📌 Key Penalties:

• Failure to register: AED 10,000

• Late filing of return: AED 500 per month (capped)

• Failure to maintain records: AED 10,000 to AED 20,000

• Incorrect filings or non-cooperation: Higher administrative and tax penalties

________________________________________

🧾 Recordkeeping Requirements

Businesses must keep proper books of accounts and supporting documents for at least 7 years, including:

• Financial statements

• Transfer pricing files

• Contracts

• Invoices and bank records

• Group structure and ownership information

________________________________________

🧠 How We Can Help at Sheikh Anwar Accounting and Auditing LLC

As a professional auditing and tax consultancy firm in the UAE, we offer:

✅ Corporate Tax registration

✅ CT return preparation and filing

✅ Tax impact assessments

✅ Free zone qualification reviews

✅ Transfer Pricing compliance and documentation

✅ Representation during FTA audits and clarifications

________________________________________

🏁 Conclusion

The introduction of Corporate Tax in the UAE is a major development. While the rates remain competitive, the law introduces complex compliance requirements, especially around financial reporting, free zone eligibility, and related party transactions.

Proper planning and expert advice are critical for ensuring compliance and minimizing tax exposure. Let Sheikh Anwar Accounting and Auditing LLC be your trusted tax advisor.

📞 +971-XXX-XXXX | 🌐 www.sa-auditors.com

✉️ info@sa-auditors.com