Onboarding Clients with AML in Mind

Introduction

Client onboarding is the first line of defense in the fight against money laundering and terrorist financing. A weak onboarding process can expose businesses to financial crime, regulatory penalties, and reputational damage. In the UAE, regulators such as the Ministry of Economy (MOE), Central Bank, DFSA, and FSRA emphasize that Designated Non-Financial Businesses and Professions (DNFBPs) and financial institutions must adopt a risk-based approach when onboarding new clients.

________________________________________

1. The Regulatory Context

UAE AML obligations for client onboarding are rooted in:

• Federal Decree-Law No. 20 of 2018 on AML/CFT.

• Cabinet Decision No. 10 of 2019 (executive regulations).

• Cabinet Decision No. 58 of 2020 (beneficial ownership and UBO registers).

• Sector-specific guidelines issued by regulators.

These require businesses to identify and verify customers, beneficial owners, and risk exposures before establishing a business relationship.

________________________________________

2. The Role of Risk-Based Onboarding

A Risk-Based Approach (RBA) ensures resources are allocated efficiently:

• Low-Risk Clients: Simplified due diligence (e.g., listed companies, regulated financial institutions).

• Medium-Risk Clients: Standard due diligence (full KYC, UBO checks, sanctions screening).

• High-Risk Clients: Enhanced due diligence (PEPs, high-risk jurisdictions, complex structures).

This helps businesses balance compliance, efficiency, and customer experience.

________________________________________

3. Key Steps in AML-Compliant Client Onboarding

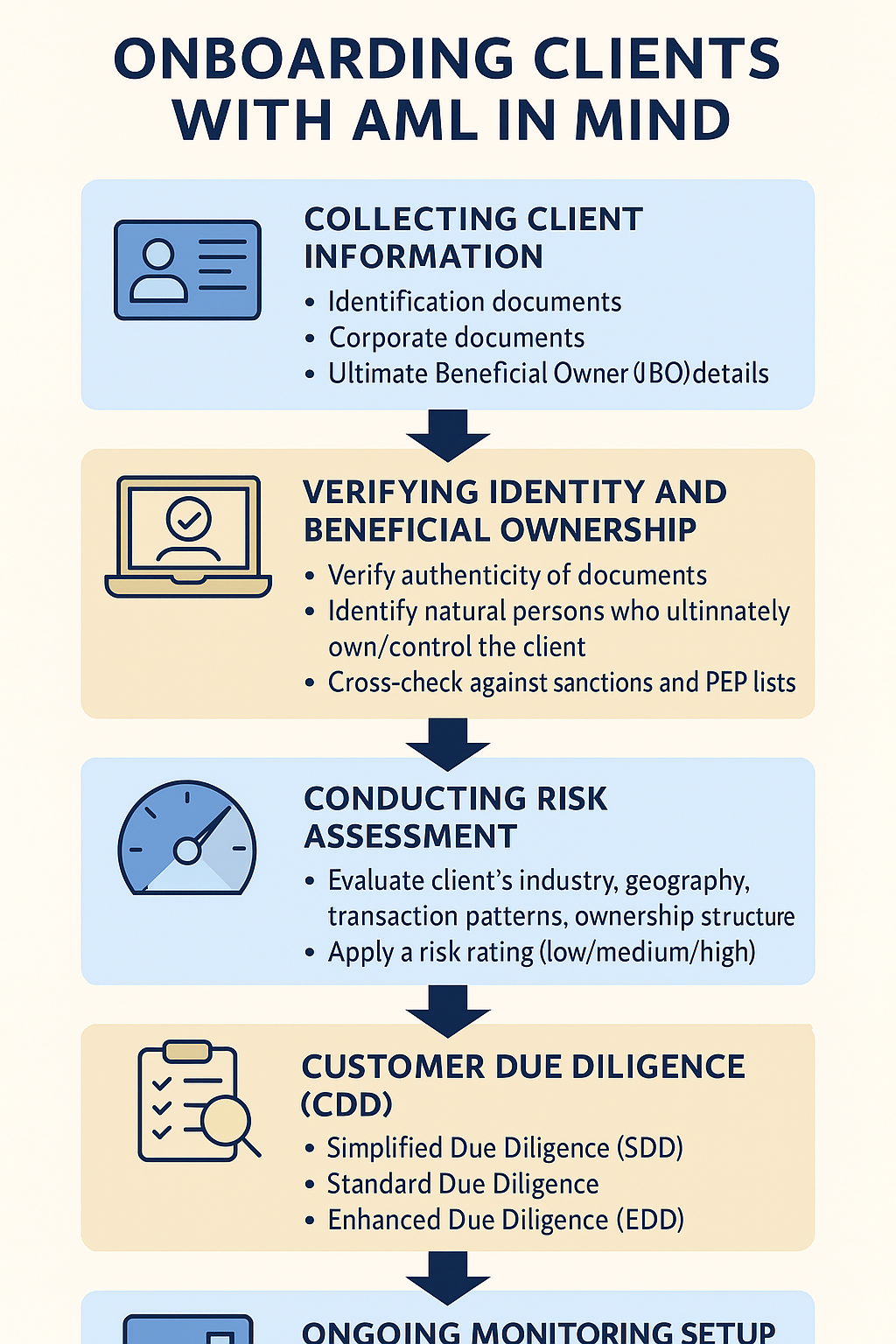

Step 1: Collecting Client Information

• Identification documents (passport, Emirates ID, trade license).

• Corporate documents (articles of association, shareholder registry).

• Ultimate Beneficial Owner (UBO) details.

Step 2: Verifying Identity and Beneficial Ownership

• Verify authenticity of documents.

• Identify natural persons who ultimately own/control the client.

• Cross-check against sanctions and PEP lists.

Step 3: Conducting Risk Assessment

• Evaluate client’s industry, geography, transaction patterns, and ownership structure.

• Apply a risk rating (low/medium/high).

Step 4: Customer Due Diligence (CDD)

• Simplified Due Diligence (SDD): For low-risk clients.

• Standard Due Diligence: For most clients.

• Enhanced Due Diligence (EDD): For PEPs, high-risk jurisdictions, or unusual structures (source of funds/wealth checks).

Step 5: Ongoing Monitoring Setup

• Integrate client into transaction monitoring systems.

• Define frequency of periodic reviews based on risk rating.

• Ensure automatic sanctions/PEP re-screening.

________________________________________

4. Challenges in AML Onboarding

• Complex Ownership Structures: Shell companies and layered ownership require deeper scrutiny.

• Data Accuracy: Incomplete or false documentation increases risks.

• Balancing Compliance and Client Experience: Overly burdensome onboarding can drive away legitimate clients.

________________________________________

5. Best Practices for Effective Onboarding

• Adopt Technology: Use AML/KYC platforms for document verification, sanctions screening, and risk scoring.

• Customize Workflows: Align onboarding procedures with business risk appetite.

• Train Staff: Ensure front-office staff understand AML red flags.

• Keep Records: Maintain onboarding files for at least five years, as required by UAE law.

• Update Regularly: Risk assessments and client profiles must evolve with changing business activity.

________________________________________

6. Benefits of AML-Focused Onboarding

• Regulatory Compliance: Avoid fines and sanctions.

• Fraud Prevention: Filter out bad actors at the entry point.

• Efficiency: Reduce manual errors with risk-based automation.

• Reputation Protection: Build trust with regulators, banks, and stakeholders.

________________________________________

Conclusion

Onboarding clients with AML in mind is more than a regulatory requirement — it is a strategic advantage. By applying a risk-based, technology-driven onboarding process, businesses in the UAE can protect themselves from financial crime while maintaining smooth customer relationships.

When done properly, onboarding not only ensures compliance but also reinforces the credibility and resilience of the organization.

________________________________________

About Sheikh Anwar Accounting & Auditing LLC

At Sheikh Anwar Accounting & Auditing LLC, we specialize in helping businesses implement AML-compliant onboarding frameworks. From customer due diligence and risk assessments to outsourced MLRO services, we provide end-to-end compliance solutions tailored for UAE businesses.

📍 Address: Sheikh Anwar Accounting & Auditing LLC, Office M-35, Dubai Creek Tower, Dubai, UAE

🌐 Website: www.sa-auditors.com

📧 Email: info@sa-auditors.com