Loss Carry Forward Rules

Introduction

One of the most significant features of the UAE Corporate Tax regime, established under Federal Decree-Law No. 47 of 2022, is the ability for businesses to carry forward tax losses and offset them against future taxable income. This provision ensures that businesses, especially those in their startup or investment-heavy phases, are not penalized during periods of initial losses.

Sheikh Anwar Accounting & Auditing LLC provides a comprehensive explanation of the loss carry forward mechanism, its conditions, limitations, and strategic benefits.

________________________________________

📜 Legal Reference

The loss carry forward rules are covered under:

• Article 37 – Utilization of Tax Losses

• Article 38 – Transfer of Tax Losses (if applicable)

• Ministerial Decision No. 114 of 2023 – Additional conditions

________________________________________

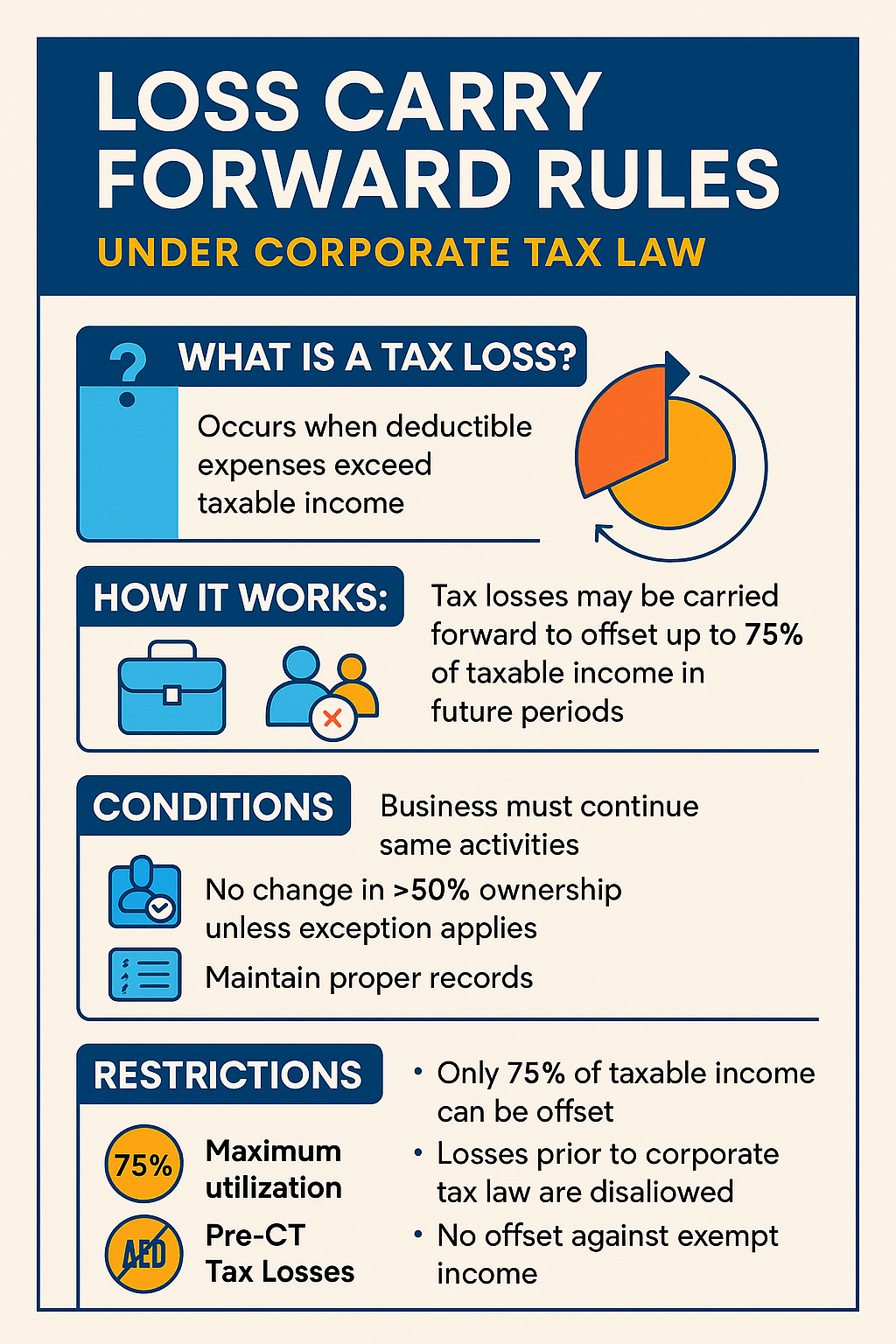

💡 What is a Tax Loss?

A tax loss occurs when a business’s deductible expenses exceed its taxable income in a financial year.

These tax losses cannot be refunded by the FTA but can be:

• Carried forward to reduce taxable income in future years

• Transferred to another group entity under certain conditions (as per Article 38)

________________________________________

🔁 How Loss Carry Forward Works

A business that incurs a loss in one tax year can carry that loss forward and set it off against up to 75% of its future taxable income in subsequent tax periods.

📌 Example:

• Year 1 Tax Loss: AED 1,000,000

• Year 2 Taxable Income: AED 2,000,000

• Max Offset Allowed: 75% of 2,000,000 = AED 1,500,000

• Usable Loss: AED 1,000,000 (fully utilized)

✅ Taxable income in Year 2 = AED 2,000,000 – AED 1,000,000 = AED 1,000,000

________________________________________

⏳ How Long Can Tax Losses Be Carried Forward?

Tax losses can be carried forward indefinitely, provided:

• The same legal entity continues the business

• There is no change in 50% or more of the ownership, unless continuity of business is proven

________________________________________

🔐 Ownership Change Rule

If more than 50% of ownership or voting rights changes:

• The company may lose the ability to carry forward past losses

• Exception: If the business continues the same or similar activities, the losses may still be allowed, subject to FTA approval

________________________________________

✅ Conditions to Use Carried Forward Losses

Condition Description

Business Continuity Entity must continue same or similar activities

Ownership Control No major change (>50%) in ownership unless exception applies

Proper Records Must maintain audited financials and loss calculations

Tax Compliance Returns must be submitted and maintained timely

________________________________________

🚫 Restrictions

Item Restriction

Maximum Utilization Only 75% of taxable income can be offset in any tax year

Losses Before CT Law Losses before June 1, 2023 are not allowed to be carried forward

No Offset Against Exempt Income Carried losses cannot reduce exempt or 0% income

Free Zone Entities Must segregate qualifying and non-qualifying income for proper usage

________________________________________

🧾 Example – Carry Forward Across Multiple Years

Year Taxable Income Carried Loss Loss Used Taxable After Offset

2024 (AED 600,000) AED 600,000 - -

2025 AED 800,000 AED 600,000 AED 600,000 AED 200,000

2026 AED 1,000,000 - - AED 1,000,000

________________________________________

👥 Special Cases – Tax Groups

If the entity is part of a Tax Group:

• The losses carried forward prior to forming the group stay with the respective entity

• Losses can only be used to offset the entity’s income within the group

• The 75% cap still applies at the consolidated level

________________________________________

🧠 Expert Insight by Sheikh Anwar Accounting & Auditing LLC

Our corporate tax professionals help you:

✅ Track losses accurately in your accounting system

✅ Preserve eligibility even through restructuring

✅ File tax returns reflecting proper utilization

✅ Handle FTA inquiries and documentation

✅ Evaluate transfer vs. carry forward options

________________________________________

📞 Contact Us to Manage Your Tax Losses Strategically

Optimize your tax position by correctly applying loss carry forward rules.

📍 Sheikh Anwar Accounting & Auditing LLC

🌐 www.sa-auditors.com

📧 info@sa-auditors.com

📞 +971-XX-XXX-XXXX