Lease Payments and Deductibility

Introduction

Many businesses in the UAE lease assets such as offices, warehouses, equipment, or vehicles to operate efficiently without committing to large capital expenditures. But are lease payments deductible for corporate tax purposes?

Under the UAE Corporate Tax Law, lease payments are generally deductible—subject to certain conditions and distinctions between finance leases and operating leases.

Sheikh Anwar Accounting and Auditing LLC outlines the deductibility of lease payments, documentation requirements, and potential restrictions businesses should be aware of.

________________________________________

📜 Legal Basis

The treatment of lease expenses is governed by:

• Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses

• Ministerial Decision No. 114 of 2023 on deductible and non-deductible expenses

• IFRS 16 – Leases (for accounting treatment and classification guidance)

________________________________________

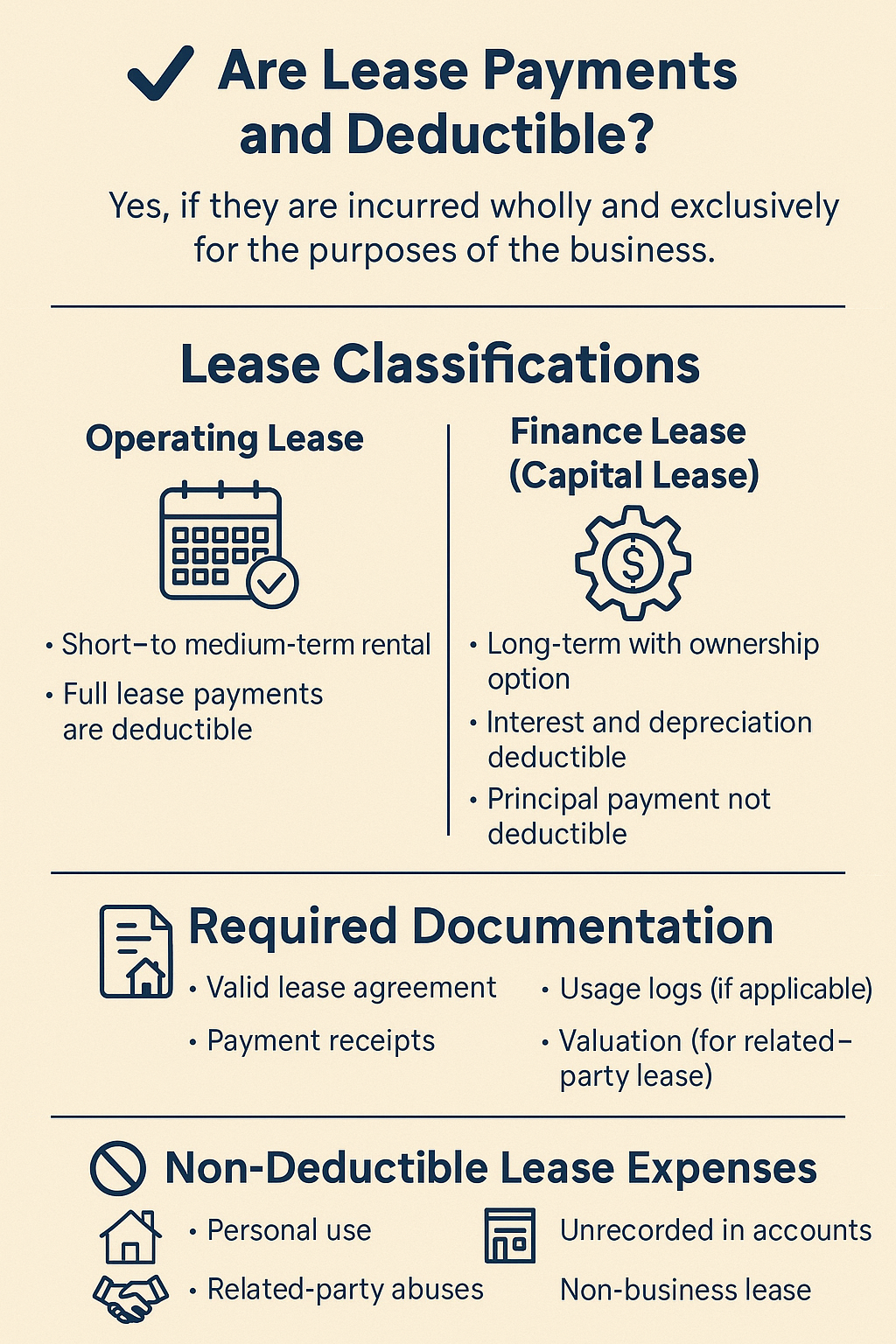

✅ Are Lease Payments Tax Deductible?

Yes, lease payments are generally deductible under UAE Corporate Tax Law if they are incurred wholly and exclusively for business purposes and meet the necessary documentation and classification criteria.

However, how the lease is structured—as an operating lease or a finance lease—will determine how the deduction is calculated and presented.

________________________________________

🔍 Understanding Lease Classifications

1. Operating Lease

• Definition: Short- to medium-term leases where the lessee does not assume ownership risks.

• Examples: Rental of office space, vehicle leases, warehouse rentals.

• Tax Treatment: Entire lease rental payments are deductible in the period they are incurred.

2. Finance Lease (Capital Lease)

• Definition: Long-term lease where the lessee assumes most of the risks and rewards of ownership (e.g., purchase option at end).

• Examples: Leasing machinery with intent to buy.

• Tax Treatment:

o Depreciation of the leased asset is deductible

o Finance cost (interest portion) is also deductible

o The principal repayment is not deductible

💡 Under IFRS 16, many leases previously treated as operating leases may now be classified as finance leases, so correct classification is critical.

________________________________________

🧾 Conditions for Deductibility

To claim lease payments as a deductible expense, businesses must ensure:

1. ✅ The lease is incurred for business use

2. ✅ A valid lease agreement exists

3. ✅ The lease expense is recognized in the accounting records

4. ✅ Payments are not excessive or related-party abusive (subject to arm's length rules)

5. ✅ If the lease is a finance lease, only interest and depreciation are claimed

________________________________________

📂 Required Documentation

To defend your deduction in case of FTA audit, the following records must be maintained:

• Lease agreement (tenancy contract or rental contract)

• Payment receipts or bank statements

• Asset usage logs (if applicable)

• Invoices or debit notes

• Accounting entries in the financial records

• Valuation or benchmarking (for related-party leases)

Sheikh Anwar Accounting and Auditing LLC helps businesses review lease contracts to classify leases accurately and ensure proper documentation.

________________________________________

🚫 Non-Deductible Lease Expenses

While most lease expenses are deductible, some situations can lead to disallowance:

Situation Deductible?

Lease for personal use (e.g., director’s villa) ❌ No

Related-party lease without market terms ❌ May be denied

Lease not recorded in accounting books ❌ No

Lease for tax-exempt or unrelated business ❌ No

________________________________________

💼 Real-Life Example

ABC Interiors LLC leases machinery worth AED 500,000 for 5 years with a buyout option. It is classified as a finance lease.

Expense Type Amount (AED) Tax Treatment

Interest expense 25,000/year ✅ Deductible

Depreciation (10 yrs) 50,000/year ✅ Deductible

Principal payment 100,000/year ❌ Not deductible

Total deductible amount per year = AED 75,000

________________________________________

🧮 Lease vs. Buy – Tax Implications

Option Tax Impact

Lease Lease payments (operating lease) or depreciation + interest (finance lease) are deductible

Buy Capital asset; depreciation deductible over useful life; interest deductible if financed

We assist clients with lease vs. buy analysis to determine the most tax-efficient financing strategy.

________________________________________

🏢 Free Zone Companies and Lease Payments

Free Zone Persons that are subject to 0% tax on Qualifying Income may still claim lease deductions on non-qualifying income.

Proper segregation of qualifying and non-qualifying income and expenses is necessary to avoid misstatements.

________________________________________

📣 Final Thoughts

Lease payments, whether for office rent or equipment, are an integral part of business operations. UAE Corporate Tax Law recognizes this and allows such expenses as deductible—but only when structured and documented properly.

Whether your business leases premises, machinery, or vehicles, Sheikh Anwar Accounting and Auditing LLC ensures that:

• Lease classifications are compliant with IFRS and tax law

• Deductible components are accurately captured

• Related-party leases meet Transfer Pricing standards

• Tax savings are maximized while staying fully compliant

________________________________________

📩 Need help reviewing your lease contracts for tax deductibility?

🌐 Visit: www.sa-auditors.com

📧 Email: info@sa-auditors.com