Key Definitions in Corporate Tax

Introduction

With the introduction of Corporate Tax in the UAE effective from 1st June 2023, it’s essential for businesses and professionals to understand the key terminology used in the Corporate Tax Law. Whether you're a startup, a free zone entity, or a multinational, understanding these definitions is critical for compliance and tax planning.

Here, we simplify the most important definitions from the UAE Corporate Tax framework under Federal Decree-Law No. 47 of 2022.

________________________________________

🧾 Key Definitions Under UAE Corporate Tax Law

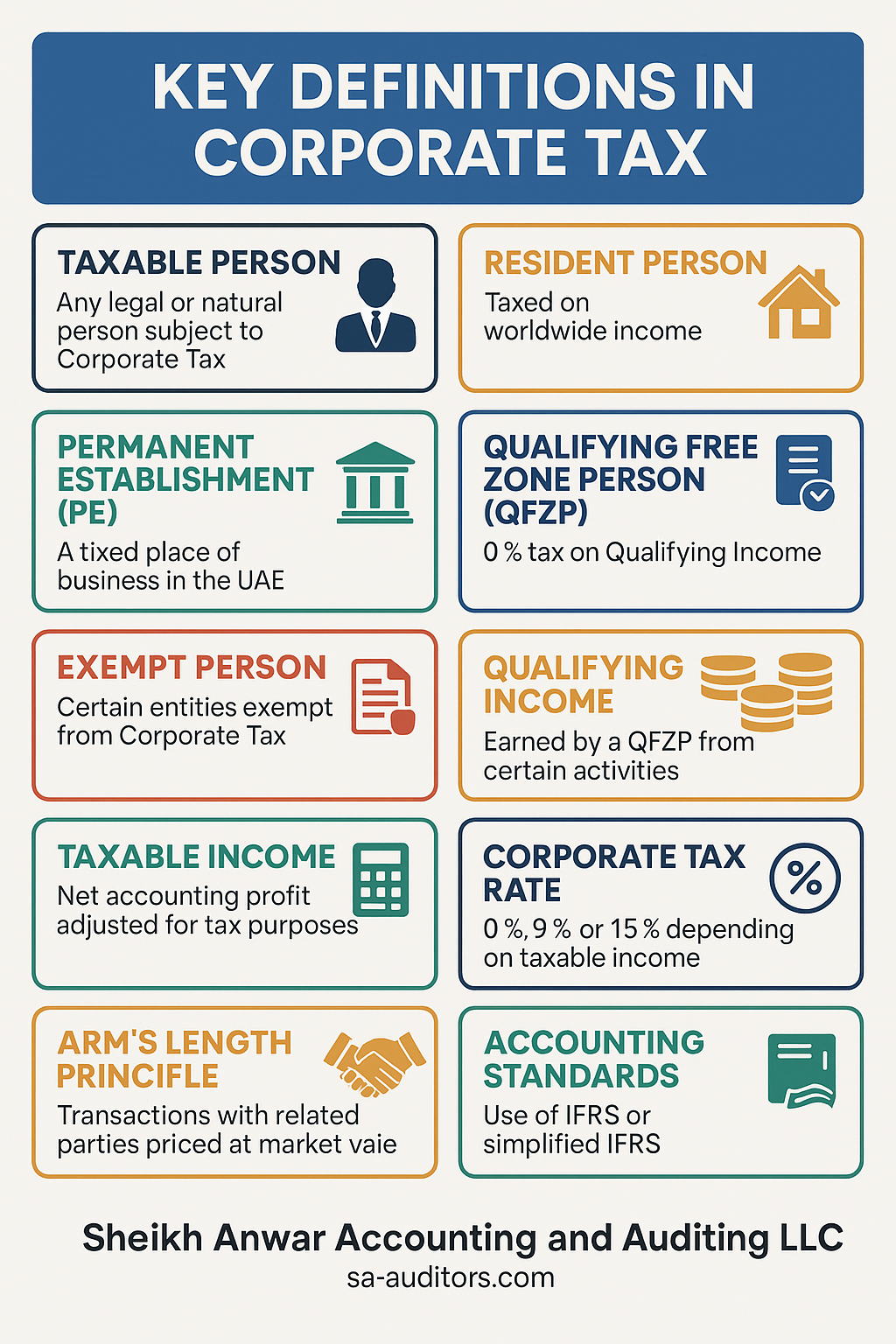

1. Taxable Person

A Taxable Person is any legal or natural person subject to Corporate Tax. This includes:

• UAE-incorporated companies

• Foreign companies with UAE-sourced income or a permanent establishment

• Individuals conducting business in the UAE

• Certain partnerships (depending on structure)

________________________________________

2. Resident Person

A Resident Person is:

• A juridical person incorporated in the UAE

• A foreign company effectively managed and controlled from the UAE

• A natural person conducting business in the UAE

Resident persons are taxed on worldwide income, unless exempted.

________________________________________

3. Non-Resident Person

A Non-Resident Person is any entity that:

• Has no incorporation or effective management in the UAE, and

• Derives income from the UAE, or

• Has a Permanent Establishment (PE) in the UAE

They are taxed only on UAE-sourced income or income attributable to the PE.

________________________________________

4. Permanent Establishment (PE)

This refers to a fixed place of business or dependent agent through which a foreign business partly or wholly carries on its business in the UAE.

Examples include:

• A branch, office, or warehouse

• A construction site (if it meets time thresholds)

• An agent who habitually concludes contracts on behalf of the foreign company

________________________________________

5. Qualifying Free Zone Person (QFZP)

A QFZP is a Free Zone entity that:

• Maintains adequate substance in the UAE

• Derives Qualifying Income

• Prepares audited financial statements

• Complies with transfer pricing rules

QFZPs can benefit from 0% Corporate Tax on qualifying income, but are subject to 9% on non-qualifying income.

________________________________________

6. Qualifying Income

This is income earned by a QFZP from:

• Transactions with other Free Zone Persons

• Certain income from mainland UAE or foreign parties (like re-exports, warehousing, inter-group services, and qualifying trading)

Non-qualifying income will be taxed at 9%.

________________________________________

7. Exempt Person

Entities that are exempt from Corporate Tax, such as:

• Government entities

• Qualifying public benefit entities

• Qualifying investment funds

• Natural resource businesses (taxed locally)

However, registration with the FTA may still be required.

________________________________________

8. Taxable Income

This refers to the net accounting profit (from IFRS-compliant financials), adjusted for:

• Exempt income

• Non-deductible expenses

• Reliefs and losses carried forward

This figure determines your actual tax liability.

________________________________________

9. Corporate Tax Rate

UAE Corporate Tax rates are:

• 0%: For taxable income up to AED 375,000

• 9%: For taxable income exceeding AED 375,000

• 15%: For multinational groups under OECD Pillar Two

________________________________________

10. Arm’s Length Principle

This principle ensures that transactions with related parties are priced as if between unrelated parties in an open market. It prevents profit shifting and ensures fair taxation.

________________________________________

11. Transfer Pricing

These are rules that apply to related party transactions, requiring:

• Documentation (Master File and Local File)

• Disclosure in tax returns

• Justification of pricing using international methods

________________________________________

12. Business

“Business” includes any activity conducted regularly, such as:

• Commercial, industrial, professional, or vocational activities

• Earning income from the use of property or services

If conducted with a valid license, the income may be subject to tax.

________________________________________

13. Accounting Standards

Businesses are required to use International Financial Reporting Standards (IFRS) or simplified IFRS (for small businesses) to compute profits and taxable income.

________________________________________

14. Small Business Relief

Businesses with revenue less than AED 3 million in a tax period may qualify for Small Business Relief and be treated as if they have no taxable income (until 2026).

________________________________________

💼 Why These Definitions Matter

Understanding these definitions helps businesses:

✅ Determine their tax residency and obligations

✅ Accurately calculate and report taxable income

✅ Make strategic decisions (e.g., Free Zone structures)

✅ Avoid penalties due to misclassification or non-compliance

________________________________________

📌 Let Us Help You Stay Compliant

At Sheikh Anwar Accounting and Auditing LLC, we provide:

• Tax health checks and reviews

• Assistance with FTA Corporate Tax registration

• Advice on Free Zone eligibility

• Transfer Pricing compliance documentation

• Corporate Tax filing and representation

________________________________________

📞 Contact Us Today!

📍 Dubai | 🌐 www.sa-auditors.com

📩 info@sa-auditors.com | 📱 +971-XXX-XXXX