Key Components of an AML Policy in UAE

Introduction

An effective Anti-Money Laundering (AML) compliance framework is essential for organizations in the UAE, particularly financial institutions and Designated Non-Financial Businesses and Professions (DNFBPs) such as jewellers, real estate brokers, accountants, and law firms.

With increasing regulatory scrutiny from the Ministry of Economy, Central Bank of the UAE, and free zone regulators (DFSA in DIFC, FSRA in ADGM), businesses must demonstrate robust AML frameworks that align with Federal Decree-Law No. 20 of 2018, Cabinet Decision No. 10 of 2019, and FATF recommendations.

A well-designed AML compliance framework not only ensures legal compliance but also protects reputation, builds client trust, and safeguards against financial crime risks.

________________________________________

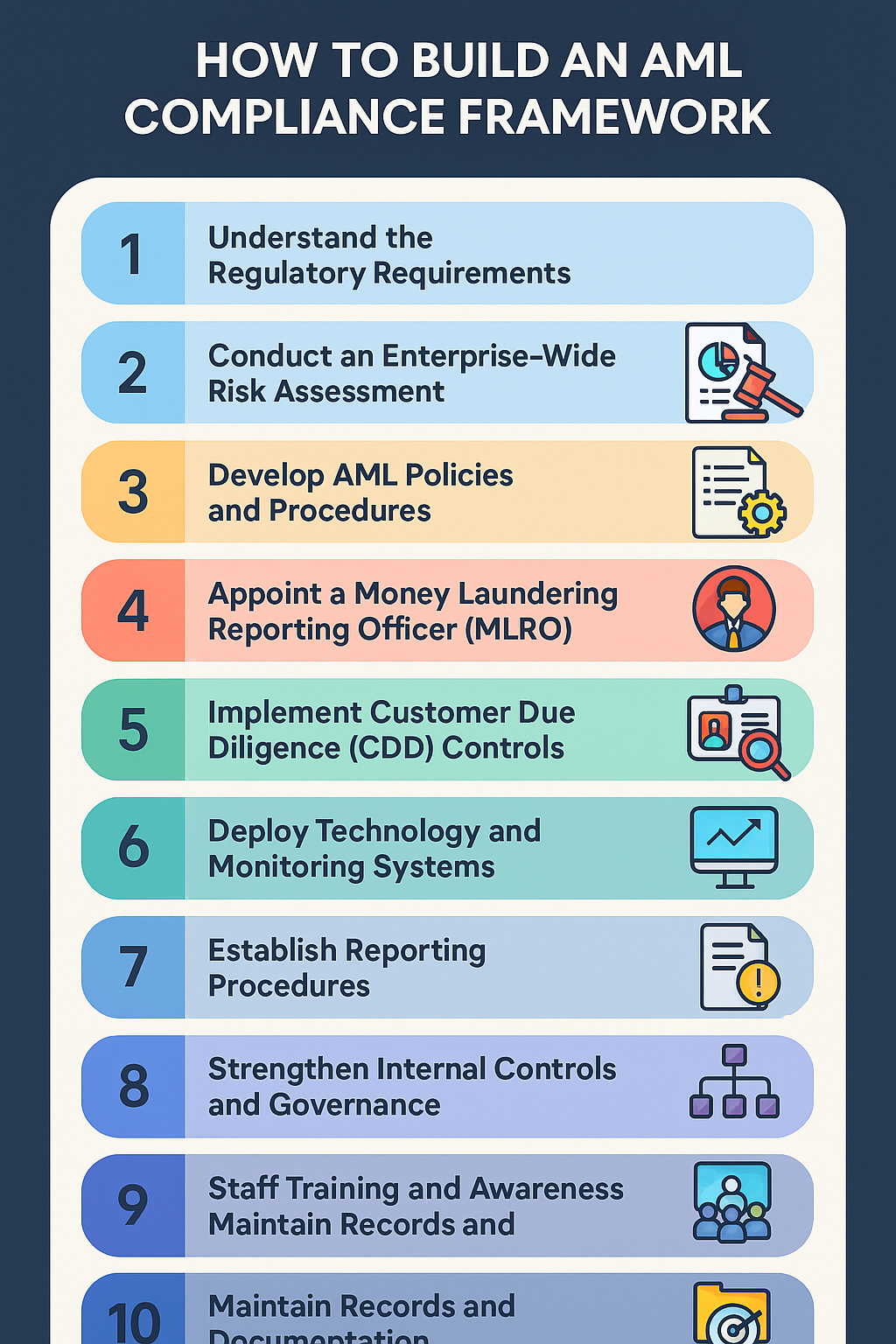

1. Understand the Regulatory Requirements

The first step is to identify the applicable regulations for your business:

• Federal AML/CFT Law (Decree-Law No. 20 of 2018).

• Implementing Regulations under Cabinet Decision No. 10 of 2019.

• Targeted Financial Sanctions obligations (Cabinet Resolution No. 74 of 2020).

• Free zone-specific rules (e.g., DIFC DFSA Rulebook, ADGM FSRA Guidance).

Compliance starts with a clear understanding of which obligations apply to your sector.

________________________________________

2. Conduct an Enterprise-Wide Risk Assessment

• Assess risks based on customers, geography, products, and delivery channels.

• Categorize clients into low, medium, and high-risk segments.

• Use results to shape due diligence, monitoring, and reporting processes.

A risk-based approach (RBA) is central to any AML framework.

________________________________________

3. Develop AML Policies and Procedures

Create written AML policies and procedures that clearly define:

• Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD).

• Sanctions and PEP screening.

• Monitoring and reporting obligations (STRs, LCTRs, DPMSRs).

• Escalation protocols for red flags.

Policies must be reviewed regularly to stay aligned with evolving UAE regulations.

________________________________________

4. Appoint a Money Laundering Reporting Officer (MLRO)

• Designate an MLRO or Compliance Officer responsible for implementing and monitoring the AML framework.

• Ensure the MLRO has direct access to management and regulators.

• Define clear reporting lines and responsibilities.

________________________________________

5. Implement Customer Due Diligence (CDD) Controls

• Verify customer identity using reliable documents.

• Identify Ultimate Beneficial Owners (UBOs) in corporate structures.

• Apply EDD for PEPs or high-risk jurisdictions.

• Retain copies of identification documents for at least five years.

________________________________________

6. Deploy Technology and Monitoring Systems

• Use e-KYC and digital onboarding tools to speed up verification.

• Implement AI-driven transaction monitoring for unusual patterns.

• Integrate systems with the goAML portal for automated reporting.

• Ensure sanctions and PEP screening tools are updated in real time.

________________________________________

7. Establish Reporting Procedures

• File Suspicious Transaction Reports (STRs) to the FIU via goAML.

• Report Large Cash Transactions (LCTRs) exceeding AED 55,000.

• For DPMS, submit DPMS Reports when thresholds are triggered.

• Keep evidence of all reports and communications with regulators.

________________________________________

8. Strengthen Internal Controls and Governance

• Segregate duties to avoid conflicts of interest.

• Perform regular internal audits of AML processes.

• Test the effectiveness of controls through independent reviews.

________________________________________

9. Staff Training and Awareness

• Conduct mandatory AML training for all employees.

• Educate staff on identifying red flags (e.g., structuring, unusual behavior, offshore transfers).

• Keep training logs to demonstrate compliance during inspections.

________________________________________

10. Maintain Records and Documentation

• Retain customer records, CDD files, and transaction history for at least five years.

• Ensure records are easily retrievable for regulatory audits.

________________________________________

11. Continuous Improvement and Regulatory Engagement

• Regularly update the AML framework to reflect new FATF recommendations and UAE regulations.

• Engage proactively with regulators during inspections.

• Benchmark against international best practices to ensure resilience.

________________________________________

Conclusion

Building an AML compliance framework requires a balance of regulatory knowledge, risk-based controls, governance, and technology. For businesses in the UAE—especially DNFBPs—compliance is not just about avoiding penalties but about protecting business integrity and contributing to the UAE’s global reputation for financial transparency.

A well-structured framework is not a one-time effort; it evolves with regulations, technology, and risk trends. Organizations that invest in strong AML foundations today will be better positioned for sustainable growth tomorrow.

________________________________________

About Us

Sheikh Anwar Accounting and Auditing LLC is a trusted auditing and compliance firm in Dubai, specializing in AML advisory, corporate tax, VAT, and transfer pricing. We help DNFBPs and financial institutions design, implement, and test AML compliance frameworks that meet both UAE regulations and FATF standards.

📍 Address: Dubai Creek Tower, M 35, Dubai, UAE

📞 Contact: info@sa-auditors.com | +971-XXX-XXXX

🌐 Website: www.sa-auditors.com