Is RCM Applicable to Intercompany Transactions?

Introduction

As multinational groups (MNEs) expand operations across borders, intercompany transactions are becoming increasingly common—especially between parent entities, subsidiaries, and branches. In this context, one of the most frequently asked VAT questions in the UAE is:

“Does the Reverse Charge Mechanism (RCM) apply to intercompany transactions?”

The answer is yes—but not always. This article explains in detail when and how RCM applies to related-party transactions, supported by examples and official references from the UAE VAT Law and Federal Tax Authority (FTA).

________________________________________

🔄 What is the Reverse Charge Mechanism?

Under Article 48 of UAE VAT Law (Federal Decree-Law No. 8 of 2017), the Reverse Charge Mechanism (RCM) is a provision where the recipient of a supply becomes liable to account for output VAT instead of the supplier.

This applies when:

• The supplier is not VAT-registered in the UAE,

• The recipient is VAT-registered in the UAE,

• The supply is taxable in the UAE (e.g. imported services or goods).

________________________________________

🔍 What is an Intercompany Transaction?

An intercompany transaction refers to a supply of goods or services between related parties, such as:

• Parent companies and subsidiaries

• Branches and head offices

• Group companies under common control

These transactions are not exempt from VAT by default. Like any transaction, they must be analyzed to determine:

• Whether a supply has occurred

• Whether it is taxable, zero-rated, or outside the scope

________________________________________

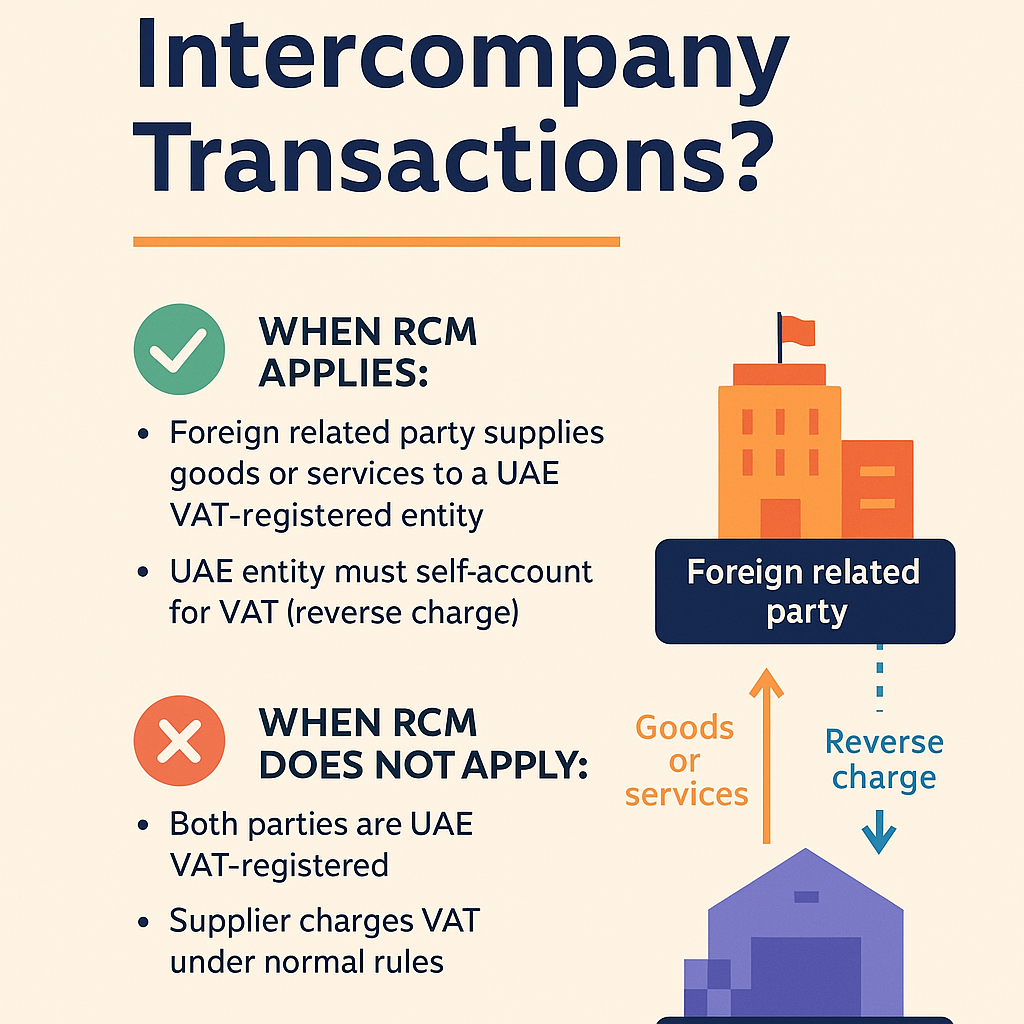

✅ When Does RCM Apply to Intercompany Transactions?

RCM does apply to intercompany transactions, but only under certain conditions:

1. Cross-border service supply from a foreign related party

If a foreign parent company, branch, or group entity provides services to a VAT-registered UAE entity, and the foreign supplier is not registered for VAT in the UAE, the recipient must self-account for VAT under RCM.

2. Imported services or intangible supplies

RCM is automatically triggered when:

• The supplier is outside the UAE

• The UAE recipient uses the service for business purposes

• The UAE recipient is VAT-registered

Common examples:

• Management services from a foreign head office

• Software licenses or cloud services

• Royalty or trademark fees from a foreign parent company

• Back-office or IT support

📜 Legal Reference:

Article 48(1) of UAE VAT Law:

If the supplier is not a taxable person and the recipient is, the recipient shall be treated as making the supply to itself and must account for VAT accordingly.

________________________________________

❌ When Does RCM Not Apply?

1. Domestic Intercompany Transactions (UAE to UAE)

If both companies:

• Are established in the UAE

• Are VAT-registered, and

• Engage in taxable supplies

➡️ Then normal VAT invoicing applies. The supplier charges 5% VAT on their invoice—RCM is not used.

________________________________________

2. Same Legal Entity (Head Office–Branch Transfers)

Transactions between branches and head offices are generally considered outside the scope of VAT if they are not separate legal persons.

However, if:

• The branch and head office operate independently

• The branch has a separate VAT registration

• There’s a supply of goods or services

➡️ Then RCM may apply, subject to FTA interpretation.

________________________________________

🧠 Examples of Intercompany Transactions under RCM

📌 Example 1: Foreign Parent to UAE Subsidiary

A parent company in Germany provides legal and compliance services to its UAE subsidiary. The parent is not VAT-registered in the UAE.

✅ RCM applies.

The UAE subsidiary must:

• Account for output VAT at 5% on the imported service

• Report it under Box 3 in the VAT return

• Claim input VAT in Box 10, if eligible

________________________________________

📌 Example 2: UAE Parent to UAE Subsidiary

Both companies are:

• Incorporated in the UAE

• VAT-registered

The parent provides management consultancy and invoices the subsidiary.

❌ RCM does NOT apply

The parent issues a normal tax invoice with 5% VAT.

________________________________________

📌 Example 3: Foreign Branch to UAE Head Office (Same Legal Entity)

A UAE head office receives internal reports and software support from its branch in India. There is no formal invoice, and both are part of the same legal entity.

⚠️ This is generally outside the scope of VAT, unless:

• The UAE entity is treated as independent for VAT

• Separate VAT registration applies

________________________________________

📚 Guidance from UAE Authorities

FTA VATP019 Public Clarification:

Transactions between related parties must be analyzed based on their substance, not just legal form. RCM can apply even if the entities are related, provided the supplier is not UAE VAT-registered.

________________________________________

📊 Summary Table: When is RCM Applicable?

Scenario RCM Applicable?

Foreign related party provides services to UAE ✅ Yes

UAE group company provides services to UAE entity ❌ No

Foreign branch provides service to UAE HQ ⚠️ Depends on setup

UAE entity imports software/license from group ✅ Yes

________________________________________

💼 Best Practices for Intercompany RCM Compliance

• ✅ Document all intercompany agreements

• ✅ Maintain evidence of supply, such as contracts and service reports

• ✅ Ensure accurate VAT return filings (Box 3 for output VAT, Box 10 for input VAT)

• ✅ Evaluate Transfer Pricing implications (consistent with OECD guidelines)

________________________________________

📩 Need Help with Intercompany VAT or RCM?

Navigating intercompany transactions in the UAE requires expertise in both VAT law and transfer pricing. At Sheikh Anwar Accounting & Auditing LLC, we help businesses:

• Assess RCM applicability

• Prepare compliant documentation

• Coordinate VAT and TP positions

📧 Contact us at info@sa-auditors.com or

🌐 Visit www.sa-auditors.com to schedule a consultation.