Intragroup Services and TP Adjustments

Introduction

As multinational groups expand, the use of intragroup services—such as management support, IT, HR, finance, and marketing—has become increasingly common. However, these services are one of the most scrutinised areas under Transfer Pricing (TP) regulations worldwide, including under the UAE Corporate Tax Law (Federal Decree-Law No. 47 of 2022).

Tax authorities, including the Federal Tax Authority (FTA), expect businesses to prove that intragroup services are:

1. Actually rendered,

2. Provide economic or commercial value, and

3. Charged at arm’s length prices.

If not properly documented, intragroup service charges may be disallowed, leading to TP adjustments, penalties, and potential double taxation.

________________________________________

1. What are Intragroup Services?

Intragroup services refer to activities provided by one group entity to another, for which an arm’s length remuneration should be charged. Common examples include:

• Management Services – strategic planning, corporate governance.

• Administrative Support – HR, legal, accounting, payroll.

• IT Services – software, systems support, data hosting.

• Financial Services – treasury, cash pooling, guarantees.

• Marketing and Sales Support – branding, advertising campaigns.

👉 The key question is whether an independent company would be willing to pay for the same service under comparable circumstances.

________________________________________

2. Arm’s Length Principle in Intragroup Services

To comply with TP rules, intragroup service charges must reflect the Arm’s Length Principle (ALP). This means:

• Services must generate value for the recipient.

• Charges should be based on benefit received, not merely cost incurred.

• Duplicated services (e.g., both parent and subsidiary performing the same task) are generally not deductible.

• Shareholder activities (like investor reporting, board meetings) are not chargeable to subsidiaries.

________________________________________

3. Methods for Pricing Intragroup Services

Common TP methods applied include:

• Cost Plus Method – charging actual cost plus an appropriate mark-up (most common).

• CUP (Comparable Uncontrolled Price) – if independent comparables for similar services exist.

• TNMM (Transactional Net Margin Method) – in cases where services are bundled or hard to price individually.

👉 Routine services (e.g., IT helpdesk, HR support) typically justify a low mark-up (3–8%), while high-value services (e.g., R&D, specialized advisory) may command higher returns.

________________________________________

4. Documentation Requirements in UAE

FTA expects intragroup services to be supported by robust documentation, including:

• Service Agreements – contracts outlining nature, scope, and pricing.

• Benefit Test Evidence – demonstrating commercial or economic value.

• Cost Allocation Keys – transparent allocation method across group entities (e.g., headcount, revenue).

• Invoices and Supporting Records – time sheets, reports, emails, usage logs.

• Benchmarking Studies – to support cost-plus mark-ups.

Without proper documentation, charges may be disallowed as non-arm’s length.

________________________________________

5. Transfer Pricing Adjustments

What are TP Adjustments?

TP adjustments are modifications made to align reported profits with the arm’s length principle. Adjustments can be:

• Primary Adjustments – made by the tax authority (e.g., disallowing excessive service charges).

• Secondary Adjustments – re-characterisation of transactions (e.g., treated as deemed dividend).

• Compensating Adjustments – voluntary corrections made by taxpayers to align with ALP.

When Do Adjustments Arise?

• If service fees are inflated or unsubstantiated.

• If duplicated or shareholder services are charged.

• If allocation keys are arbitrary and not benefit-driven.

• If group-wide services are charged without evidence of use.

________________________________________

6. UAE-Specific Considerations

• Free Zone Entities: Intragroup service arrangements must be arm’s length to qualify for 0% tax on Qualifying Income.

• Cross-Border Services: Ensure compliance with withholding tax rules in other jurisdictions, even though UAE does not levy WHT.

• Gold & Jewellery Industry: Shared back-office functions (HR, compliance, IT) should be properly allocated with support evidence.

• Family-Owned Groups: Important to separate shareholder activities (not chargeable) from genuine intragroup services.

________________________________________

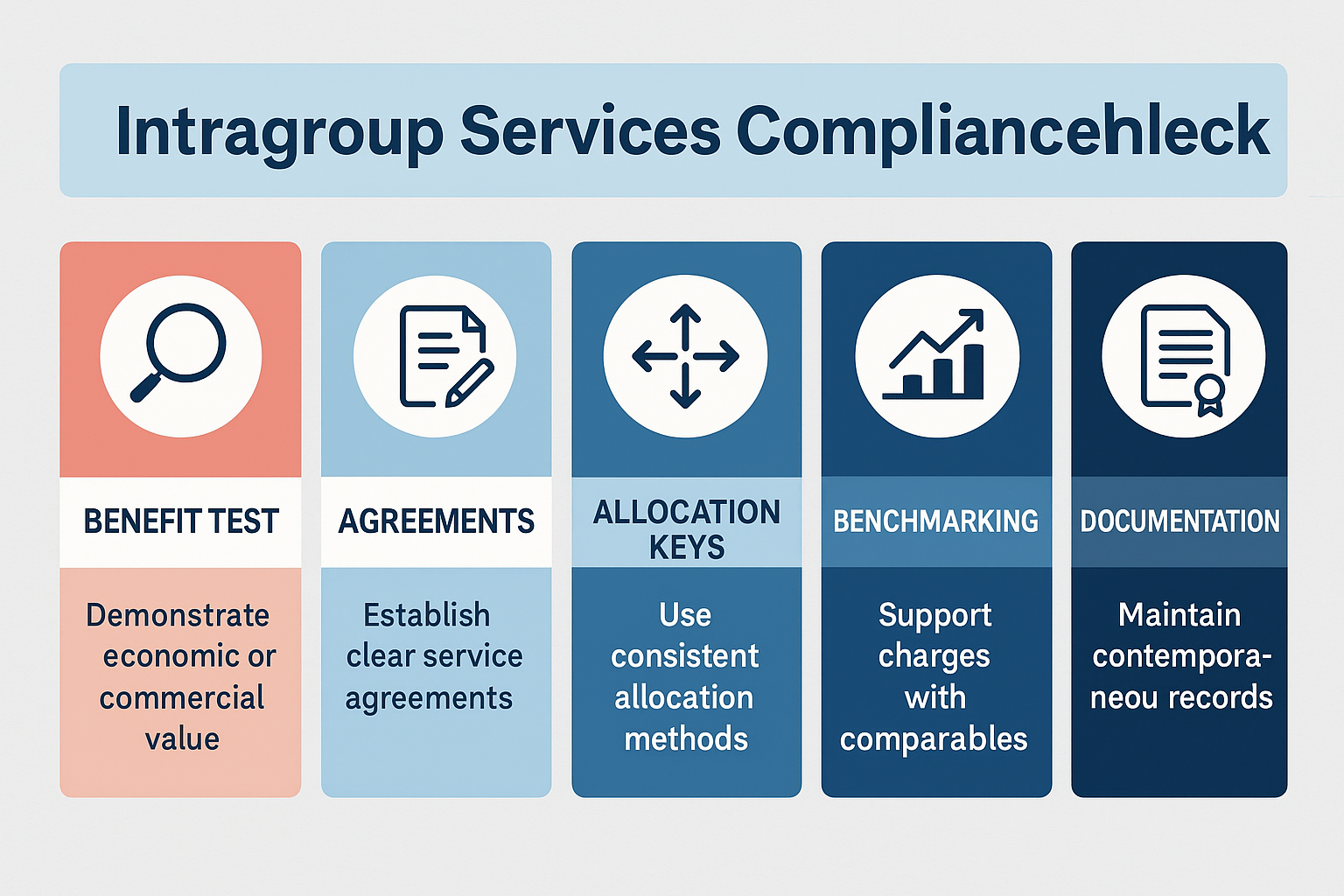

7. Best Practices to Avoid TP Adjustments

• Conduct a Benefit Test before charging services.

• Establish clear intragroup service agreements.

• Use consistent cost allocation keys across group companies.

• Benchmark cost-plus mark-ups against independent comparables.

• Maintain contemporaneous documentation for FTA audits.

• Perform year-end TP adjustments if results fall outside the arm’s length range.

________________________________________

✅ How Sheikh Anwar Accounting & Auditing LLC Can Help

At Sheikh Anwar Accounting & Auditing LLC, we help UAE businesses ensure their intragroup service arrangements are fully compliant with the Corporate Tax and TP framework.

Our Services Include:

• Drafting & reviewing intragroup service agreements.

• Conducting benefit tests and cost allocation analysis.

• Preparing benchmarking studies for service mark-ups.

• Assisting in TP documentation (Local File, Master File).

• Advising on compensating adjustments and audit defence.

📌 Contact Us Today

🌐 www.sa-auditors.com

✉️ info@sa-auditors.com | 📱 +971-XX-XXXXXXX

________________________________________

Conclusion

Intragroup services are a high-risk area for Transfer Pricing compliance in the UAE. Without strong evidence of benefits and arm’s length pricing, businesses may face TP adjustments and penalties. By adopting proper documentation and proactive compliance measures, companies can ensure tax efficiency while avoiding disputes.