Intercompany Loan Interest Deduction Rules

Introduction

In today’s interconnected business landscape, intercompany loans are widely used by group entities to manage liquidity, fund expansion, and optimize tax efficiency. However, the tax treatment of interest expenses on such loans is highly regulated to prevent base erosion and profit shifting (BEPS). As a leading advisory firm in the UAE, Sheikh Anwar Accounting and Auditing LLC explains the key rules, risks, and best practices surrounding intercompany loan interest deductions.

________________________________________

1️⃣ What Are Intercompany Loans?

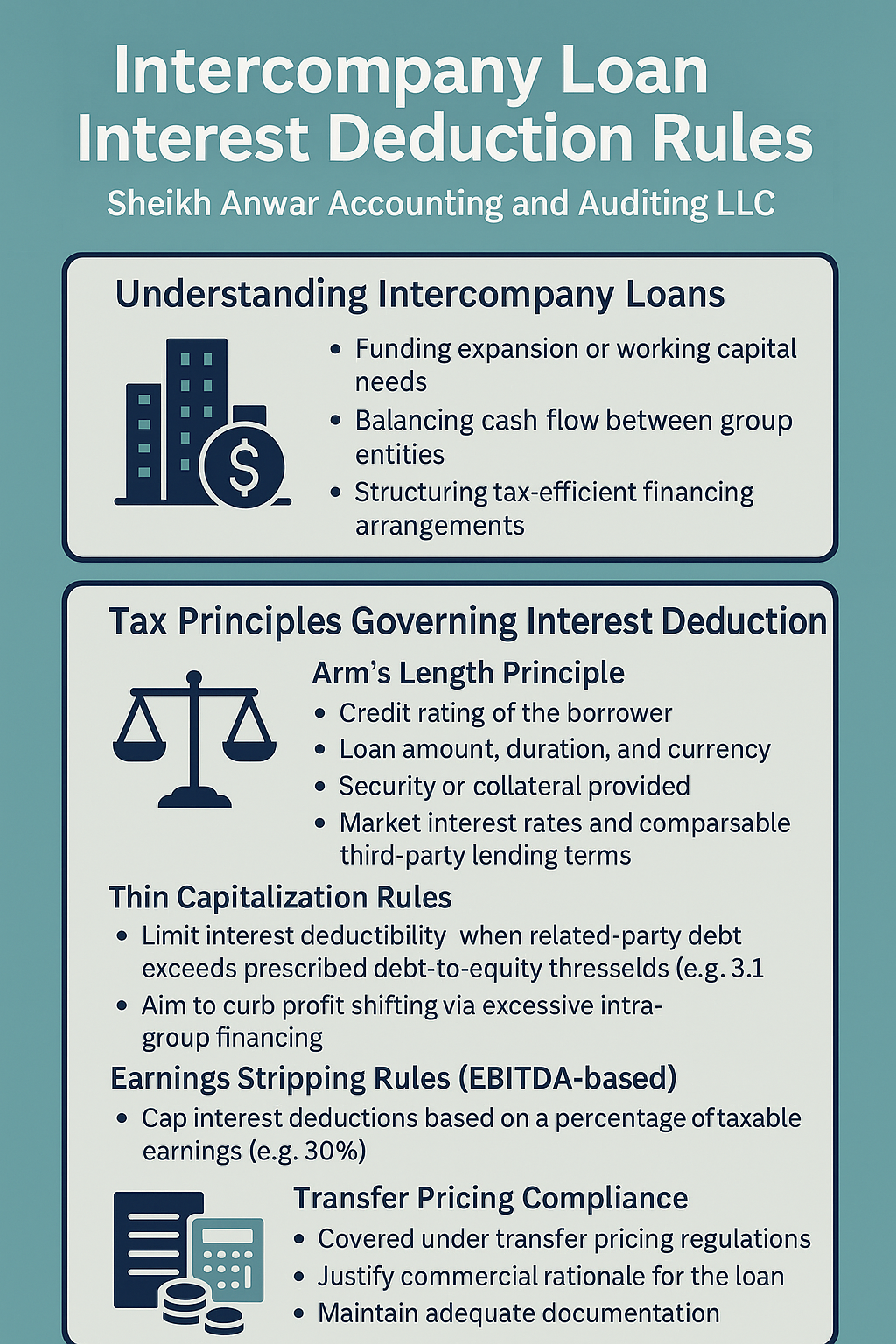

An intercompany loan is a financing arrangement where one entity within a corporate group lends funds to another entity in the same group. These loans can:

• Provide working capital support

• Finance investments or acquisitions

• Optimize tax positions within a group

While beneficial, tax authorities in the UAE and globally carefully examine interest deductions on such loans to ensure they are legitimate and at arm’s length.

________________________________________

2️⃣ Tax Principles Governing Interest Deduction

At Sheikh Anwar Accounting and Auditing LLC, we advise businesses to consider the following tax principles:

a) Arm’s Length Principle

Interest rates and terms on intercompany loans must reflect what independent third parties would agree to under similar circumstances.

Factors influencing arm’s length pricing include:

• Borrower’s credit rating

• Loan amount and duration

• Currency and collateral provided

• Market lending rates

Non-arm’s length interest rates may result in partial or full denial of deductions during tax assessments.

________________________________________

b) Thin Capitalization Rules

Many tax regimes, including those influencing UAE transfer pricing policies, restrict interest deductions when related-party debt exceeds certain debt-to-equity ratios (e.g., 3:1).

If these limits are breached, excess interest may be reclassified as non-deductible dividends.

________________________________________

c) Earnings Stripping Rules

Certain jurisdictions impose EBITDA-based restrictions, allowing deductions only up to 30% of taxable earnings, with excess amounts carried forward. UAE businesses operating globally need to consider these rules in their financing structures.

________________________________________

d) Transfer Pricing Documentation

Intercompany loans fall under transfer pricing regulations, requiring businesses to:

• Prepare loan agreements outlining terms and repayment schedules

• Benchmark interest rates using comparable market data

• Maintain supporting documentation for tax audits

Failure to comply can lead to penalties and disallowance of deductions.

________________________________________

3️⃣ Why Interest Deductions May Be Denied

Authorities may disallow deductions if:

• Interest rates exceed market norms

• Loans lack a genuine commercial purpose

• Loans are perpetual or structured as disguised equity

• Instruments create tax mismatches across jurisdictions

At Sheikh Anwar Accounting and Auditing LLC, we’ve seen businesses face disputes due to insufficient documentation or unrealistic interest terms on related-party financing.

________________________________________

4️⃣ Best Practices for UAE Businesses

To maximize deductibility and remain compliant, we recommend:

1. Drafting Comprehensive Loan Agreements with clear repayment terms and interest clauses.

2. Conducting Transfer Pricing Studies to determine arm’s length interest rates.

3. Monitoring Thin Capitalization Ratios to avoid excess debt classification issues.

4. Maintaining Evidence of Commercial Rationale for all intra-group loans.

5. Reviewing Cross-Border Tax Implications, including withholding taxes on outbound interest payments.

Our team at Sheikh Anwar Accounting and Auditing LLC assists clients in preparing transfer pricing documentation, benchmarking studies, and tax planning strategies to safeguard interest deductions.

________________________________________

5️⃣ Conclusion

Intercompany loans are an effective financing mechanism, but interest deductions are not guaranteed. Businesses must comply with:

• Arm’s length principles

• Thin capitalization and earnings stripping rules

• Transfer pricing documentation requirements

At Sheikh Anwar Accounting and Auditing LLC, we help companies structure intercompany financing arrangements to withstand tax authority scrutiny while optimizing tax positions.

________________________________________

📧 Email: info@sa-auditors.com

🌐 Website: www.sa-auditors.com

✅ Contact us today for expert advice on intercompany loan structuring, interest deductibility, and UAE corporate tax compliance.