Insurance Premiums – Are They Deductible?

Introduction

Businesses often spend significant amounts on insurance premiums to protect assets, employees, and operations from unforeseen risks. But when it comes to tax planning, one crucial question arises: Are insurance premiums deductible for tax purposes in the UAE?

Sheikh Anwar Accounting and Auditing LLC, a leading accounting and advisory firm in Dubai, provides a detailed explanation of insurance premium deductibility, accounting treatment, and UAE tax implications.

________________________________________

1️⃣ What Are Insurance Premiums?

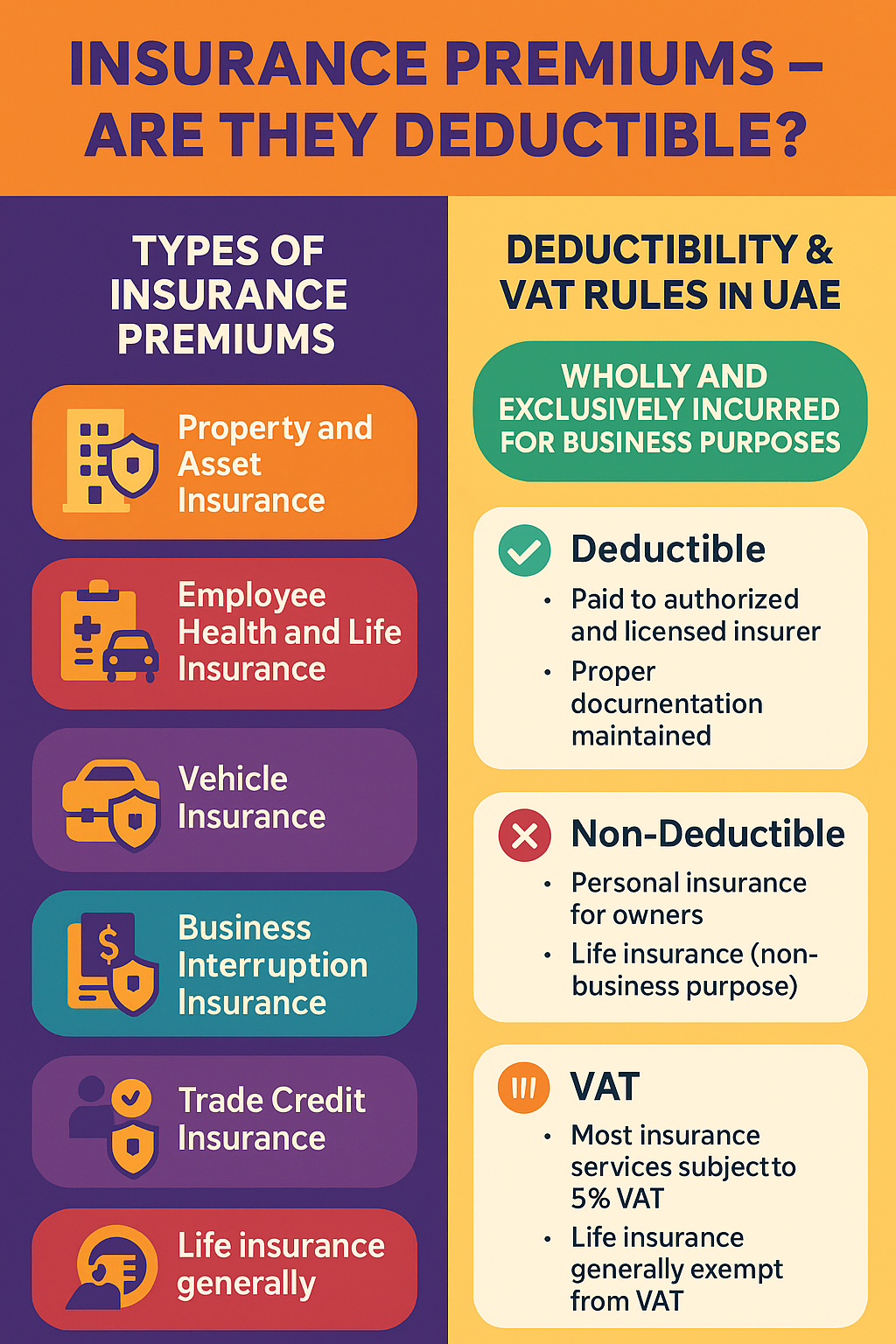

Insurance premiums are the amounts a business pays to an insurance company to cover risks associated with its operations. These payments can relate to:

• Property and asset insurance

• Employee health and life insurance

• Professional indemnity or liability insurance

• Vehicle and fleet insurance

• Business interruption coverage

Such premiums are essential for risk management and business continuity.

________________________________________

2️⃣ Types of Insurance Premiums for Businesses

1. Property and Asset Insurance – Covers damage to buildings, machinery, and equipment.

2. Employee Health and Life Insurance – Covers medical expenses and life protection for employees.

3. Vehicle Insurance – For company cars, trucks, and transport vehicles.

4. Professional Liability Insurance – Protects against claims arising from professional services.

5. Business Interruption Insurance – Provides compensation for loss of income due to unexpected disruptions.

6. Trade Credit Insurance – Covers the risk of non-payment by clients or customers.

________________________________________

3️⃣ Accounting Treatment of Insurance Premiums

• Insurance premiums are usually recorded as operating expenses under "Insurance Costs" in the Profit and Loss account.

• If the premium covers multiple accounting periods (e.g., annual policy), the expense is amortized proportionally over the coverage period.

• Refunds or rebates received from insurers are adjusted against the expense account.

________________________________________

4️⃣ Are Insurance Premiums Deductible for Corporate Tax in UAE?

Yes, insurance premiums are generally deductible for corporate tax purposes in the UAE, subject to certain conditions:

✅ Deductible Premiums:

• Must be wholly and exclusively incurred for business purposes.

• Payments must be to an authorized and licensed insurer.

• Proper documentation (policy, invoice, payment proof) must be available.

• Premiums for employee medical insurance (often mandatory in UAE) are fully deductible.

🚫 Non-Deductible Premiums:

• Personal insurance for owners or shareholders not linked to the business.

• Life insurance policies where the company or owners are the beneficiaries (non-business purpose).

• Fines or penalties charged by insurers due to policy breaches.

________________________________________

5️⃣ VAT Treatment of Insurance Premiums in UAE

• Most insurance services (except life insurance) are subject to 5% VAT in the UAE.

• Input VAT paid on insurance premiums is recoverable if the policy is for taxable business activities.

• Non-business-related insurance or employee leisure benefits may result in blocked VAT input.

• Life insurance premiums are generally exempt from VAT, meaning no input VAT recovery is available.

________________________________________

6️⃣ Documentation Requirements

To ensure deductibility and VAT recovery, businesses must maintain:

• Original insurance policy and premium invoices

• Proof of payment to the insurer

• Records showing the business purpose of the insurance

• Allocation details if insurance covers both personal and business elements

________________________________________

7️⃣ Common Mistakes to Avoid

• Claiming premiums for personal or mixed-use policies as full business expenses.

• Failing to proportionately allocate multi-year premiums.

• Ignoring VAT recovery opportunities for eligible insurance services.

• Missing documentation, leading to tax disallowances during audits.

________________________________________

8️⃣ Best Practices for Managing Insurance Premium Claims

1. Review insurance policies annually for coverage relevance.

2. Keep proper documentation for each premium payment.

3. Classify premiums correctly between deductible and non-deductible expenses.

4. Work with professional advisors for tax-efficient structuring of insurance coverage.

5. Ensure premiums are paid to licensed insurance providers only.

________________________________________

Conclusion

Insurance premiums are an important risk management tool for businesses. The UAE Corporate Tax law allows deductions for insurance premiums incurred wholly and exclusively for business purposes, subject to proper documentation. VAT input can also be recovered on eligible insurance services, improving tax efficiency.

At Sheikh Anwar Accounting and Auditing LLC, we help businesses analyze, classify, and optimize insurance premium expenses, ensuring maximum tax benefits and full compliance with UAE regulations.

________________________________________

📧 Email: info@sa-auditors.com

🌐 Website: www.sa-auditors.com