Importance of Periodic AML Risk Re-Assessments

Introduction

In the rapidly evolving world of financial crime and compliance, risk is never static.

What was considered low-risk last year may become high-risk today due to new regulations, customer behavior, or geopolitical developments.

That’s why Periodic AML Risk Re-Assessment is a critical element of every organization’s Anti-Money Laundering (AML) framework.

Under Federal Decree-Law No. (20) of 2018, Cabinet Decision No. (10) of 2019, and Cabinet Decision No. (109) of 2023, all Designated Non-Financial Businesses and Professions (DNFBPs)—including gold traders, real estate brokers, auditors, and lawyers—are legally required to review and update their AML risk assessments periodically.

This explains why periodic re-assessments are essential, when they should be done, and how businesses in the UAE can implement them effectively.

________________________________________

1. What Is an AML Risk Re-Assessment?

An AML Risk Re-Assessment is the process of re-evaluating existing money laundering and terrorist financing risks after the initial assessment has been completed.

It helps ensure that the organization’s understanding of its risks remains accurate, current, and aligned with regulatory expectations.

A re-assessment involves reviewing and updating:

• Customer risk profiles

• Product and service risk

• Geographical exposure

• Delivery channels

• Effectiveness of AML controls

________________________________________

2. Why Periodic Re-Assessments Are Crucial

a. Dynamic Nature of Money Laundering Risks

Money laundering techniques evolve continuously. Criminals exploit new products, technologies, and loopholes.

For example:

• The rise of virtual assets and digital payments has created new laundering channels.

• Political shifts may change country risk ratings overnight.

Re-assessing risks ensures your AML framework adapts to these new realities.

________________________________________

b. Regulatory Compliance

UAE AML regulations explicitly require DNFBPs to maintain updated AML risk assessments.

During Ministry of Economy (MOE) inspections, businesses must demonstrate:

• The date of the last AML risk assessment.

• Evidence of periodic updates.

• Documentation showing changes in risk levels and mitigation measures.

Failure to conduct periodic reviews can result in non-compliance penalties and reputational damage.

________________________________________

c. Changes in Business Operations

As your business evolves, so do your risks. Examples include:

• Launching new services (e.g., online trading).

• Expanding to new countries or markets.

• Onboarding new types of clients (e.g., foreign entities).

Periodic risk re-assessments ensure these operational changes are reflected in your AML controls.

________________________________________

d. Emerging Regulatory and FATF Updates

The Financial Action Task Force (FATF) frequently updates its guidance, grey/black lists, and risk indicators.

A country that was low-risk last year could now be on the FATF grey list, directly impacting your geographic risk.

Re-assessments ensure your framework remains aligned with the latest FATF and UAE FIU directives.

________________________________________

e. Identifying Weaknesses in AML Controls

Regular re-assessments highlight whether existing controls are still effective.

For instance:

• Is your Customer Due Diligence (CDD) still robust enough?

• Are your transaction monitoring systems detecting red flags efficiently?

Periodic reviews enable timely corrective actions before compliance gaps widen.

________________________________________

f. Enhancing Regulatory Confidence

Businesses that perform regular risk re-assessments show regulators they take AML compliance seriously.

This proactive approach:

• Demonstrates strong governance and accountability.

• Builds trust with banks and regulators.

• Simplifies AML audits and inspections.

________________________________________

3. When Should AML Risk Re-Assessments Be Conducted?

While the UAE AML Law doesn’t specify an exact interval, international best practices and MOE expectations recommend:

Scenario Recommended Re-Assessment Frequency

Routine AML review Annually

Launch of new products or services Immediately upon introduction

Expansion to new geographic markets Within 1–3 months

FATF or MOE regulatory updates As soon as changes occur

Major organizational restructuring Post-change review

Detection of suspicious activity or STR After internal investigation

Regular re-assessment ensures continuous compliance, not just “one-time readiness.”

________________________________________

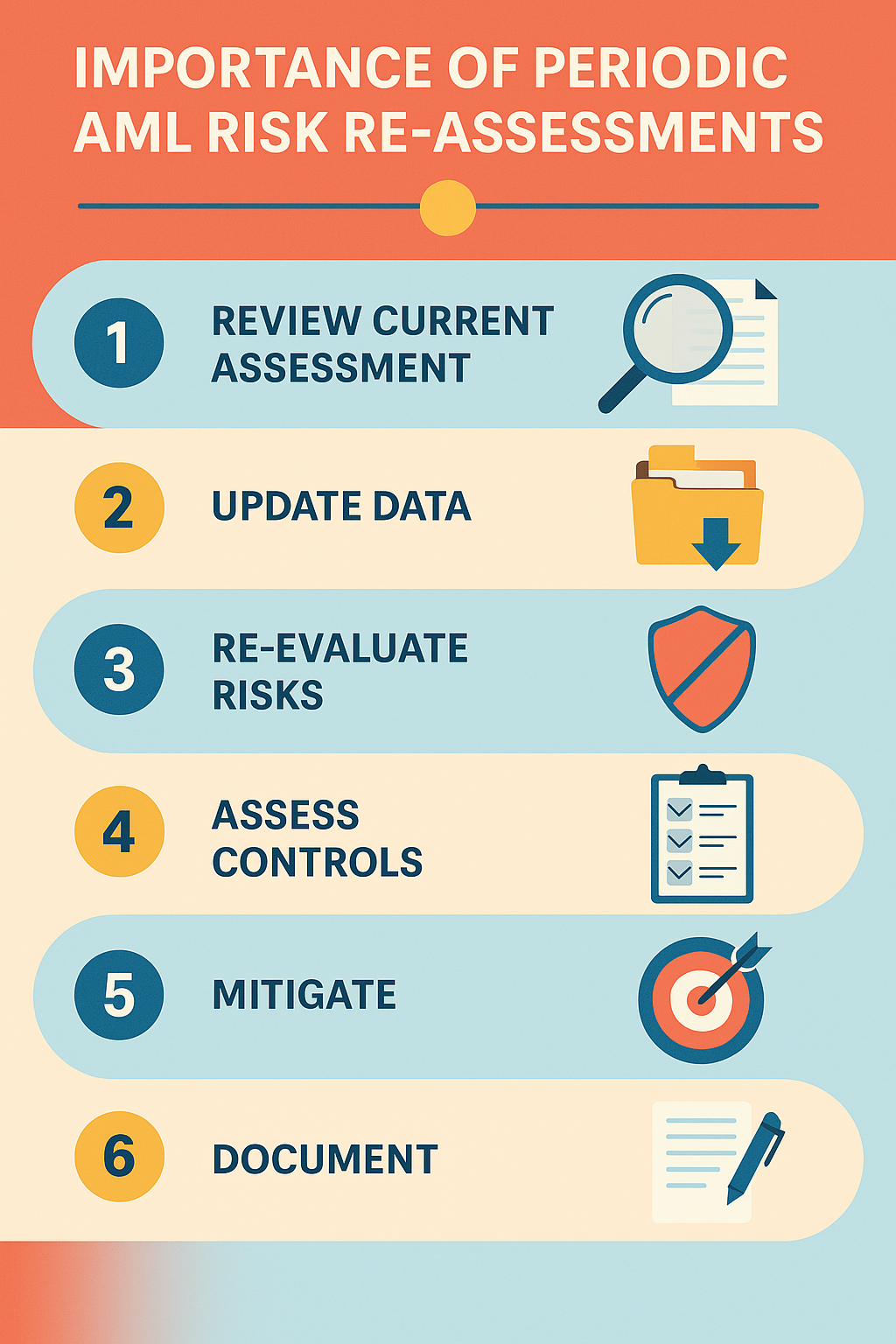

4. Key Steps to Conduct an AML Risk Re-Assessment

Step 1 – Review Current Risk Assessment

Start with your existing AML risk assessment report.

Evaluate whether the risk categories (customer, product, geography, transaction, delivery channel) still reflect current realities.

________________________________________

Step 2 – Gather Updated Data

Collect new information such as:

• Updated customer lists and classifications.

• Recent FATF and sanctions updates.

• Internal audit findings.

• Transaction monitoring reports.

Data accuracy is crucial for valid re-assessment results.

________________________________________

Step 3 – Re-Evaluate Inherent Risks

Recalculate risk levels for each category using your scoring model.

For example:

Risk Area Previous Rating Updated Rating Reason

Geographic Risk Medium High Client expansion to FATF grey-listed country

Product Risk Low Medium Introduction of new cash-based product

________________________________________

Step 4 – Assess Control Effectiveness

Test whether existing AML controls are functioning as intended:

• Is staff training updated?

• Are PEP and sanctions screening tools current?

• Are STR filing processes effective?

Assign control effectiveness ratings (Strong / Moderate / Weak).

________________________________________

Step 5 – Determine Residual Risk

After considering control effectiveness, determine the residual risk level for each category.

Residual risk = Inherent Risk – Control Strength

Document changes and note any increase or decrease in overall risk exposure.

________________________________________

Step 6 – Update Mitigation Plans

If new or higher risks are identified:

• Strengthen CDD/EDD procedures.

• Upgrade AML software or transaction monitoring tools.

• Increase audit frequency or staff training.

• Introduce new internal approval layers for high-risk clients.

________________________________________

Step 7 – Document and Obtain Approval

Prepare an updated AML Risk Assessment Report that includes:

• Summary of key changes.

• Updated risk matrix.

• Revised mitigation measures.

• Approval from senior management or MLRO.

Keep both soft and hard copies ready for inspection by authorities.

________________________________________

5. Technology’s Role in AML Re-Assessment

Modern AML platforms such as MyAML.io and Finabooks.com simplify re-assessments through:

• Automated customer risk scoring.

• Real-time sanctions and PEP screening.

• AI-driven transaction analytics.

• Auto-generated AML Risk Re-Assessment Reports.

• Version tracking and digital documentation for audits.

Automation ensures consistency, speed, and accuracy, allowing compliance officers to focus on risk analysis rather than manual paperwork.

________________________________________

6. Common Mistakes in AML Re-Assessments

1. Treating risk re-assessment as a formality.

2. Copying the previous year’s report without actual updates.

3. Ignoring changes in customer base or geography.

4. Not obtaining management sign-off.

5. Failing to link re-assessment findings to policy updates.

Such oversights can trigger compliance penalties during MOE audits.

________________________________________

7. Benefits of Regular AML Re-Assessments

✅ Ensures ongoing regulatory compliance.

✅ Enhances early detection of emerging ML/TF risks.

✅ Improves efficiency of AML monitoring systems.

✅ Demonstrates proactive governance and accountability.

✅ Strengthens business reputation and credibility.

________________________________________

8. Documentation and Retention

Keep comprehensive records of:

• Re-assessment reports and summaries.

• Supporting data and risk matrices.

• Approval minutes from senior management.

• Evidence of policy or control updates.

As per UAE AML law, maintain documentation for at least five years from the date of assessment.

________________________________________

Conclusion

Periodic AML Risk Re-Assessments are not just regulatory requirements—they are essential tools for protecting businesses from financial crime, maintaining compliance, and building institutional integrity.

By adopting a structured, data-driven, and technology-enabled approach to risk re-assessment, DNFBPs can stay one step ahead of evolving threats and remain fully aligned with UAE AML regulations and FATF best practices.

________________________________________

Sheikh Anwar Accounting & Auditing LLC

Licensed Auditor – Ministry of Economy (Entry No. 5817)

📍 Dubai Creek Tower, Office M35, Dubai, UAE

🌐 www.sa-auditors.com

✉️ info@sa-auditors.com