Impact of Anti-Abuse Rules on Free Zones

Introduction

The UAE Corporate Tax regime offers generous incentives for Free Zone businesses, including a 0% tax rate for Qualifying Free Zone Persons (QFZPs). However, to prevent misuse, the law introduces strict General Anti-Abuse Rules (GAAR).

Here, we explore the impact of anti-abuse rules on Free Zone entities, the risks of structuring for tax benefits, and how companies can mitigate exposure.

________________________________________

⚖️ Legal Foundation

The UAE Corporate Tax Law (Federal Decree-Law No. 47 of 2022) includes a General Anti-Abuse Rule (GAAR) under Article 50, which empowers the Federal Tax Authority (FTA) to counteract tax advantages arising from artificial or non-genuine arrangements.

Key references:

• Article 50 – General Anti-Abuse Rule

• Cabinet Decision No. 75 of 2023 (GAAR guidance)

• Ministerial Decision No. 139 of 2023 (QFZP qualifying activities)

• FTA Public Clarifications (on QFZPs and structuring)

________________________________________

🧠 What is the GAAR?

The General Anti-Abuse Rule allows the FTA to recharacterize or disregard arrangements if:

“It can be reasonably concluded that the main purpose or one of the main purposes of the arrangement is to obtain a Corporate Tax advantage that is not consistent with the intention of the law.”

In simpler terms, even if your structure complies with the literal wording of the law, the FTA can deny the benefit if the structure is:

• Artificial or contrived

• Lacks economic substance

• Doesn’t align with business reality

________________________________________

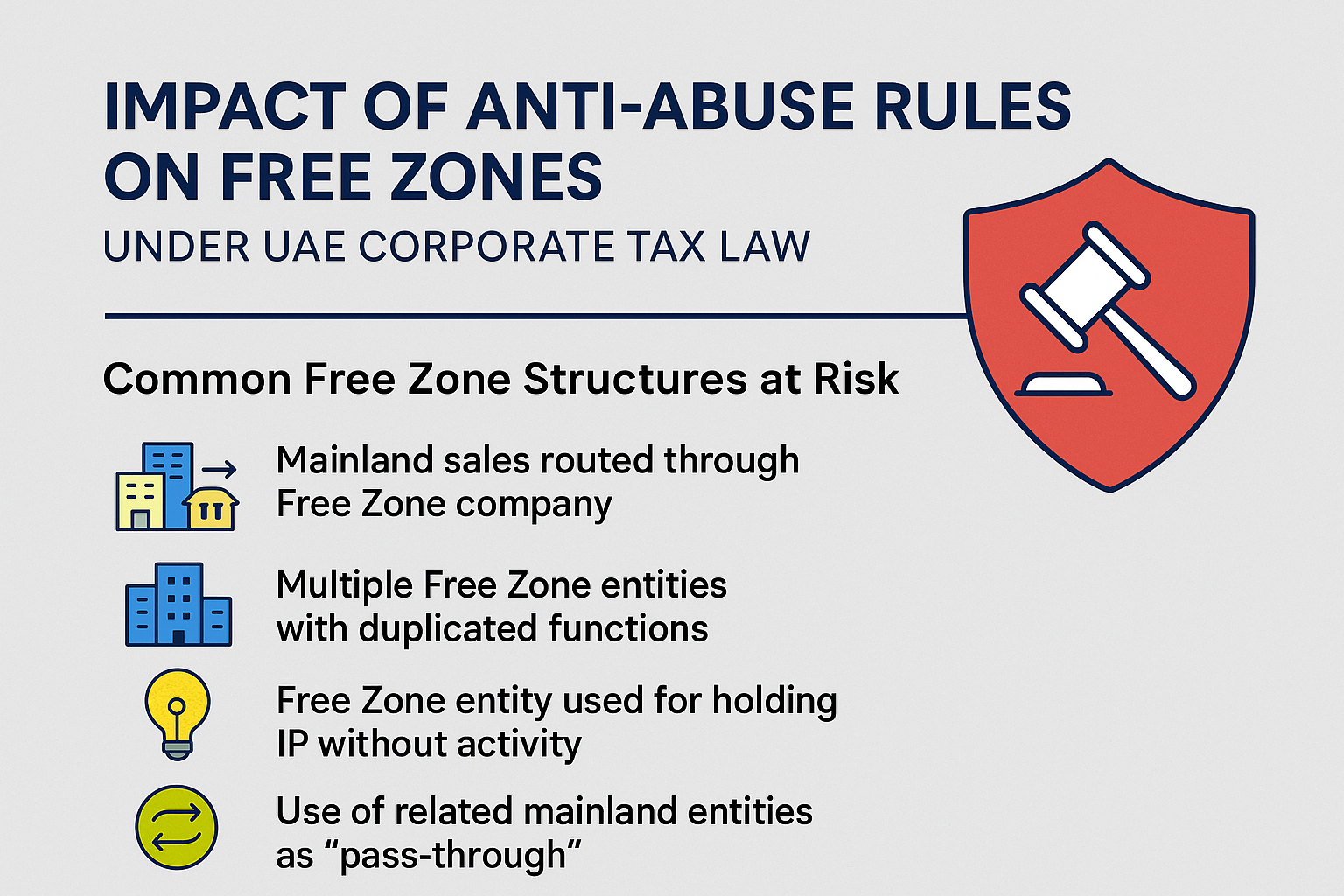

🏗️ Common Free Zone Structures at Risk

1️⃣ Mainland Sales Routed through Free Zone Company

Example: A group sells goods to mainland customers via a Free Zone company just to benefit from the 0% rate.

• 🚨 Red Flag: No operational substance in Free Zone.

• ⚠️ GAAR Risk: FTA may treat the structure as tax-motivated and apply 9% tax.

________________________________________

2️⃣ Multiple Free Zone Entities with Duplicated Functions

Example: Setting up several Free Zone companies performing the same or similar activities without commercial need.

• 🚨 Red Flag: Fragmented invoicing to lower taxable income.

• ⚠️ GAAR Risk: FTA may consolidate or disregard entities.

________________________________________

3️⃣ Free Zone Entity Used for Holding IP Without Activity

Example: A company holds trademarks, patents, or software in a Free Zone entity to shift profits via royalty income.

• 🚨 Red Flag: No R&D or active asset development in Free Zone.

• ⚠️ GAAR Risk: Royalty income may be recharacterized as non-qualifying.

________________________________________

4️⃣ Use of Related Mainland Entities as ‘Pass-through’

Example: Mainland company acts as a sales agent for Free Zone parent, merely passing on income to claim it as Free Zone revenue.

• 🚨 Red Flag: Functions and risks borne by mainland entity.

• ⚠️ GAAR Risk: FTA may tax income in mainland entity.

________________________________________

🧾 FTA Powers Under GAAR

The FTA can take the following actions under Article 50:

FTA Action Description

Disregard an arrangement Treat transaction as if it never occurred

Recharacterize income Assign taxable income to the economically active party

Adjust tax liability Deny tax benefits that arise from the structure

Deny QFZP status Revoke 0% tax benefit even if formal conditions are met

These decisions are made retrospectively and can apply even if a structure was pre-approved, unless substance is demonstrated.

________________________________________

🧠 How to Reduce GAAR Exposure

Compliance Area Best Practice

Economic Substance Ensure employees, premises, and real operations exist in Free Zone

Commercial Purpose Document real business rationale for each entity and transaction

Transparent Documentation Maintain board minutes, service agreements, transfer pricing reports

Income Segregation Clearly separate qualifying and non-qualifying income

Avoid Circular Transactions No artificial movement of funds between group entities

Annual QFZP Review Perform internal review to test GAAR risk and substance

________________________________________

📌 Summary

GAAR introduces a "substance over form" test — Free Zone entities must prove genuine economic activity and purpose to retain corporate tax benefits. The 0% QFZP rate is not an entitlement; it’s a conditional incentive based on commercial reality.

________________________________________

🧑💼 Need Help Navigating GAAR?

At Sheikh Anwar Accounting and Auditing LLC, we help Free Zone companies:

• Review their structures for GAAR exposure

• Establish and document economic substance

• Conduct QFZP eligibility checks

• Prepare audit-ready files and Transfer Pricing reports

📧 Email: info@sa-auditors.com

🌐 Website: https://www.sa-auditors.com