How to Verify RCM on Your VAT Return

Introduction

The Reverse Charge Mechanism (RCM) plays a crucial role in VAT compliance, especially when dealing with cross-border transactions. However, many businesses fail to verify RCM entries properly in their VAT Return (Form 201), leading to mismatches and potential penalties.

It will walk you through the step-by-step process of verifying RCM entries in your VAT return to ensure everything is accurate and compliant.

________________________________________

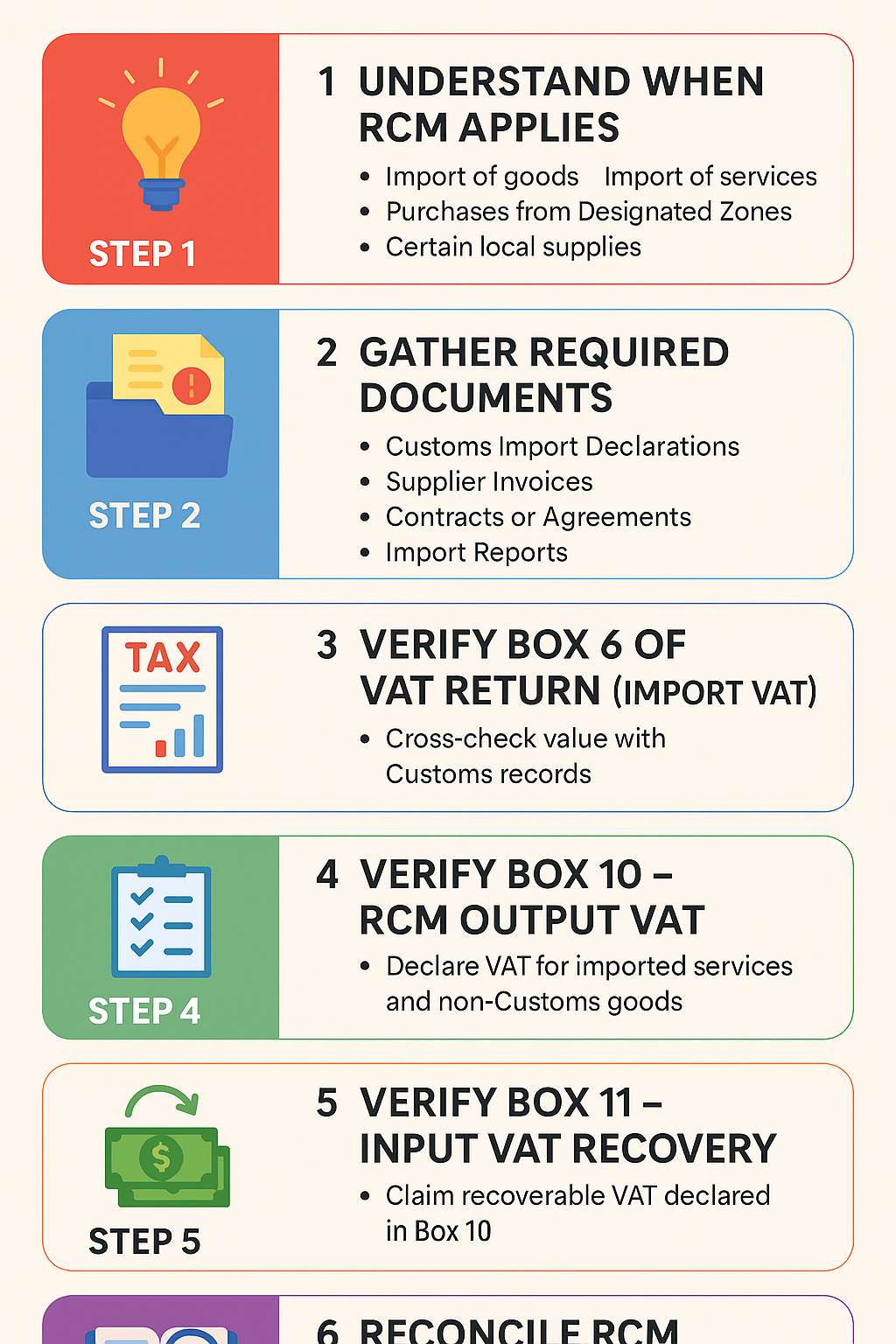

📌 Step 1: Understand When RCM Applies

Before you verify, know when RCM is relevant:

RCM typically applies to:

• Import of goods into the UAE (Customs-cleared)

• Import of services from outside the UAE

• Purchases from Designated Zones (if supply is considered to take place in UAE)

• Certain notified local supplies (e.g., crude oil, gold, hydrocarbons)

________________________________________

🗂 Step 2: Gather Required Documents

Collect and review the documents related to RCM transactions:

• Customs Import Declarations (Bills of Entry)

• Supplier Invoices from overseas vendors

• Contracts or Agreements for cross-border services

• Emirates Import Code Reports (from UAE Customs)

• Internal ledger entries

________________________________________

🧾 Step 3: Verify Box 6 of VAT Return (Import VAT)

This box is auto-populated in Form 201 based on your Customs records. It shows the VAT calculated on goods imported into the UAE.

✔️ Cross-check this value with:

• Total VAT from customs bills of entry (for the period)

• Emirates Import Report (downloadable from EmaraTax)

________________________________________

📤 Step 4: Verify Box 10 – RCM Output VAT

You must manually declare VAT under RCM for:

• Imported services

• Goods purchased from Free Zones or foreign suppliers (non-Customs)

✔️ Verify that:

• All applicable invoices are included

• Correct VAT rate (usually 5%) is applied

• Amount aligns with your input VAT claim

________________________________________

📥 Step 5: Verify Box 11 – Input VAT Recovery

This is where you recover the same VAT declared in Box 10 if you’re eligible (i.e., you make taxable supplies).

✔️ Confirm that:

• Only recoverable Input VAT is claimed

• There is no claim on exempt/non-business use

• Matching entries exist in Box 10

________________________________________

🔍 Step 6: Reconcile RCM Ledger Entries

Internally, you should maintain a Reverse Charge Ledger or Journal that:

• Lists every RCM transaction by date, supplier, and amount

• Shows Output VAT and matching Input VAT

• Helps you reconcile monthly or quarterly with VAT Return

________________________________________

📊 Sample RCM Journal Entry

Date Supplier Description Value (AED) Output VAT (AED) Input VAT (AED)

10-Jun-24 ABC Ltd (UK) Legal Consultancy 10,000 500 500

________________________________________

⚠️ Common Errors to Avoid

❌ Missing imported service entries in Box 10

❌ Claiming VAT without eligible use in Box 11

❌ Mismatch between Customs data and Box 6

❌ Double claiming RCM entries

________________________________________

✅ Best Practices

✔ Review all overseas supplier invoices each return period

✔ Match Customs VAT data to Box 6 entries

✔ Maintain a dedicated RCM ledger

✔ Consult your VAT advisor in case of uncertainty

________________________________________

🧠 Conclusion

Verifying RCM in your VAT return is essential to ensure full compliance and avoid unnecessary penalties. While the process may seem technical, a structured approach, good recordkeeping, and periodic reconciliation can help you stay fully compliant with UAE VAT laws.

🌐 Visit us: www.sa-auditors.com

📧 Email: info@sa-auditors.com

📱 WhatsApp: +971-XX-XXXXXXX