How to Report RCM in VAT Return Form 201

Introduction

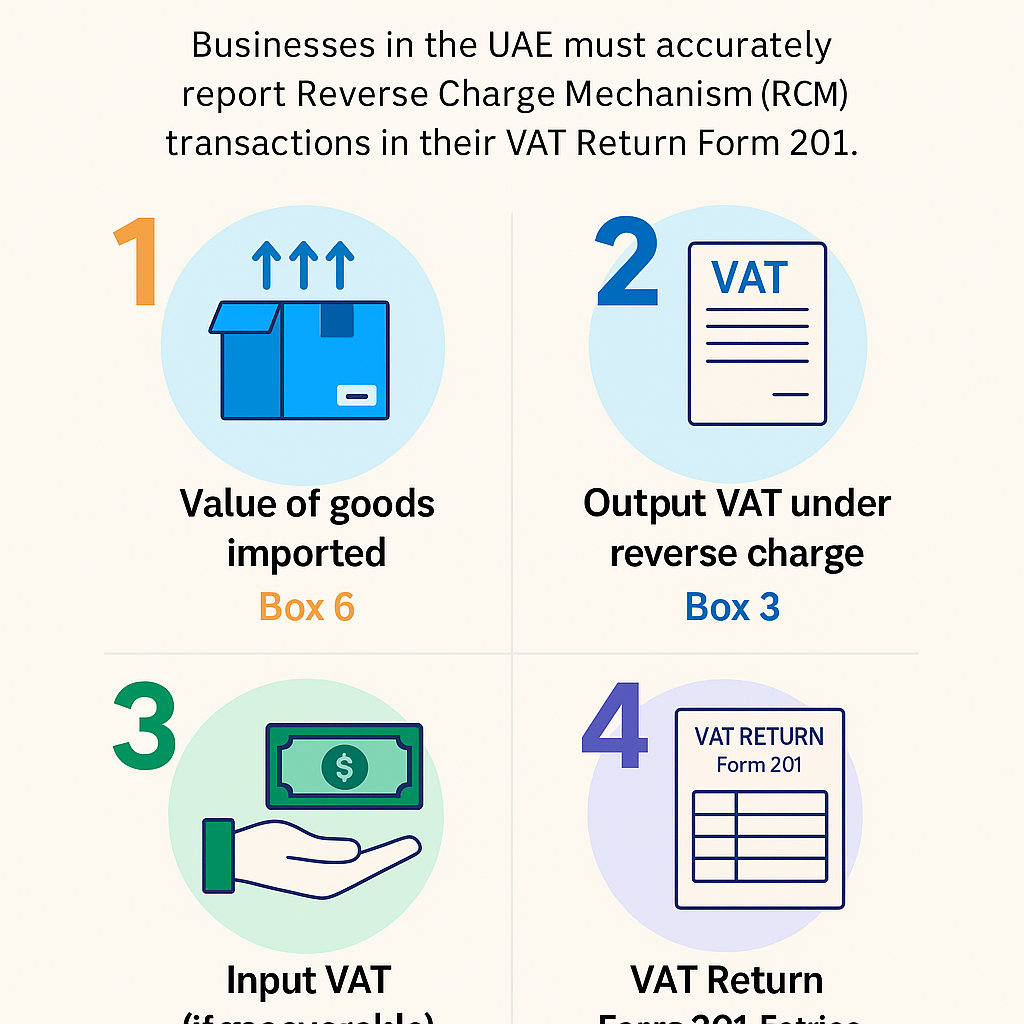

Businesses in the UAE that import goods or services from overseas must comply with the Reverse Charge Mechanism (RCM) requirements under the UAE VAT Law. While RCM does not always involve a cash transaction, it must still be accurately reported in your VAT Return Form 201.

Here, we explain step-by-step how to report RCM transactions properly in your VAT return, including which boxes to fill, how to calculate the tax, and common errors to avoid.

________________________________________

✅ What Is RCM and Why It Must Be Reported

Under the Reverse Charge Mechanism, the responsibility to report and pay VAT shifts from the foreign supplier to the UAE-based buyer. Though no VAT is charged on the invoice, the UAE business must:

1. Declare output VAT (as if they were the supplier), and

2. Claim input VAT (if eligible for recovery)

This ensures that imports are taxed the same way as domestic supplies.

________________________________________

📥 When RCM Applies (Quick Recap)

• Import of goods from outside UAE

• Import of services from foreign providers

• Supplies of gold, diamonds, and hydrocarbons under special RCM conditions

• Supplies involving Designated Zones in some cases

________________________________________

🧾 RCM Reporting in VAT Return Form 201

The VAT Return Form 201 is submitted through the EmaraTax portal on the Federal Tax Authority (FTA) website. The form has specific fields where RCM-related entries must be made.

________________________________________

📌 Key VAT Return Boxes for RCM

Description VAT Return Box # What to Enter

Value of goods imported Box 6 Total customs-declared import value

Output VAT under reverse charge Box 3 VAT @ 5% on imported goods/services

Input VAT (if recoverable) Box 10 / 11 Reclaim the same VAT amount (if eligible)

________________________________________

🧮 Step-by-Step Example

Scenario:

A UAE VAT-registered company imports software services worth AED 20,000 from a US-based provider.

Step 1: Calculate Reverse Charge VAT

• 5% of AED 20,000 = AED 1,000

Step 2: Report in Form 201

• Box 3 (Output VAT): AED 1,000

• Box 6 (Value of import): AED 20,000

• Box 10 or 11 (Input VAT): AED 1,000 (if eligible)

Final Result:

No net VAT payable, but correct reporting is mandatory.

________________________________________

📑 Supporting Documents to Keep for RCM

To avoid issues during FTA audits, retain:

• Supplier invoices from abroad

• Customs BOE (for goods)

• Service agreements/contracts

• Proof of payment (bank remittance)

• RCM accounting journal entries

________________________________________

❌ Common Mistakes to Avoid

• Failing to report imported services in Box 3

• Skipping Box 6 for goods imported via customs

• Claiming input VAT without declaring output VAT

• Misplacing RCM entries in other boxes

• Overstating VAT recovery on non-taxable use

________________________________________

🧠 Pro Tips for Accurate RCM Reporting

• Use VAT301 Declaration Form to reconcile with customs records

• Reconcile your BOEs (Bill of Entry) monthly with accounting software

• Keep separate RCM ledgers for tracking imports

• Use an FTA-compliant ERP system to auto-populate return data

________________________________________

📆 When to File

The VAT return (Form 201) is filed quarterly or monthly, depending on your tax period. Ensure RCM entries are made in the return period corresponding to the invoice date or customs clearance date.

________________________________________

🎯 Final Thoughts

Correctly reporting RCM transactions in VAT Return Form 201 is crucial for compliance with UAE VAT regulations. Even if the VAT impact is neutral, accurate disclosure ensures audit readiness and avoids administrative penalties.

________________________________________

💼 Need Help with RCM or VAT Filing?

At Sheikh Anwar Accounting & Auditing LLC, we help businesses manage RCM entries, reconcile customs data, and file VAT returns accurately. Contact us today for professional VAT return filing and advisory services.

🌐 Visit us: www.sa-auditors.com

📧 Email: info@sa-auditors.com

📱 WhatsApp: +971-XX-XXXXXXX