How to Issue VAT Invoice for Advance Payment

Introduction

In the UAE, Value Added Tax (VAT) applies not just when goods are delivered or services are rendered, but also when advance payments are received. As per UAE VAT Law, when a business receives full or partial payment in advance, a VAT invoice must be issued — even if the supply is to happen in the future.

Here we explain when and how to issue a VAT invoice for advance payments, what to include, and how to report it in your VAT return (Form 201).

📘 What Is an Advance Payment?

An advance payment (or down payment) is money received before the actual supply of goods or services takes place. It may be partial or full and is treated as a taxable event under UAE VAT.

✅ When Is VAT Due on Advance Payments?

According to Article 25(1)(b) of the UAE VAT Law:

VAT becomes due on the earlier of:

The date of issuance of the tax invoice, or

The date the payment is received, whether in full or part.

➡️ This means: If a business receives an advance, it must issue a tax invoice and charge VAT at that point — even if the delivery/service is scheduled later.

🧾 Steps to Issue VAT Invoice for Advance Payments

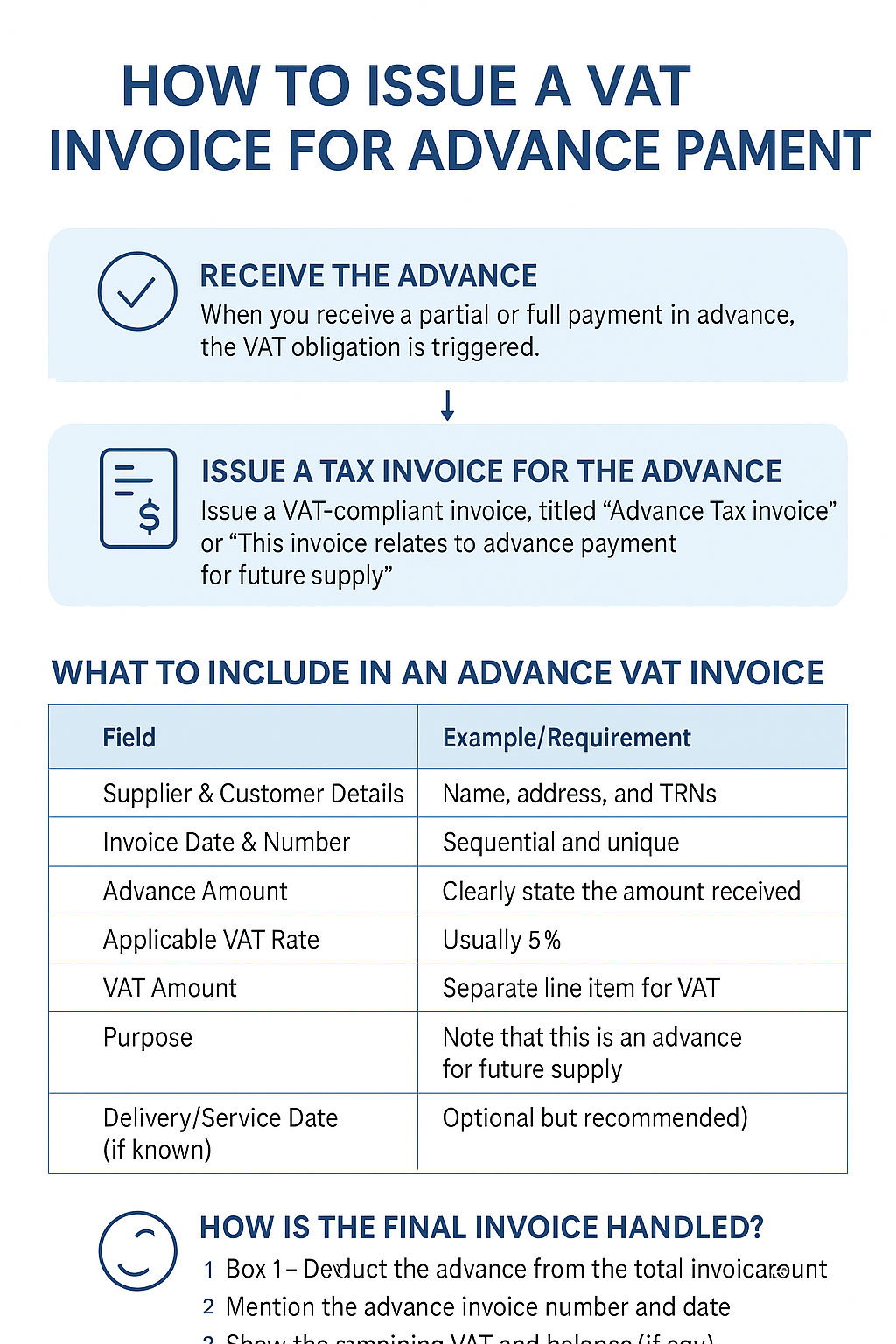

Step 1: Receive the Advance

Once you receive a partial or full payment in advance from your customer (whether B2B or B2C), the VAT obligation is triggered.

Step 2: Issue a Tax Invoice for the Advance

You must issue a VAT-compliant invoice, but clearly indicate that it relates to an advance.

📌 The invoice should be titled either:

“Advance Tax Invoice”, or

A regular tax invoice with a reference such as:

"This invoice relates to advance payment for future supply of [goods/services]."

📋 What to Include in an Advance VAT Invoice?

Field Example/Requirement

Supplier & Customer Details Name, address, and TRNs

Invoice Date & Number Sequential and unique

Advance Amount Clearly state the amount received

Applicable VAT Rate Usually 5%

VAT Amount Separate line item for VAT

Purpose Note that this is an advance for future supply

Delivery/Service Date (if known) Optional but recommended

Balance Due (optional) To be shown in future final invoice

🔄 How Is the Final Invoice Handled?

When the full supply is made, issue the final invoice, and:

Deduct the advance from the total invoice amount

Mention the advance invoice number and date

Show the remaining VAT and balance (if any)

Example:

Item Amount

Total value of goods AED 10,000

Less: Advance (incl. VAT) AED 2,100

Net payable now AED 7,900

🧾 Reporting in VAT Return (Form 201)

Box 1 – Declare the advance VAT collected in the tax period when the advance was received.

Box 6 – Show total output VAT due.

On final supply, only report the balance if the advance has already been taxed.

⚠️ Do not double-count the VAT in two different periods.

💡 Special Considerations

Scenario VAT Treatment

Advance is refunded before supply Adjust using credit note and reverse VAT

Supply is to another GCC country Reverse charge may apply based on implementation status

Multiple advances for one project Issue separate advance invoices or track with a schedule

No invoice issued but advance received VAT is still due on payment receipt date

⚠️ Common Mistakes to Avoid

Mistake Risk

Not issuing a tax invoice on advance VAT non-compliance

Charging VAT only on final invoice Underreporting of tax in prior period

Double taxing same amount Overpayment and reconciliation issues

Omitting reference to advance on final invoice Audit challenges

✅ Best Practices

Use VAT-compliant invoicing software to automate advance tracking (e.g., Finabooks)

Maintain customer advance ledger

Cross-reference advance and final invoices

Reconcile VAT liability monthly based on invoices and payments

🧠 Final Thoughts

Issuing a VAT invoice for advance payments is not just a good practice—it is a legal obligation under UAE VAT law. Businesses must track and report such advances accurately to avoid penalties or discrepancies during FTA audits.

💼 Need help automating VAT invoicing or managing customer advances in your accounts?

Contact Sheikh Anwar Accounting & Auditing LLC for expert support in VAT compliance, accounting automation, and FTA audit readiness.