How to Account for RCM in Your Books

Introduction

The Reverse Charge Mechanism (RCM) under UAE VAT is a compliance-critical area for businesses that deal with imports and certain types of local or international transactions. Unlike regular VAT, where the supplier charges VAT, under RCM, the buyer is responsible for self-assessing and recording the VAT.

Here we will walk you through the accounting treatment of RCM transactions, step-by-step, with journal entries and best practices.

________________________________________

🔍 When Does RCM Apply?

RCM typically applies in the following scenarios:

• Import of goods from outside the UAE

• Import of services from foreign suppliers

• Certain domestic supplies (e.g., crude oil, hydrocarbons, gold & diamonds, etc.)

• Purchases from non-registered UAE suppliers

________________________________________

🧾 Key Concepts to Understand

• Output VAT under RCM is accounted for by the buyer and paid to the FTA.

• Input VAT may be recoverable in the same return, provided the goods/services are used for taxable business purposes.

• These entries are often "net neutral", meaning no payment is due if fully recoverable.

________________________________________

📊 RCM Accounting – Step-by-Step

Let’s break it down using an example:

📦 Scenario:

Your company receives design services from a UK supplier worth AED 10,000. The UK supplier is not VAT-registered in the UAE.

✅ VAT Rate: 5%

________________________________________

1. Journal Entries

At the time of recording the invoice:

Dr. Expense / Service Account – AED 10,000

Cr. Accounts Payable (UK Supplier) – AED 10,000

At the time of accounting for RCM:

Dr. Input VAT (Reverse Charge) – AED 500

Cr. Output VAT (Reverse Charge) – AED 500

💡 This means you are "paying" VAT to FTA and simultaneously recovering it if eligible.

________________________________________

2. If Input VAT is Not Recoverable

In case the service is used for non-taxable purposes (e.g., exempt supplies):

Dr. Input VAT (Reverse Charge) – AED 500

Cr. Output VAT (Reverse Charge) – AED 500

Dr. Expense Account (Non-Recoverable VAT) – AED 500

Cr. Input VAT (Disallowable) – AED 500

________________________________________

3. RCM in VAT Return (Form 201)

Box No. Description Action Required

Box 3 Imports subject to VAT at Customs Add import value

Box 6 Supplies subject to RCM Declare service value

Box 10 Recoverable Input VAT Claim eligible input

________________________________________

🧮 Accounting Software Tips

• Use VAT-compliant software that supports RCM treatment.

• Make sure your chart of accounts includes:

o RCM Input VAT Ledger

o RCM Output VAT Ledger

o RCM Suspense or Control Account (optional)

________________________________________

📌 Best Practices

1. Create vendor types (local vs. international) in your system.

2. Use tax codes like “RCM-G” (goods) and “RCM-S” (services).

3. Maintain reverse charge invoices with proper documentation.

4. Reconcile output VAT and input VAT balances regularly.

5. Consult tax advisors for transactions involving mixed use or exempt supplies.

________________________________________

🚨 Common Mistakes to Avoid

• Forgetting to account for RCM at all

• Claiming input VAT for exempt/non-taxable use

• Not reconciling Box 6 and Box 10 in the return

• Ignoring proper documentation

________________________________________

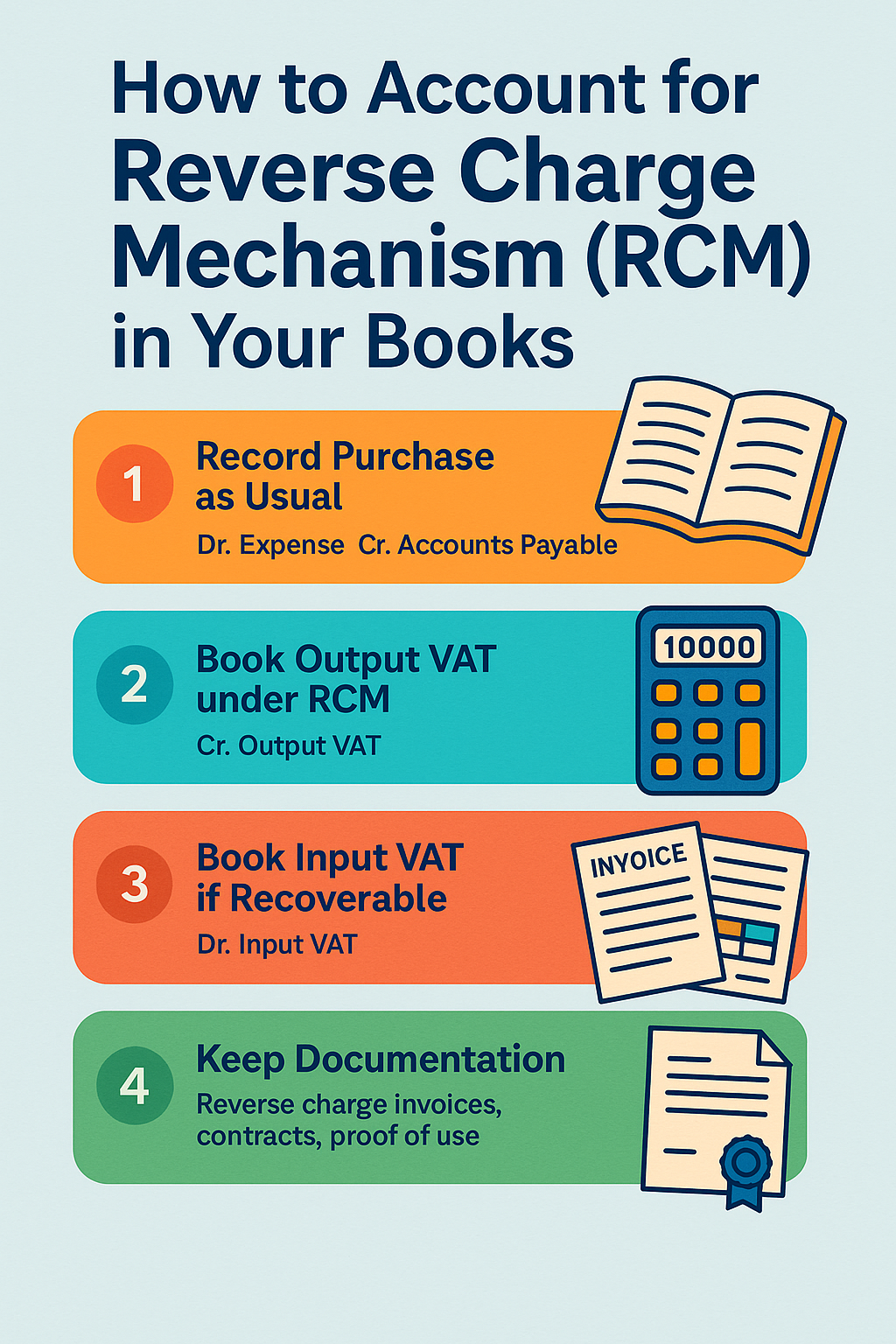

📘 Summary

Step Action

1. Record purchase as usual Dr. Expense, Cr. Payable

2. Book output VAT under RCM Cr. Output VAT

3. Book input VAT if recoverable Dr. Input VAT

4. Report in VAT Form 201 Boxes 3, 6, and 10

5. Keep documentation Reverse charge invoices, contracts, proof of use

________________________________________

🤝 Need Help?

At Sheikh Anwar Accounting & Auditing LLC, we help UAE businesses stay compliant with VAT regulations, including RCM application, accounting treatment, and return filing. Let our experts simplify your VAT journey!

🌐 Visit us: www.sa-auditors.com

📧 Email: info@sa-auditors.com

📱 WhatsApp: +971-XX-XXXXXXX