How Technology Reduces False Positives in AML

Introduction

False positives — the bane of every compliance officer’s existence.

In Anti-Money Laundering (AML) operations, a false positive occurs when a legitimate transaction or customer is incorrectly flagged as suspicious. These false alerts consume up to 80–90% of total AML investigation resources, leading to compliance fatigue, operational inefficiency, and delayed reporting.

Fortunately, with the rise of artificial intelligence (AI), machine learning (ML), and advanced analytics, financial institutions are shifting from rule-based rigidity to intelligent, data-driven accuracy. This explores how technology is transforming false-positive management and redefining efficiency in AML compliance.

________________________________________

1. Understanding False Positives in AML

What Are False Positives?

In AML systems, false positives are alerts triggered by monitoring rules that flag low-risk or normal transactions as potentially suspicious.

These often result from:

• Overly broad rule thresholds (e.g., “transactions above AED 50,000”).

• Lack of contextual data (why or where the transaction occurred).

• Outdated customer risk profiles.

• Static rules that fail to adapt to behavioral changes.

Impact on Compliance Operations

• Wasted analyst time reviewing benign alerts.

• Alert backlogs that delay genuine investigations.

• Increased compliance costs and burnout.

• Regulator criticism for ineffective risk-based approaches.

________________________________________

2. Why Traditional AML Systems Struggle

Traditional rule-based AML solutions are reactive and rigid. They operate on static thresholds, such as:

“Trigger an alert if a transaction exceeds AED 100,000.”

However, these systems cannot interpret context or behavioral nuances. For instance:

• A gold trader making large deposits is normal activity, not suspicious.

• A retail customer with sudden high-value transfers, however, may need review.

Without contextual intelligence, both cases trigger identical alerts — flooding systems with false positives.

________________________________________

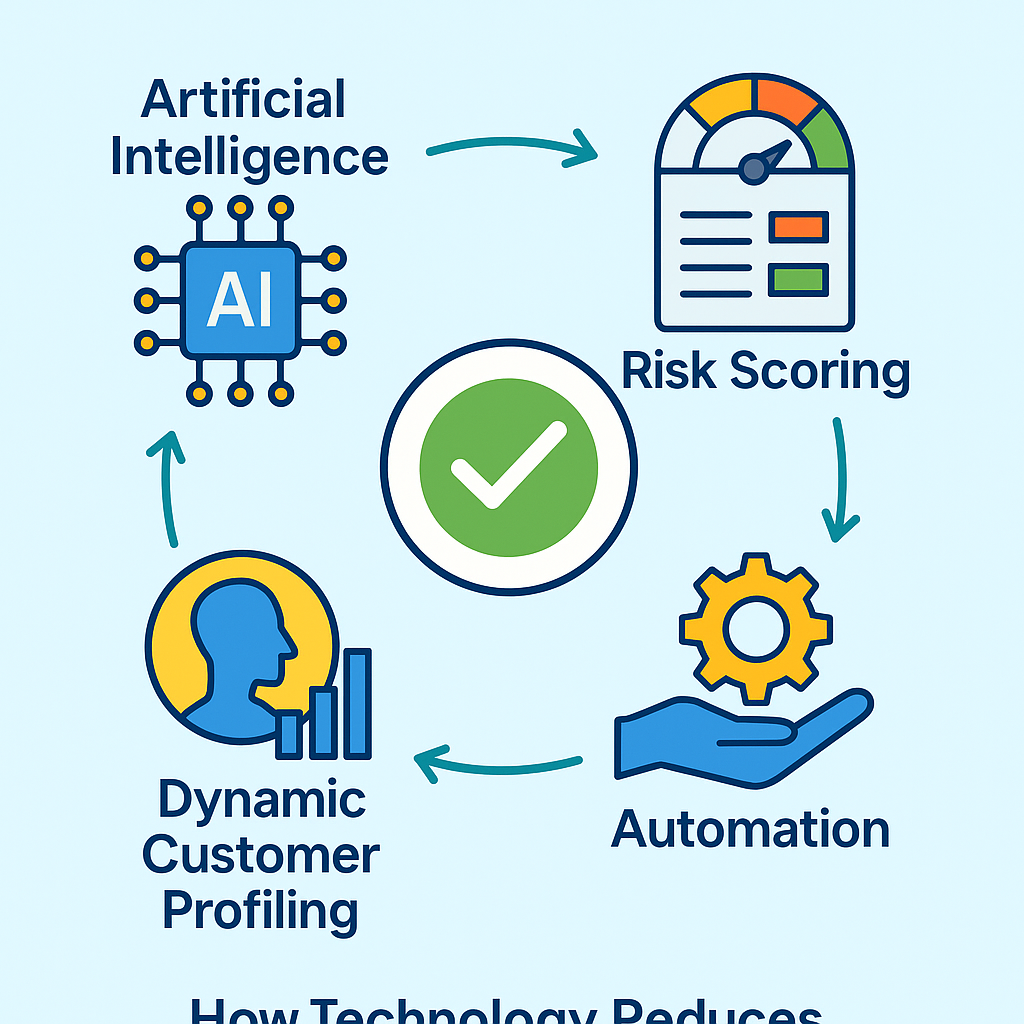

3. The Role of Technology in Reducing False Positives

Modern AML compliance is evolving from rules-based monitoring to risk-intelligent automation.

Here’s how advanced technology makes this possible:

________________________________________

A. Artificial Intelligence (AI) & Machine Learning (ML)

AI models analyze historical alert data to learn which alerts were genuine and which were false.

They then predict the probability of a new alert being truly suspicious.

How it helps:

• Learns from human investigator feedback.

• Continuously refines thresholds based on patterns.

• Prioritizes alerts by risk level — high, medium, or low.

• Reduces repetitive manual review of low-risk alerts.

Example:

An ML model learns that salary payments from the same corporate client are always legitimate and stops flagging them after repeated clearance.

________________________________________

B. Dynamic Customer Risk Profiling

Static risk ratings (Low/Medium/High) often cause irrelevant alerts.

Technology enables dynamic profiling, where customer risk evolves automatically based on:

• Transaction trends.

• Counterparty networks.

• Geographical exposure.

• Sanctions list updates.

Result: The system intelligently adapts, reducing false positives for consistent low-risk customers.

________________________________________

C. Advanced Analytics & Behavior Modeling

Predictive analytics uses historical transaction patterns to identify what is “normal” for each customer.

Alerts are only raised when activity significantly deviates from these established baselines.

Example:

A jewellery trader regularly receives AED 200,000 cash deposits. A new transaction of AED 210,000 won’t trigger an alert — because it fits the customer’s behavior profile.

________________________________________

D. Natural Language Processing (NLP) for Screening

False positives in sanctions and PEP screening often arise from name mismatches (“Ali Mohammad” vs “Mohammed Ali”).

NLP-based matching engines use phonetic, linguistic, and transliteration algorithms to:

• Accurately distinguish genuine matches from coincidental similarities.

• Understand context (e.g., nationality, address).

• Reduce screening noise while maintaining sensitivity.

________________________________________

E. Entity Resolution & Graph Analytics

Entity resolution links customer data across systems and jurisdictions, identifying the same person under multiple aliases.

Graph analytics visualizes relationships between entities to detect true risks while eliminating irrelevant matches.

Example:

A client appearing under two similar names in separate systems is recognized as the same individual — avoiding duplicate alerts.

________________________________________

F. Explainable AI (XAI)

Regulators demand transparency.

Explainable AI ensures that each alert or decision made by a machine-learning model is traceable and interpretable.

Compliance officers can view why a certain alert was suppressed or prioritized, ensuring accountability and regulatory confidence.

________________________________________

4. Integration with AML Workflows

Modern AML ecosystems integrate false-positive reduction tools with:

• Transaction Monitoring Systems (TMS) — AI-based alert scoring and case prioritization.

• KYC/CDD Platforms — Continuous customer screening with dynamic updates.

• Sanctions Engines — Intelligent fuzzy matching to prevent name-based errors.

• Case Management Tools — Unified dashboards showing AI confidence levels and analyst notes.

Such integration ensures seamless workflow automation and consistency across compliance operations.

________________________________________

5. Benefits of Technology-Driven False Positive Reduction

Benefit Impact

Reduced Alert Volume 40–70% fewer false positives.

Improved Efficiency Analysts focus on genuine suspicious cases.

Lower Operational Costs Less manual review and rework.

Faster STR Filing Timely detection and reporting to FIU (e.g., goAML).

Enhanced Regulator Confidence Evidence of risk-based, intelligent compliance.

Continuous Learning Models improve over time through feedback loops.

________________________________________

6. UAE & Global Regulatory Perspective

The UAE’s regulatory framework under:

• Federal Decree-Law No. 20 of 2018 (AML/CFT)

• Cabinet Decision No. 10 of 2019

• Cabinet Decision No. 109 of 2023 (Virtual Asset Regulation)

promotes risk-based approaches that prioritize effectiveness over volume.

Global regulators — including FATF, EU AMLA, and FinCEN — are encouraging the use of RegTech and AI to enhance detection accuracy and reduce false alerts.

The UAE’s Ministry of Economy (MOE) and Financial Intelligence Unit (FIU) support AI-driven systems that ensure timely, accurate Suspicious Transaction Reporting (STR) with minimal resource wastage.

________________________________________

7. Best Practices for Implementation

1. Start with Data Quality: Clean, unified, and enriched data is critical.

2. Adopt Explainable AI Models: Ensure full audit trails for regulator acceptance.

3. Create Feedback Loops: Let investigators’ outcomes refine model performance.

4. Monitor Model Drift: Regularly retrain models to reflect new typologies.

5. Balance Sensitivity and Specificity: Don’t over-optimize for alert reduction at the cost of missing real threats.

6. Ensure Governance: Maintain documentation, approvals, and periodic validation.

________________________________________

8. Case Example: From Rule-Based to AI-Driven

A UAE-based exchange handling high transaction volumes faced 95% false positives from its old AML monitoring system.

By implementing AI-enhanced alert scoring and behavioral analytics, it:

• Reduced false positives by 68%.

• Improved case closure rates by 55%.

• Enhanced FIU reporting accuracy and turnaround time.

This transformation showcased measurable compliance efficiency and regulator confidence.

________________________________________

9. The Future: Autonomous Compliance Systems

As AML systems evolve, we are heading toward autonomous compliance ecosystems — where:

• AI continuously self-learns from global typologies.

• Blockchain ensures data integrity.

• Predictive analytics proactively detects laundering intent.

• Compliance officers act as supervisors, not manual reviewers.

The convergence of AI, cloud computing, and RegTech platforms will eliminate manual inefficiencies and set new global standards for AML precision.

________________________________________

10. Conclusion

Reducing false positives is not just about saving time — it’s about building an effective, risk-based AML program that focuses on true threats.

Technology enables compliance teams to shift from volume-based monitoring to intelligence-based detection, enhancing both efficiency and regulatory compliance.

By adopting AI-driven, adaptive systems, organizations in the UAE and beyond can strengthen financial integrity, protect reputations, and align with the highest global AML standards.

________________________________________

About Sheikh Anwar Accounting & Auditing LLC

Sheikh Anwar Accounting & Auditing LLC (SA Auditors) — MOE Entry No. 5817 — is a leading UAE-based firm providing AML compliance, outsourced MLRO services, audit, and corporate tax advisory.

Through our RegTech platform MyAML.io, we help financial institutions and DNFBPs implement AI-based AML systems that reduce false positives, enhance detection accuracy, and maintain full regulatory alignment.

📍 Office Address: M-35, Dubai Creek Tower, Dubai, U.A.E.

📞 Phone: +971 4 250 1084

✉️ Email: info@sa-auditors.com

🌐 Websites: www.sa-auditors.com | www.myaml.io