How FATF Defines Suspicious Transactions

Introduction

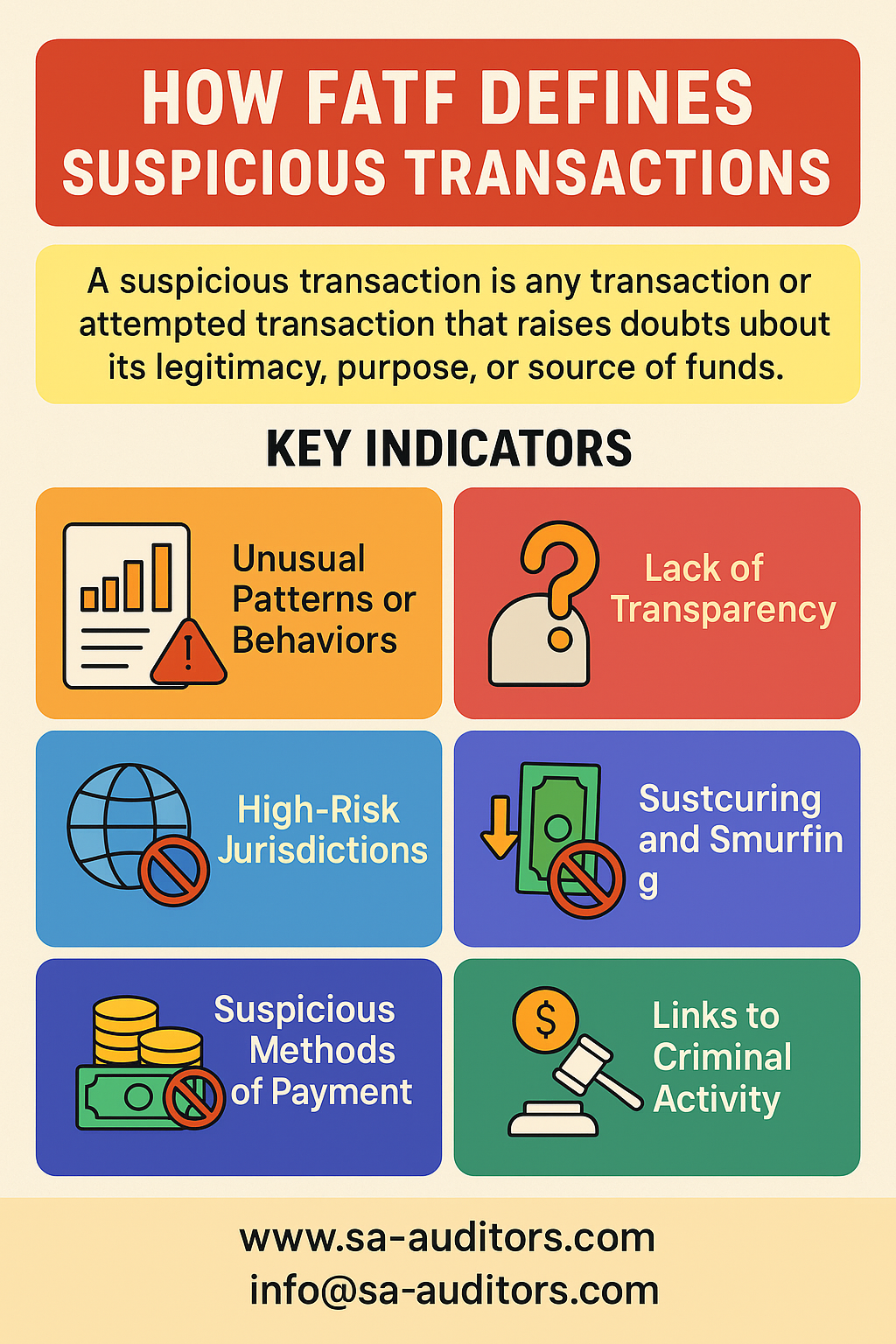

The Financial Action Task Force (FATF), as the global standard-setter for Anti-Money Laundering and Countering the Financing of Terrorism (AML/CFT), provides clear guidance on what constitutes a Suspicious Transaction. According to FATF, a suspicious transaction is any transaction or attempted transaction that raises doubts about its legitimacy, purpose, or source of funds.

These transactions may not always involve criminal activity, but the presence of certain indicators (red flags) requires financial institutions and DNFBPs to exercise enhanced scrutiny and, when appropriate, file a Suspicious Transaction Report (STR) with the Financial Intelligence Unit (FIU).

________________________________________

1. Core Definition by FATF

• A suspicious transaction is one where there are reasonable grounds to suspect that funds are the proceeds of crime or related to terrorist financing.

• Suspicion can arise from the nature, size, frequency, or pattern of transactions.

• Both completed and attempted transactions fall within this scope.

________________________________________

2. Key FATF Criteria for Suspicious Transactions

FATF highlights several situations where a transaction may be deemed suspicious:

a) Unusual Patterns or Behaviors

• Transactions inconsistent with a customer’s known profile or business activities.

• Abrupt changes in financial behavior (e.g., sudden large transfers).

b) Lack of Transparency

• Clients reluctant to provide information or submit incomplete/false documents.

• Use of complex structures without clear business rationale.

c) High-Risk Jurisdictions

• Transactions linked to countries with weak AML/CFT controls, sanctions, or secrecy laws.

d) Structuring and Smurfing

• Breaking down large transactions into smaller ones to avoid reporting thresholds.

e) Suspicious Methods of Payment

• Heavy use of cash or third-party payments.

• Transactions routed through unusual intermediaries or unrelated accounts.

f) Links to Criminal Activity

• Funds suspected to be connected to drug trafficking, corruption, tax evasion, or terrorist networks.

________________________________________

3. FATF Guidance on Reporting

• Obligation to Report: When suspicion arises, the institution or DNFBP must file an STR without delay.

• No Requirement for Proof: FATF clarifies that staff do not need evidence of a crime—just reasonable grounds to suspect.

• Confidentiality: Entities must keep STR filings confidential to protect both the investigation and the reporting staff.

________________________________________

4. Examples of FATF Suspicious Transaction Indicators

• A real estate purchase paid entirely in cash without legitimate explanation.

• Jewellery dealer clients making multiple transactions just below AED 55,000 threshold.

• Company service providers setting up entities with nominee shareholders and unexplained ownership structures.

• Transfers between accounts in multiple jurisdictions with no economic justification.

________________________________________

5. Importance for UAE DNFBPs

In the UAE, DNFBPs are under strict obligation to align with FATF recommendations, as implemented through Federal Decree-Law No. 20 of 2018 and Cabinet Decision No. 10 of 2019. Identifying and reporting suspicious transactions is a critical responsibility to:

• Strengthen the UAE’s AML/CFT framework.

• Avoid regulatory penalties.

• Protect businesses from being used as channels for illicit activities.

________________________________________

📩 For AML training and STR compliance support, contact us:

Sheikh Anwar Accounting & Auditing LLC

🌐 www.sa-auditors.com

📧 info@sa-auditors.com