Guidelines for Cross-border Invoicing

Introduction

As businesses in the UAE increasingly engage in international trade, it is essential to understand the rules for cross-border invoicing under the UAE VAT Law. Whether you are exporting goods, importing services, or dealing with foreign clients, your VAT invoices must reflect the correct treatment to remain compliant with the Federal Tax Authority (FTA).

It outlines the key rules, invoice content, and compliance guidelines for issuing cross-border VAT invoices in the UAE.

________________________________________

📦 What is a Cross-Border Invoice?

A cross-border invoice is issued when goods or services are sold or purchased across country borders. This includes:

• Exports of goods/services from UAE

• Imports of goods/services into UAE

• Supplies to or from GCC countries

Correct treatment depends on whether the customer is located inside or outside the GCC, and whether the supply is of goods or services.

________________________________________

✅ Key VAT Treatments for Cross-Border Transactions

Transaction Type VAT Treatment Invoicing Note

Export of goods (outside GCC) Zero-rated (0%) Must retain export evidence

Export of services (to outside UAE) Zero-rated (0%) if conditions met Must prove client is outside UAE

Import of goods Subject to reverse charge VAT paid via customs/import declaration

Import of services Reverse charge applies VAT accounted by UAE recipient

Supply to GCC VAT-registered customer Zero-rated, if TRN verified and transport proven Must mention recipient’s TRN

Supply to unregistered GCC customer Standard-rated (5%) Treated as local UAE supply

________________________________________

🧾 Invoicing Guidelines for Cross-Border Transactions

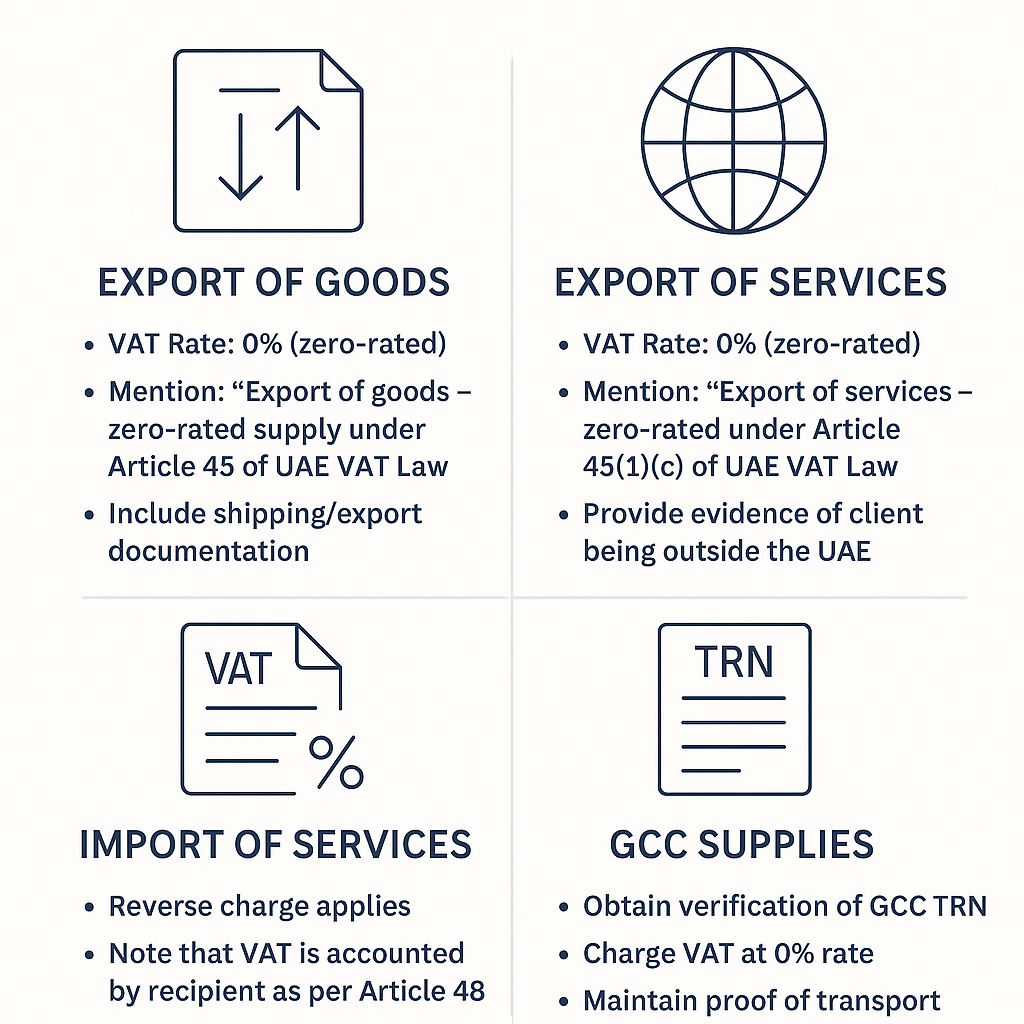

🔹 For Exports of Goods (Outside GCC)

• Issue a full tax invoice even for zero-rated supplies

• Mention: “Export of goods – zero-rated supply under Article 45 of UAE VAT Law”

• Include shipping/export documentation

• Include customer name and address, even if not VAT-registered

• VAT Rate: 0%

________________________________________

🔹 For Export of Services (to Clients Outside UAE)

• VAT zero-rated only if:

o Customer is not in the UAE

o Customer is not using the service within UAE

• Invoice must mention:

“Export of services – zero-rated under Article 45(1)(c) of UAE VAT Law”

• Include evidence such as:

o Client’s foreign address

o Contract specifying location of use

________________________________________

🔹 For Import of Services (Cross-border B2B from Non-UAE Supplier)

• UAE business must self-account for VAT via reverse charge

• VAT must be shown in VAT return (Form 201 – Boxes 3 & 10)

• Supplier invoice must include:

o Supplier details (may or may not have TRN)

o Clear description of service

• Recipient must annotate:

“Reverse charge applies – VAT to be accounted by recipient as per Article 48”

________________________________________

🔹 For GCC Supplies (If Recipient is VAT-Registered)

• Verify customer’s GCC TRN (e.g., KSA, Bahrain)

• Maintain proof of transport and customer location

• Charge VAT at 0% and issue full tax invoice

• Mention:

“Intra-GCC supply – zero-rated under GCC VAT Framework”

________________________________________

📋 Must-Have Details on a Cross-Border Invoice

Field Description

Supplier Name, Address, TRN Must be included

Customer Name, Address Especially if based outside UAE

Invoice Date & Number Sequential and unique

Description of Supply Goods or services provided

Place of Supply Determines VAT treatment

VAT Rate 0%, 5%, or Reverse Charge

Currency Preferably AED; other currencies allowed with AED equivalent

Reverse Charge Note (if applicable) Mandatory for import of services

________________________________________

🔁 Currency and Exchange Rate Requirements

• Invoices can be in foreign currencies, but:

o VAT amount must be shown in AED

o Use CBUAE exchange rate on the date of supply

o Mention exchange rate used

________________________________________

🔎 Recordkeeping & Documentation

To ensure compliance and justify VAT treatment, retain:

• Customs declarations (for imports)

• Airway bills, bill of lading, or delivery notes

• Service contracts showing overseas use

• TRN validation records for GCC transactions

• Self-invoices or debit notes (for imports)

FTA requires records to be kept for at least 5 years.

________________________________________

⚠️ Common Mistakes to Avoid

Mistake Risk

Charging 5% VAT on exports Overpayment, audit risk

Using simplified invoice for export Non-compliance

Not verifying GCC TRN Wrong VAT treatment

Ignoring reverse charge on imported services Underreporting VAT

Missing AED conversion VAT calculation error

________________________________________

🧠 Final Thoughts

Cross-border invoicing under UAE VAT law involves complex rules, especially in distinguishing between zero-rated, standard-rated, and reverse charge transactions. Proper invoice formatting, documentation, and reporting are critical to maintaining compliance and avoiding FTA penalties.

💼 Need help verifying VAT treatments on your international invoices?

Contact Sheikh Anwar Accounting & Auditing LLC for professional advice and invoicing system setup.

📧 info@sa-auditors.com

🌐 www.sa-auditors.com