Group Taxation Under UAE Law

Introduction

The UAE Corporate Tax Law introduces provisions that allow business groups to benefit from group taxation, enabling them to simplify tax compliance, consolidate tax returns, and optimize tax liability.

Here we explains the concept of Tax Groups, the legal framework under UAE law, eligibility criteria, benefits, limitations, and compliance obligations—so your business can make informed decisions when forming or joining a Tax Group.

________________________________________

📚 Legal Basis

The group taxation provisions are set out in:

• Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses

• Article 40 to 42 – Tax Group rules

• Ministerial Decision No. 125 of 2023 – Tax group formation, continuation, and dissolution

• FTA Public Clarifications (where applicable)

________________________________________

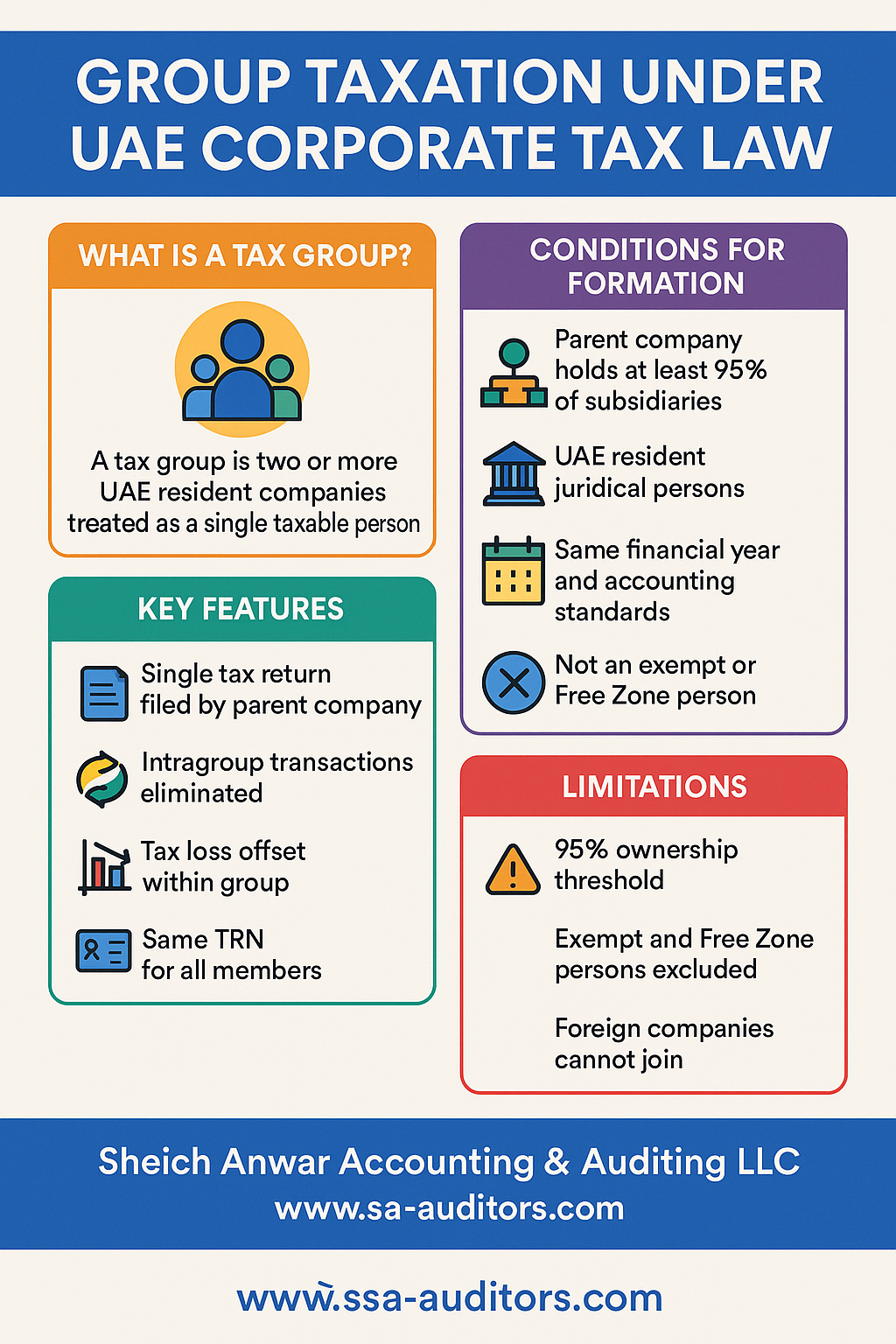

🧾 What Is a Tax Group?

A Tax Group is a group of two or more UAE resident juridical persons (companies) that are treated as a single taxable person for Corporate Tax purposes.

Once formed:

• The parent company files a single consolidated Corporate Tax return on behalf of the group.

• Intragroup transactions are eliminated, and profits/losses are pooled.

• The group is treated as one legal taxable unit for UAE Corporate Tax purposes.

________________________________________

✅ Conditions for Forming a Tax Group

To form a Tax Group, the following requirements must be met:

1. Parent-Subsidiary Relationship:

o The parent company must hold at least 95% of the voting rights, share capital, and entitlement to profits/losses of each subsidiary.

2. UAE Resident Legal Persons:

o Both the parent and subsidiaries must be resident juridical persons (not natural persons).

3. Same Financial Year and Accounting Standards:

o All group members must follow the same financial year and prepare accounts using the same accounting standards (e.g., IFRS).

4. Not an Exempt or Qualifying Free Zone Person:

o Companies that are exempt persons or qualifying free zone persons cannot be part of a Tax Group.

________________________________________

🧾 How to Form a Tax Group?

1. Submit an Application through the EmaraTax portal

2. Application must be jointly filed by the parent and subsidiary(ies)

3. Approval is subject to FTA’s confirmation

4. Once approved, the group will receive a single Corporate Tax Registration Number (TRN)

________________________________________

🧠 Key Features of a Tax Group

Feature Explanation

Single Tax Return Filed by the parent company for all members

Intragroup Transactions Eliminated for tax purposes

Tax Loss Offset Losses from one group company can offset profits of another (within limits)

No separate filings Subsidiaries do not file individual returns

Taxable Income Threshold The AED 375,000 threshold applies to the whole group as one entity

________________________________________

💡 Benefits of Tax Grouping

• ✅ Administrative efficiency – only one tax return

• ✅ Offset profits and losses across the group

• ✅ Elimination of internal transactions

• ✅ Cash flow optimization within the group

• ✅ Reduced risk of penalties due to unified filing

________________________________________

🚫 Limitations and Exclusions

• ❌ Exempt persons (e.g., government entities, pension funds) cannot join

• ❌ Qualifying Free Zone Persons (enjoying 0% CT) are excluded

• ❌ Foreign companies (even with UAE branches) cannot be part of the Tax Group

• ❌ Complex ownership structures might not meet the 95% test

________________________________________

🔄 Adjustments After Group Formation

➕ Adding or Removing Members:

• Can be done through amendments via EmaraTax

• Subject to FTA approval

💼 Dissolution of the Group:

• Occurs if the 95% control test fails, or companies cease operations

• Each member becomes a separate taxable person again

________________________________________

📆 Effective Date of Tax Group

• The Tax Group is effective from the start of the tax period in which the application is submitted and approved (or from a later date if specified).

________________________________________

🧾 Tax Losses Within a Tax Group

• Tax losses incurred by one member before joining the Tax Group:

o Can only be carried forward by that entity

• Losses incurred after formation are available to the entire group, subject to the 75% loss offset limitation

________________________________________

🧮 Example Scenario

Parent Company A owns 100% of Subsidiaries B and C.

Company Net Income

A AED 200,000

B AED (150,000) loss

C AED 100,000

➡️ The group’s total taxable income = AED 150,000

➡️ Taxable income below AED 375,000 → 0% tax

➡️ Filed under a single TRN by Company A

________________________________________

🧠 How Sheikh Anwar Accounting & Auditing LLC Can Help

We assist clients in:

✅ Assessing eligibility for forming a Tax Group

✅ Preparing and filing Tax Group applications

✅ Setting up intercompany accounting and eliminations

✅ Managing consolidated tax compliance

✅ Reviewing group structures for optimization

________________________________________

📞 Contact Us

📍 Sheikh Anwar Accounting & Auditing LLC

🌐 www.sa-auditors.com

📧 info@sa-auditors.com

📞 +971-XX-XXX-XXXX